National real estate sales continued to improve in May, inching closer to the historical norm. That’s put upward pressure on home prices and has also prompted the Canadian Real Estate Association (CREA) to positively update its forecast for the remainder of this year and next.

Sales rose 1.9% last month from April levels, and 6.7% from the same time in 2018; that’s the highest sales activity since January

The supply of new homes for sale also shrank slightly, with -1.2% fewer new listings brought to market compared to the month before. Combined with increased sales, that’s nudged market conditions closer to seller-friendly territory, and heated the average national home price by 1.8% to $508,000.

However, the Home Price Index, which measures the overall value of homes sold, fell for the 5thstraight month, down -0.6% from May 2018. This could indicate a greater proportion of more affordable homes sold, such as condos, as higher-priced single-family homes remain out of financial reach for buyers in Canada’s hottest markets. Dramatic declines in sales and prices in British Columbia markets also pulled the HPI down by the most in a decade.

CREA Reverses Glum Forecast as Sales Improve

CREA expects this uptick in sales to continue well into 2020, and has reversed its previous forecast for a -1.6% decline this year to an increase of 1.2%, which would total 463,000 homes changing hands. That will rise by an additional 4.4% in 2020. The average national home price, however, will dip slightly this year by -0.6% before increasing again by 0.9% to $490,000 next year.

While an uptick in sales is encouraging, CREA is quick to point out that improvements are uneven across the country, with a growing gap in price trends between Eastern and Western Canada; it expects price pain to continue in British Columbia, Alberta, and Saskatchewan, while heating in Ontario, Quebec, and the Maritime provinces.

Stress Test Continues to Quell Markets

As it has over the last year, CREA continues to pin the stressors in these declining markets on the nationally-mandated mortgage stress test, which requires mortgage borrowers to qualify for a mortgage rate roughly 2 per cent higher than the one they’ll actually receive from their bank. That’s chopped purchasing power and is being especially felt in markets where employment and migration aren’t helping to prop up real estate demand.

That’s led to supply and demand imbalances in depressed markets, and should prompt a second look from policy makers, says Gregory Klump, CREA’s chief economist.

“The mortgage stress test continues to present challenges for home buyers in housing markets where they have plenty of homes to choose from but are forced by the test to save up for a bigger down payment,” he stated. “Hopefully the stress test can be fine tuned to enable home buyers to qualify for mortgage financing sooner without causing prices to shoot up.”

Edging Towards a Sellers’ Market

Overall, the national housing market became a little more heated for buyers, as demand outweighed the supply of new homes in several markets. The national sales-to-new-listings ratio – a metric used to measure the level of competition in a market – clocked in at 57.4%, up from 55.7% last month. CREA defines a ratio between 40 – 60% to be a balanced market, with below and above that range indicating buyers’ and sellers’ markets, respectively. While the May market edged closer to sellers’ conditions, it remains balanced as a whole, with three quarters of all markets remaining in balanced territory. However, buying conditions are a bit tighter than usual, above the long-term average of 53.5%.

Months of inventory, which reflects the total amount of time required to completely sell off all available homes for sale, was 5.1 in May, down from 5.3 in April, and 5.6 in February. However, the supply of inventory was spread unevenly across the country with a glut of available homes in the prairie provinces as well as in Newfoundland and Labrador, and less than usual in Ontario and the Maritimes.

