The First-Time Home Buyer Incentive (FTHBI), the federal government’s new mortgage equity sharing program, has been somewhat controversial from the get-go; there was little clarity on the nuts and bolts of the program when it was first announced in March, and there are concerns its criteria are too restrictive to really help average first-time buyers.

However, new information released this week addresses some of those questions, as the Canada Mortgage and Housing Corporation (CMHC) delved into further detail on borrower eligibility, as well as how equity sharing will work in a fluctuating market. It also announced the FTHBI will officially go into effect in September of this year.

Who Is Eligible for the FTHBI?

The

How Does the FTHBI Work?

The FTHBI is designed to improve affordability by reducing the size of the overall mortgage, and thereby the monthly payments, alleviating the financial strain on home buyers and improving their overall debt servicing ability. For example, a buyer receiving the maximum 10% loan on a newly-built home could save as much as $286 per month, resulting in $3,430 in savings per year, according to the CMHC.

The money the CMHC kicks in takes the form of a second mortgage on the home, which is interest-free, and only needs to be paid back once the 25-year mortgage matures or the home is sold, though borrowers have the option to pay it back any time as a lump sum without financial penalty.

Loan Size Increases with the Value of the Home

However, rather than a traditional cash-value loan, the money provided is in exchange for a share of equity in the property; it’s this percentage that must be paid back, meaning homeowners may need to shell out more when the loan matures.

For example, let’s say the CMHC provides a 5% loan of $25,000 for a home purchase of $500,000. The homeowner sells the home several years later, and its value has increased to $550,000. The homeowner would then need to pay the CMHC back $27,500 to reflect 5% of the increased value of the home. However, if the home loses value over that time period, only the original amount of $25,000 would be due to the CMHC upon its sale.

Could the FTHBI Be Used in a Market Like Toronto?

A main criticism for the

For example, buyers are hard pressed to find a resale home within the eligible price range in the City of Toronto, where the average home price came to a whopping $937,804 in May.

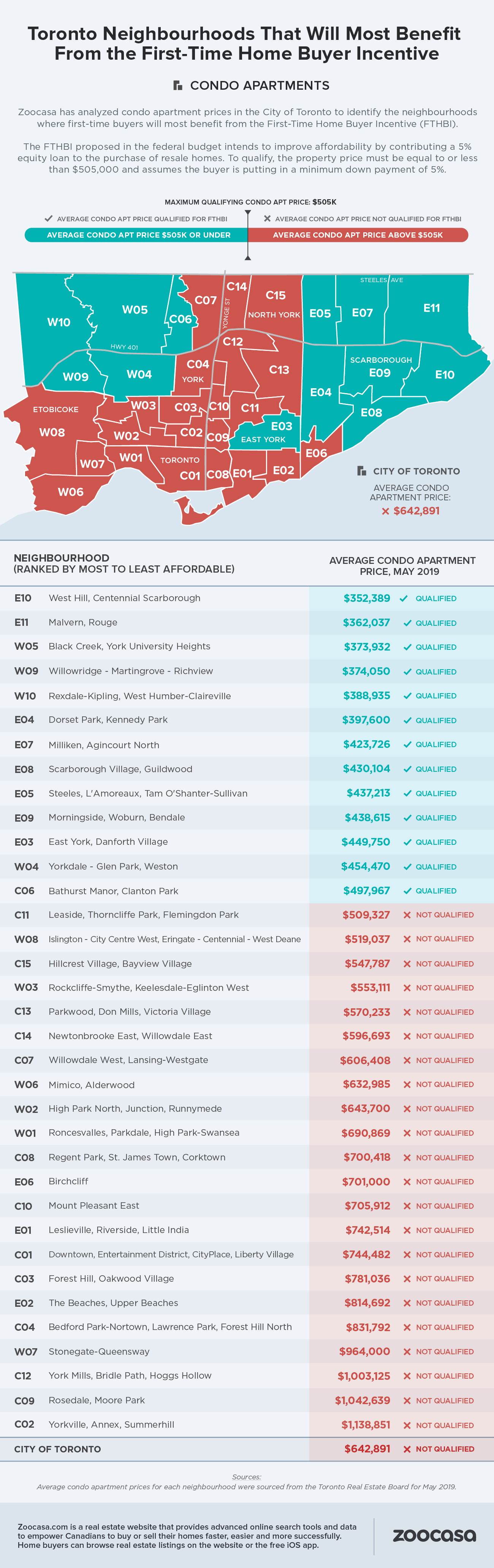

FTHBI Would Only Be Available to Toronto Condo Buyers

In fact, according to recent data compiled by Zoocasa, there are only 13 out of the city’s 35 MLS district neighbourhoods where such homes are available – and options are limited to condos located away from the city core, including North York condos and Etobicoke condos.

