When the federal Liberal government unveiled its budget back in March, it contained a key piece of new housing policy that caused ripples – both good and bad – throughout the market. Called the First-Time Home Buyer Incentive, it marked the Canadian government’s foray into shared equity mortgages, with its Crown Corporation housing agency declaring it would shoulder the down payment cost for eligible first-time buyers.

To go into effect this autumn, the FTHBI will invest $1.25 billion over three years and will provide loans of 5% to first-time buyers of resale homes, and 10% for new build purchases. The loans will be interest-free, paid back only when the home is sold or the mortgage matures, and the total amount owed will increase or decrease based on the percentage of equity and market conditions.

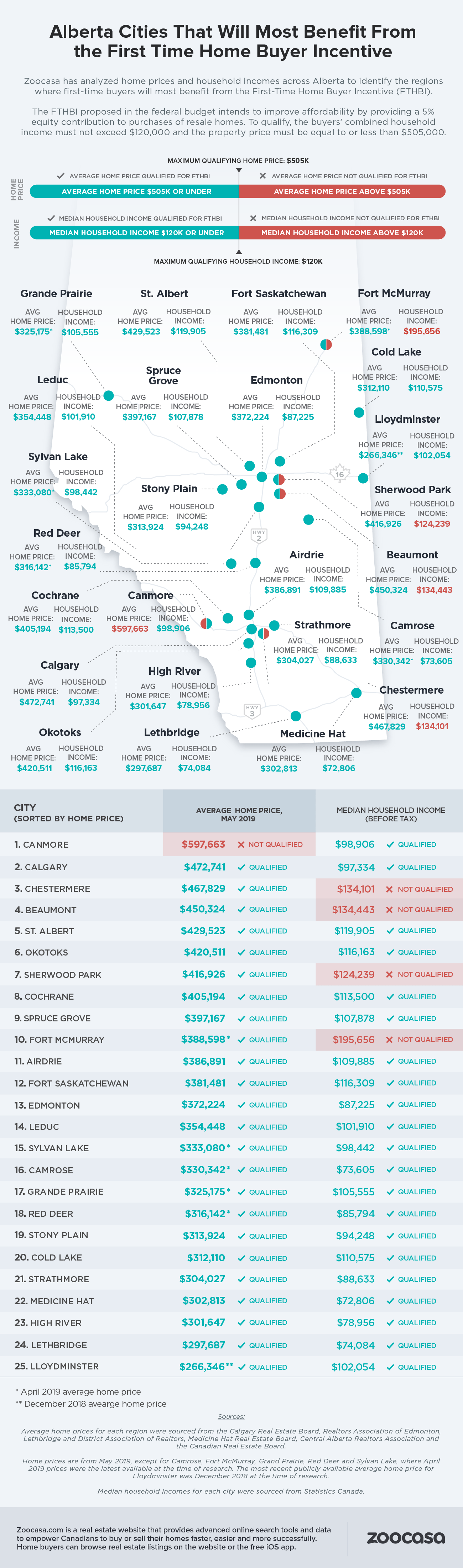

To qualify, home buyers must have a combined household income of less than or equal to $120,000, have a 5% down payment saved, and purchase a home priced at or lower than $505,000.

Criticism for the Incentive

It is due to these restrictions that the FTHBI has come under scrutiny; with average home prices pushing a million or more in Canada’s largest urban markets, critics say the criteria are simply too low for the program to be utilized in the markets where first timers would need it most.

Leading up to the FTHBI’s unveiling, there had been calls from real estate and mortgage analysts to instead reduce the criteria for the federal mortgage stress test, which requires borrowers to qualify at a rate roughly 2% higher than the one they’ll receive from their lender, or extend the maximum amortization period for high-ratio first-time buyers to 30 years. Currently, these borrowers have a capped timeline of 25 years to pay off their mortgages.

The CMHC has since defended its choice of policy, stating that it was the only solution that would alleviate down payment costs while preventing home prices from rising further; they calculate that reducing 1 per cent from the mortgage stress test or extending amortizations to 30 years would be akin to tacking 5 – 6 per cent onto current home prices, driving affordability even further out of reach for first-time buyers.

Most Albertan Markets Widely Qualify for FTHBI

However, affordability in housing markets across Canada swings wildly, with average home prices clocking in at hundreds of thousands of dollars less depending on the city and province. In fact, according to new data compiled by Zoocasa, an initiative such as the FTHBI could be widely effective in Albertan housing markets.

The study, which analyzed average home prices and median incomes across the province, found that the

Based on the criteria, buyers in the province’s two most populous cities would qualify. A buyer perusing Calgary real estate listings would be able to utilize the

According to the data, a first-time buyer purchasing a home in the following cities would not qualify for the FTHBI, based on the average home price or median income:

Canmore

Average Home Price: $597,663 (does not qualify)

Median Household Income: $98,906 (qualifies)

Chestermere

Average Home Price: $467,829 (qualifies)

Median Household Income: $134,101 (does not qualify)

Beaumont

Average Home Price: $450,324 (qualifies)

Median Household Income: $134,443 (does not qualify)

Sherwood Park

Average Home Price: $416,926 (qualifies)

Median Household Income: $124,239 (does not qualify)

Fort McMurray

Average Home Price: $388,598 (qualifies)

Median Household Income: $195,656 (does not qualify)

However, as these calculations are based on average and median criteria, it’s important to note that there may still be buyers who qualify for the FTHBI in every city, should they be purchasing a home priced below the average, or earn less than the median income.

Methodology

Average home prices for each region were sourced from the Calgary Real Estate Board, Realtors Association of Edmonton, Lethbridge and District Association of Realtors, Medicine Hat Real Estate Board, Central Alberta Realtors Association and the Canadian Real Estate Board. Home prices are from May 2019, except for Camrose, Fort McMurray, Grand Prairie, Red Deer and Sylvan Lake, where April 2019 prices were the latest available at the time of research. The most recent publicly available average home price for Lloydminster was December 2018 at the time of research.

Median household incomes for each region were sourced from Statistics Canada.

About Zoocasa

Zoocasa.com is a tech-driven brokerage that empowers Canadians to make more informed real estate decisions. Our proprietary home search tools and streamlined agent experience make buying and selling homes smarter, faster and more successful. Home buyers can browse real estate listings on the website or the free real estate iOS app.

For more information about this report or to set up a media interview, please email [email protected].