The Bank of Canada interest rate increases have been top of mind for Canadians across the country. The real estate market started with a boom in 2022; home prices were high, the competition was steep, and interest rates were low. In March, the Bank increased its overnight lending rate for the first time since the start of the pandemic. Since then, rates have increased three more times to its current rate of 2.5%. With another rate increase expected in September, prospective and existing homeowners are wondering whether they should choose a variable or fixed-rate mortgage while interest rates are rising. Here are four tips to help you decide.

Fixed-Rate Mortgages

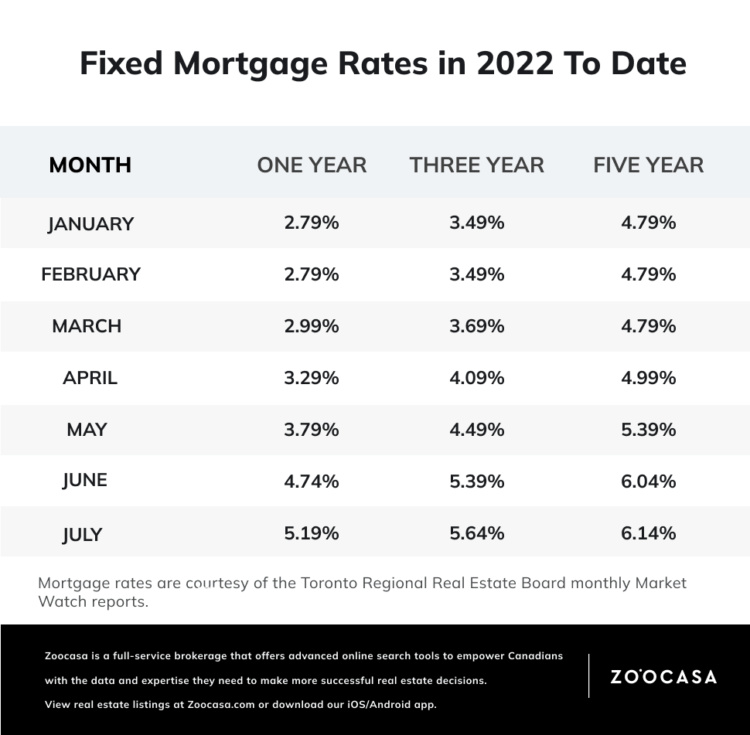

A fixed-rate mortgage stays the same throughout the entire term of your loan but means less purchasing power for buyers if payments are higher. The length of these contracts can vary, from a few months to a decade, but they are often three or five-year terms. They generally have higher rates than variable-rate mortgages, but can be a great option if you are able to lock in at a low-interest rate, or if you’d rather budget for consistent payments regardless of how the market changes.

Variable-Rate Mortgages

The interest rate of a variable-rate mortgage will change as the prime rate of your financial institution changes. These rates vary according to the key interest rate issued by the Bank of Canada. This is a good option if interest rates are low or expected to drop, and you have some flexibility in your household income to shoulder changes in monthly payments throughout your mortgage term. Variable rates tend to be slightly lower than fixed rates because they are inherently less risky for lenders.

A capped variable rate is also an option, which means your payments will never exceed a certain threshold, but there is usually an additional premium that comes along with this.

Generally speaking, variable-rate mortgages have proven to be less expensive over time than fixed-rate mortgages, but significant increases in the prime rate will increase the amount you have to pay. Fixed-rate offers more stability but if there’s a significant difference between the two types of mortgages, it may not be worth paying the premium.

Four Tips to Help You Decide Between a Variable or Fixed-Rate Mortgage

1. Determine if you’re planning to stay in the home long term

If you’re not planning to stay in your home for the entirety of your mortgage term, or perhaps are planning to live in it for a few years and then rent it out, there could be a penalty for breaking a fixed-rate mortgage. The penalty is calculated using the Interest Rate Differential (IRD), where your lender uses two interest rates to calculate the interest fees left to pay on your current term for both rates. The difference is the amount owing when breaking a fixed-rate mortgage.

With a variable-rate mortgage, homeowners have the option to break their mortgage at any point. There may still be pre-payment penalties, but they are usually much lower than the IRD penalty that those with fixed mortgages may face.

2. Understand your financial situation

Before committing to any type of mortgage, it’s important to analyze your household financial situation. This is the time to consider your job history and whether your current role is long-term and stable, or if you may need to enter the job market in the future. It’s also important to look at your monthly expenses and determine whether you have a financial cushion that allows for some wiggle room in monthly payments, especially if they go up.

3. Shop around to get the best rate

Shop around to learn what options are available to you for both types of mortgages so you can compare them accurately. There are many websites available that compare available mortgage rates, and you can also use a mortgage broker or shop around with different lenders to learn about all the rates available to you. Keep in mind that a mortgage application counts as a “hard hit” on your credit and may cause it to dip by ten or so points. Some experts recommend applying to no more than four mortgages in a short period of time.

4. Leverage expert advice

If you have a financial planner, a mortgage broker, or a trusted real estate agent, they will all have a wealth of information that can help you determine which option is right for you. You can often set up a call or in-person meeting for free to discuss your options and goals.