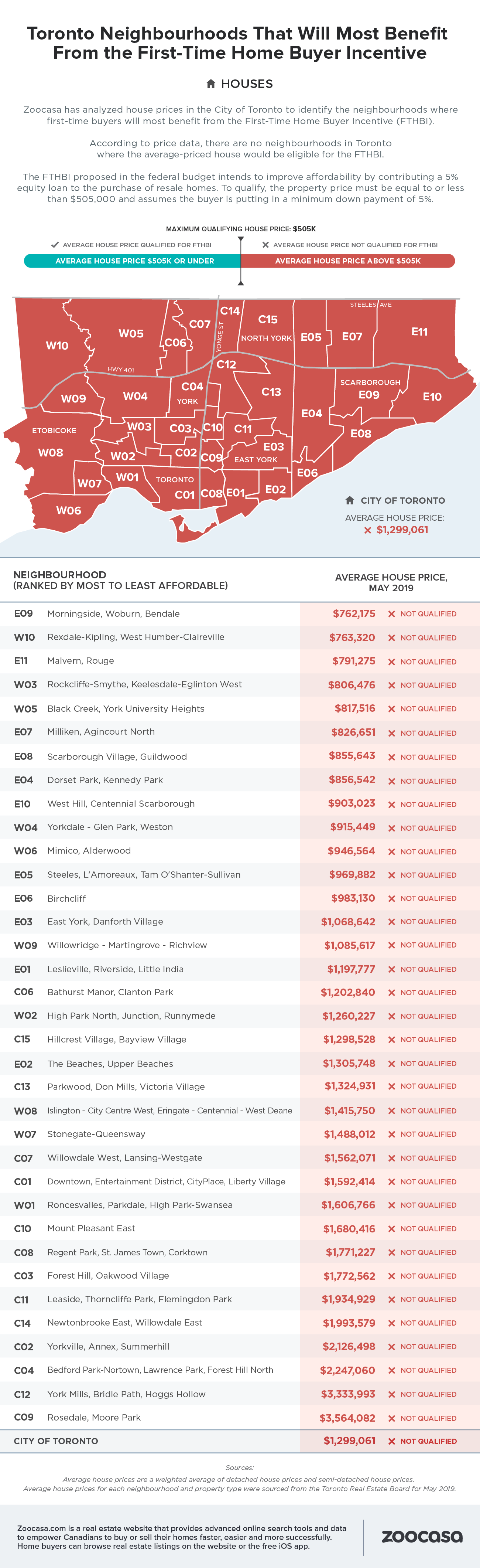

Those on the hunt for average priced houses for sale in Toronto (including both detached and semi-detached options) have zero ability to utilize the program, as the average property comes with a price tag of $1,299,061.

The study assumes a home buyer qualifies for the

Check out the infographics below to see where it’s possible to utilize the FTHBI in the City of Toronto:

Toronto Neighbourhoods Where the FTHBI Could Be Used to Buy a Condo

- E10: West Hill, Centennial Scarborough

Average Home Price: $352,389

- E11: Malvern, Rouge

Average Home Price: $362,037

- W05: Black Creek, York University Heights

Average Home Price: $373,932

- W09: Willowridge, Martingrove-Richview

Average Home Price: $374,050

- W10: Rexdale-Kipling, West Humber-Clairville

Average Home Price: $388,935

- E04: Dorset Park, Kennedy Park

Average Home Price: $397,600

- E07: Milliken, Agincourt North

Average Home Price: $423,726

- E08: Scarborough Village, Guildwood

Average Home Price: $430,104

- E05: Steeles, L’Amoreaux, Tam O’Shanter-Sullivan

Average Home Price: $437,213

- E09: Morningside, Woburn, Bendale

Average Home Price: $438,615

- E03: East York, Danforth Village

Average Home Price: $449,750

- W04: Yorkdale, Glen Park, Weston

Average Home Price: $454,470

- C06: Bathurst Manor, Clanton Park

Average Home Price: $497,967

METHODOLOGY

Condos:

Average condo apartment prices for each MLS district neighbourhood was sourced from the Toronto Real Estate Board for May 2019.

Houses:

Average house prices are a weighted average of detached house prices and semi-detached house prices. Average house prices for each neighbourhood and property type were sourced from the Toronto Real Estate Board for May 2019.

It is assumed the home buyer has the maximum eligible household income of $120,000 and has saved the minimum down payment of 5.05%, which would qualify them for an insured mortgage on a $505,000 resale home.

About Zoocasa

Zoocasa.com is a real estate website that provides advanced online search tools and data to empower Canadians to buy or sell their homes faster, easier and more successfully. Home buyers can browse real estate listings on the website or the free iOS app.