The First-Time Home Buyer Incentive (FTHBI) has been highly scrutinized since it was first announced by the federal government in March; the program, which will see the Canada Mortgage and Housing Corporation (CMHC) provide interest-free down payment loans to home buyers in exchange for a share of equity, is considered to have restrictions too strict to really make a mark in Canada’s priciest markets.

The

What Does the FTHBI Do?

The FTHBI works by adding an interest-free second mortgage to the home purchase, which only needs to be paid back once the home is sold or the 25-year mortgage amortization matures. It cannot be paid back in installments, though homeowners are able to pay it off early with a lump sum. In exchange for the interest-free loan, the CMHC assumes an equity position in the home’s value, which can increase or decrease depending on market performance.

The loan reduces the size of the mortgage upfront, thereby reducing monthly payments and the amount of interest paid. The CMHC calculates that for a buyer receiving the maximum 10% (allowable on newly-built homes only), they’d save $286 per month, resulting in $3,430 in savings per year.

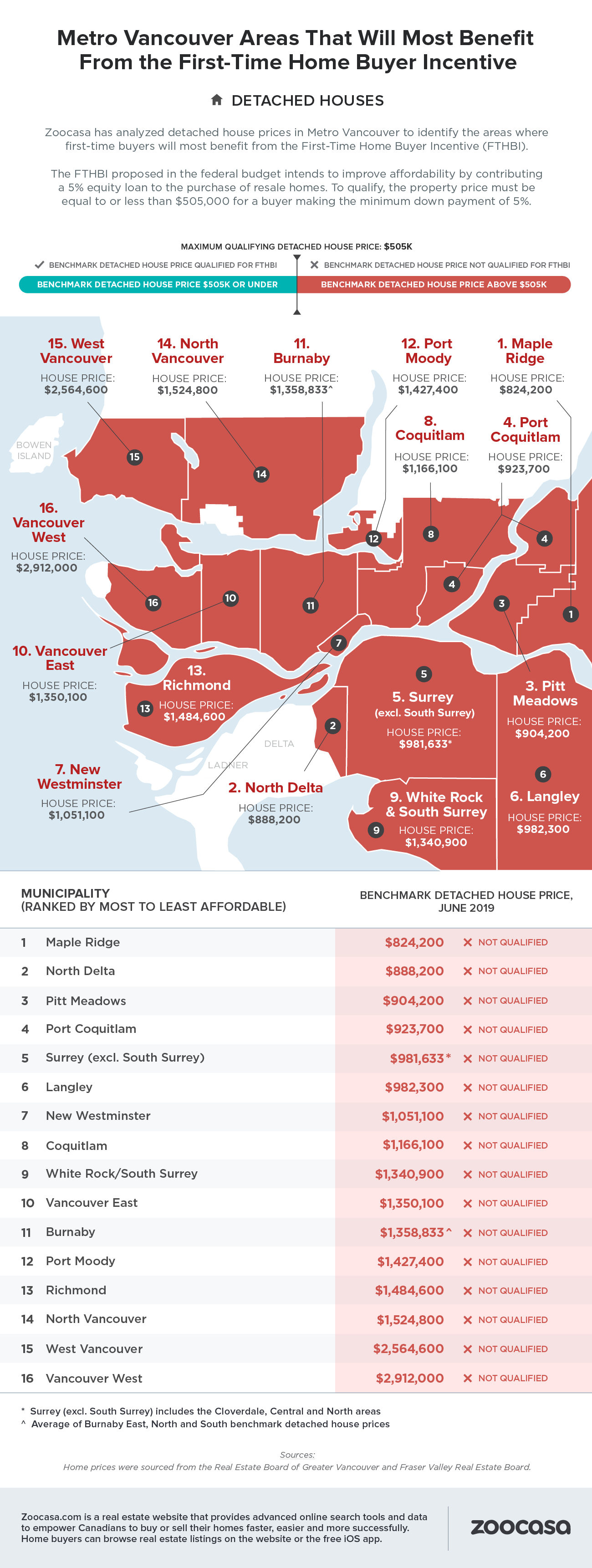

Home Price Restrictions Too Low for Vancouver Market

However, the

- Related Reads:

Can the First-Time Home Buyer Incentive Be Used in Toronto? - Alberta Housing Markets Where the FTHBI Will be Most Effective

That arguably doesn’t have much traction in a market like Metro Vancouver; benchmark prices for Vancouver homes for sale were $998,700 in June according to the Real Estate Board of Greater Vancouver; benchmark detached houses fetch $1,423,500 while benchmark apartments – likely the only viable entry point to the market for most first-time buyers – sit at $654,700.

