November housing markets across Canada continued to experience unseasonably strong sales and price growth – but don’t expect this hot real estate demand to continue into the new year, as the uptick will fade once new mortgage rules are in places says the Canadian Real Estate Association (CREA).

The national association reveals that, month over month, sales are up 3.9 per cent from October, and 2.6 per cent higher than last year – the fourth consecutive month to see growth, and the first year-over-year gains recorded since March. Two thirds of sales can be attributed to an unseasonably hot Toronto market, CREA reveals, where regional sales jumped 16 per cent.

The MLS Home Price Index rose 9.3 per cent from 2016, while the average sale price increased 2.9 per cent to $504,000. Excluding Toronto and Vancouver would strip out over $120,000, to $381,000.

As they did in October, CREA’s analysts continue to point to pending Guideline B-20 mortgage rules, which take effect on New Year’s Day. These new regulations will require all new mortgage borrowers be stress tested regardless of their home down payment size, and are anticipated to reduce the average buyer’s affordability by 20 per cent.

“Some home buyers with more than twenty per cent down payment may be fast-tracking their purchase decision in order to beat the tougher mortgage qualifications test coming into effect next year,” stated CREA President Andrew Peck. “Evidence of this is mixed and depends on the housing market. It will be interesting to see whether December sales show further signs of home purchases being fast-tracked.”

Stated Chief Economist Gregory Klump, “National sales momentum remains positive heading toward year-end. It remains to be seen whether stronger momentum now will mean weaker activity early next year once new mortgage regulations take effect beginning on New Year’s Day.”

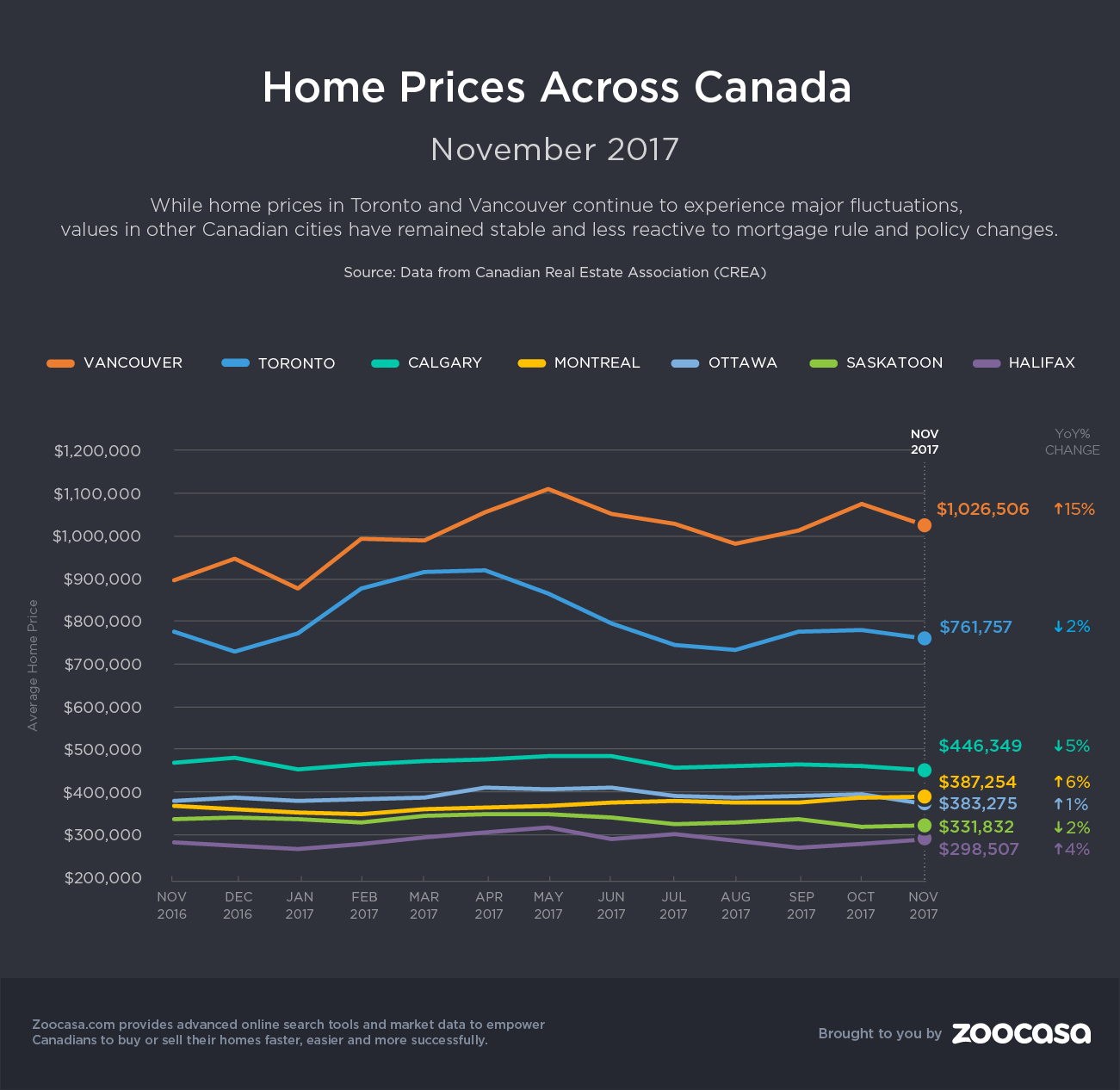

Toronto and Vancouver Buyers React to Pre-B-20

However, it appears this increased buyer urgency is concentrated on Canada’s two largest markets – Vancouver and Toronto – as other major centers experience steady sales, or slight downturns typical of the slower winter season, as seen in the infographic below:

