Soaring home prices in some parts of the country have made it harder for a number of first-time homebuyers looking to get into the market as it’s more difficult than ever to save enough for a down payment.

In RateHub.ca’s 2016 Digital Money Trends Report, we looked into down payment behaviour of Canadians. It showed various regional differences:

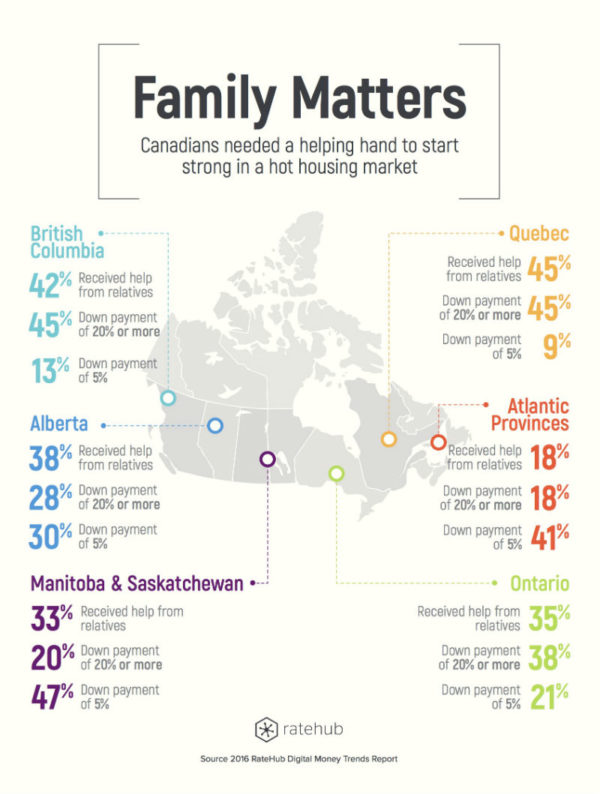

Who’s Putting 20% Down?

Residents in British Columbia and Quebec recorded the highest percentage of respondents who had a down payment of 20% or more on their first home at 45%. By contrast, residents in the Atlantic provinces (18%) were the least likely to put 20% or more down for their first home. This difference was echoed in the percentage of respondents who said they received help from relatives with their down payments. Residents in British Columbia and Quebec received the most help from relatives while residents in the Atlantic provinces received the least amount of help.

Who’s Putting 5% Down?

Respondents in Manitoba and Saskatchewan were the most likely to put 5% down for their down payment with almost half of first-time homebuyers doing so. The least likely to put 5% down were respondents in Quebec, of which only 9% put 5% down. Forty-one percent of respondents in the Atlantic provinces also had a high proportion of homebuyers put 5% down.

Where Does Ontario Rank?

Ontario seems to hover around the middle, with 35% of respondents receiving help from relatives, 38% putting 20% down compared to 21% who put 5% down. Ontario’s distribution of respondents who put 20% down compared to 5% is similar to that of British Columbia and Quebec with a higher proportion having a larger down payment.

Down Payments: 20% versus 5%

Now that we know what Canadians are putting down, what are the benefits of a 20% down payment compared to 5%? A larger down payment means your total loan value decreases. This is because your mortgage value is calculated as: home price – down payment + mortgage insurance = total mortgage required.

By increasing your down payment, you’ll be able to reduce the amount of your mortgage and save on mortgage insurance. (Getting the best mortgage rates will also help.)

Additionally, if you make a down payment of 20% or more, you’re not required to pay mortgage insurance. Mortgage insurance is required for any mortgage in which a down payment less than 20% was made. Making a large down payment of 20% or more also benefits homebuyers as they’re not affected by the new mortgage rules put in place last year, which require all insured mortgages (mortgages with a down payment of less than 20%) to be stress-tested at the Bank of Canada’s posted five-year fixed rate.

RateHub.ca is a website that compares mortgage rates, credit cards, deposit rates, and insurance with the goal to empower Canadians to search smarter and save money.