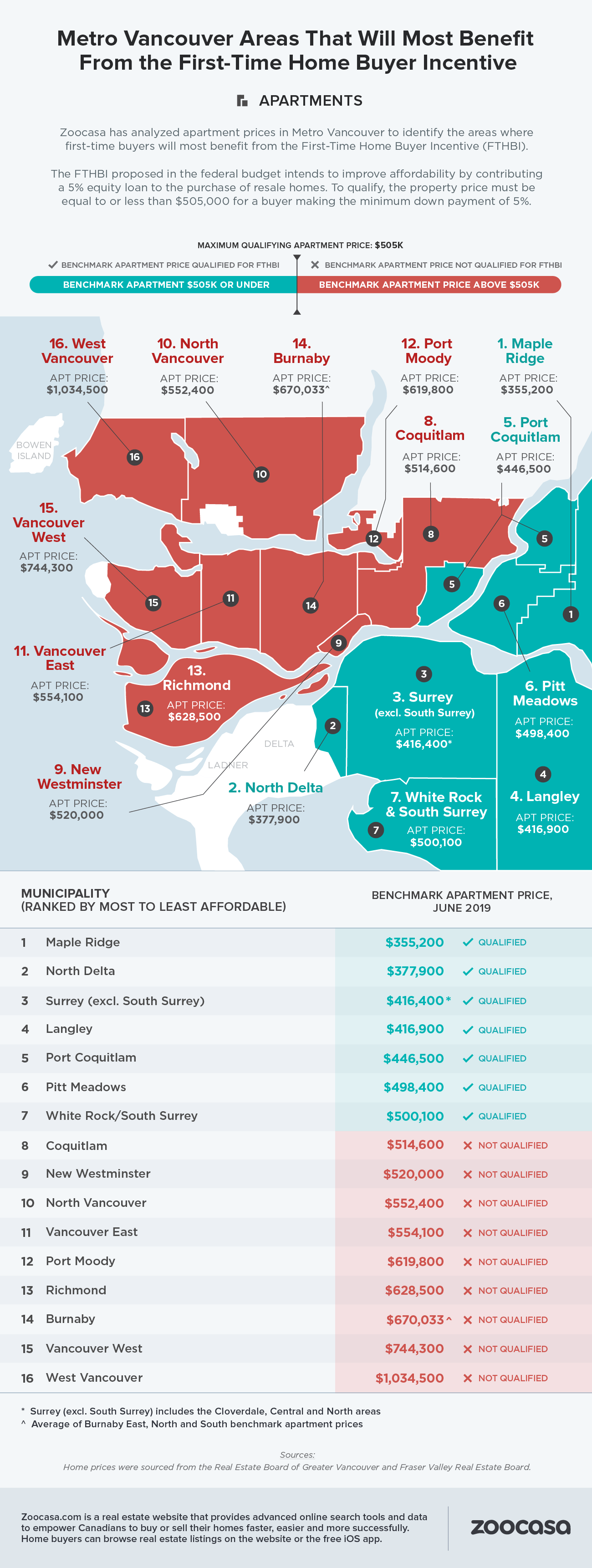

Only Apartment Purchasers Eligible in Metro Vancouver

In fact, according to recent calculations by Zoocasa, if you’re looking to purchase a benchmark-priced house in one of 16 Metro Vancouver markets using the FTHBI, you’d be out of luck altogether; there are no options priced low enough to qualify for the program anywhere in the region.

However, for apartment buyers, there are some options available in seven markets, though they remain beyond the downtown core. Here, benchmark apartment prices could potentially qualify for the FTHBI, assuming a home buyer qualifies based on household income of $120,000 and has saved the requisite 5% down payment. Home prices were sourced from the Real Estate Board of Greater Vancouver and the Fraser Valley Real Estate Board for the month of

Markets with qualifying benchmark apartment prices include:

- Maple Ridge: $355,200

- North Delta: $377,900

- Surrey (excluding South Surrey): $416,400

- Langley: $416,900

- Port Coquitlam: $446,500

- Pitt Meadows: $498,400

- White Rock / South Surrey: $500,100

Check out the infographics below to see where it’s possible to utilize the FTHBI in Metro Vancouver:

Methodology

Sources:

- Benchmark home prices were sourced from the Real Estate Board of Greater Vancouver and Fraser Valley Real Estate Board.

- It is assumed home buyers have the maximum combined household income of $

120,000, and have saved the minimum 5% down payment for a home priced at $505,000.

About Zoocasa

Zoocasa.com is a real estate website that provides advanced online search tools and data to empower Canadians to buy or sell their homes faster, easier and more successfully. Home buyers can browse real estate listings on the website or the free iOS app.

For more information about this report or to set up a media interview, please email [email protected].