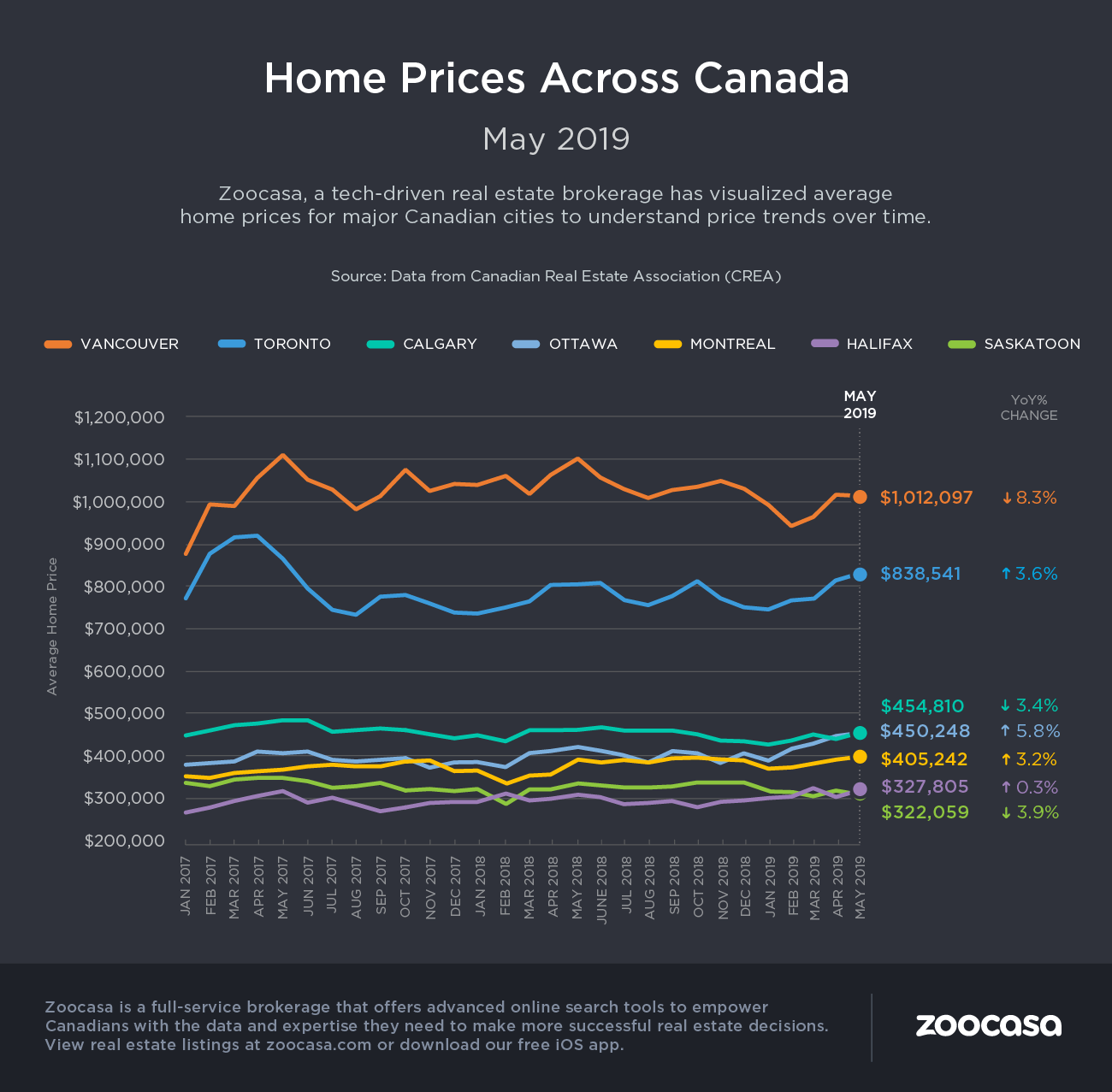

Home Prices by Region

British Columbia: The Greater Vancouver MLS and Fraser Valley markets continue to absorb large declines with prices falling -8.9% and -5.9%. The Okanagan also saw a more moderate price decrease of -0.7%, though they rose by 1% in Victoria and 4.7% elsewhere on Vancouver Island.

Ontario: May home prices rose in every market except Barrie and District, which declined by -6.1%. Otherwise, they were up 5.7% in Guelph, 5.4% in the Niagara Region, 3.4% in Hamilton-Burlington, 3.4% in Oakville-Milton, 3.1% in the GTA, and up 8% in Ottawa.

Prairies: Supply remains well above sales levels in Canada’s

Eastern Canada: Montreal continues to boom, with healthy demand pushing prices up by 6%. Greater Moncton also saw an improvement of 2% over the course of the month.