CREA anticipates this trend will continue into 2018, as Vancouver and Toronto experience the most pain from B-20, as well as any further interest rate hikes.

“Recent research by the Bank of Canada suggests that once they come into effect, tightened mortgage rules will reduce sales activity in housing markets across Canada, particularly in and around Toronto and Vancouver,” the report states.

Balancing Market Conditions

Despite a brisker-than-usual November, market conditions remain much more balanced than at 2016’s peak, when rampant demand and historically low supply pushed prices stratospherically high. The national sales-to-new-listings ratio is currently 56.4 per cent – up very slightly from 56.2 per cent last month, and kept in check by a 3.5-per-cent increase in new homes coming to market. Nationally, the amount of available inventory tightened slightly from 4.9 months to 4.8.

(CREA considers a ratio between 40 – 60 per cent to be balanced territory, with below and above signaling buyers’ and sellers’ conditions, respectively.)

More than half of all local markets were considered balanced in November, including Greater Toronto with a ratio of 42.9 per cent – drastically lower than the 72.9 per cent recorded this time last year. Month over month, it has even leaned slightly toward buyers’ conditions from 45.2 per cent, due to a flood of newly listed homes.

Vancouver, however, remains firmly in sellers’ territory at 65.8 per cent.

Prices Rising, But at Slower Pace

While the MLS HPI rose 9.3 per cent from last year, CREA says that’s the slowest increase since February 2016, mainly due to softer sales and prices in the Greater Golden Horseshoe following the implementation of the Ontario Fair Housing Plan in April.

Condos continue to drive the majority of price growth, with values up a whopping 19.4 per cent. Townhouse prices rose 12.3 per cent, with one-storey and two-storey single-family homes increasing by single digits, at 6 per cent and 5.3 per cent, respectively.

Benchmark prices are up in 11 of the 13 tracked markets, and it’s evident the effects of previous rules and regulations to cool prices are starting to subside.

British Colombia: In Vancouver, which saw prices and sales tumble following the introduction of its Foreign Buyer’s Tax last August, prices have more than recovered and are pushing new highs at an increase of 14 per cent. Increases were strongest in the Fraser Valley at 18.5 per cent, 14 per cent in Victoria, and 18.5 per cent throughout the rest of Vancouver Island.

Greater Golden Horseshoe: While price gains have slowed considerably compared to record breaking 2016 values, they’re still above last year’s levels; prices rose 8.4 per cent in Greater Toronto, up 3.5 per cent in Oakville-Milton, and 3.5 per cent in Guelph. Anticipation to Guideline B-20 is believed to be the main impetus behind price growth and sales activity.

Oil provinces: Sales remain subdued and prices are flat due to ample inventory in the prairies, up only 0.3 per cent in Calgary, and down 3.5 and 4.1 per cent in Regina and Saskatoon.

Everywhere else: Manitoba, Eastern Ontario, New Brunswick, Nova Scotia, and PEI have seen steady sales and shrinking supply, leading to modest price growth and heating market conditions.

Check out Condos for Sale in Toronto>

A Cool Start to 2018

The reaction to the new mortgage rules and resulting short-term flurry of activity have prompted CREA to revise its forecast, as it says a temporary “pull-forward” effect could lead to a quiet first half of the year.

“… With some home buyers likely advancing their purchase decision before the new rules come into effect next year, the ‘pull-forward’ of these sales may come at the expense of sales in the first half of 2018,” states the forecast.

However, this will pick up later in 2018 as buyers who had waited to save larger down payments re-enter the market, and the impact of B-20 has been absorbed.

CREA expects sales will decline by 4 per cent to 513,900 units in 2017, with Ontario leading the slowdown due to fewer sales following the OFHP in the spring. British Columbia will record 9,000 fewer home sales, but will be offset by activity in Calgary and Quebec. The national sales price for 2017 is expected to reach $510,400, up 4.2 per cent.

However, sales will drop in 2018 by 5.3 per cent, to 486,600 – 27,000 fewer than this year, and a decline of 8,500 from what was originally forecasted. Prices are expected to fall 1.4 per cent to $503,100, as the hot demand for expensive detached homes seen in the first half of 2017 won’t be repeated next year.

“The overwhelming majority of the forecast decline in sales next year reflects an expected decline in Ontario sales, with activity anticipated to remain well below the record levels logged in early 2017,” states CREA. “Indeed, new mortgage rules are expected to lower 2018 sales in all provinces except Quebec and Newfoundland and Labrador.”