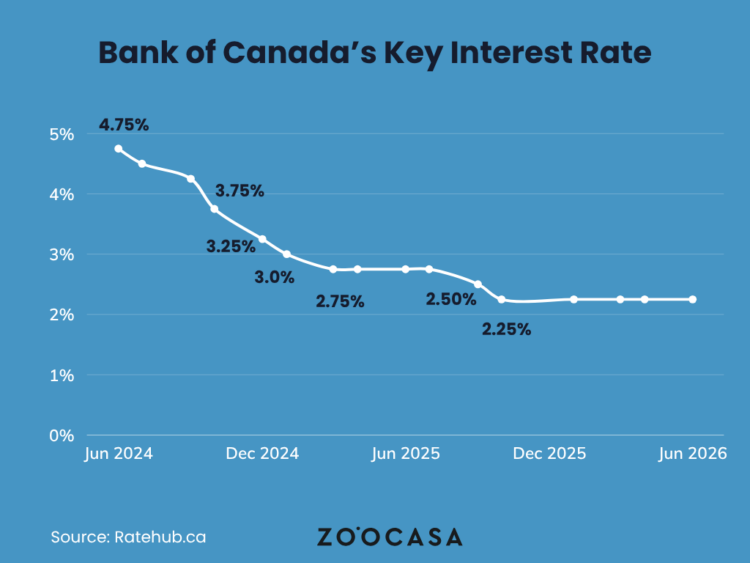

The Bank of Canada held its policy rate at 2.25% today, its sixth consecutive hold since the October 2025 cut. The decision reflects an ongoing balancing act: while economic growth is beginning to lose momentum, inflation remains uneven and somewhat stubborn.

Earlier expectations for a summer rate cut had already faded ahead of today’s announcement. Ratehub.ca’s Senior Director of Mortgages Jamie David noted that May’s inflation reading, driven higher by rising fuel and energy costs, gave the Bank little reason to consider lowering rates.

“Inflation expectations remain elevated among both consumers and businesses, while uncertainty around global trade and geopolitical tensions continues to complicate the outlook,” she said.

Variable Borrowers Bide Their Time

Mortgage rates have barely budged since June, and that stability is proving to be its own kind of relief after two years of whiplash. That matters because renewal shock has hit hard: according to CMHC’s 2026 Mortgage Consumer Survey, 35% of renewers faced greater financial pressure from rate changes, with monthly payments rising by an average of $375.

“Fixed mortgage rates have settled into a relatively stable range, as the 5-year Government of Canada bond yield continues to hover around 3%,” David said. “While lenders aren’t broadly lowering rates, competition remains strong, with some discounted options now available below the 4% mark.”

Right now, some of the more competitive offers on the market include two- and three-year fixed rates at 3.89% and a five-year fixed rate around 3.94%, the lowest levels since early spring.

Are Buyers Actually Ready to Jump Back In?

Stable rates are one thing, but buyer confidence is another. Even with borrowing costs holding steady, day-to-day cost pressures are still shaping how Canadians spend, and that caution is bleeding into how they think about buying a home.

According to a survey by TD Bank, many households are trimming their summer budgets to make room for essentials. Among those cutting back, 40% point to higher transportation costs, while 62% said they’re prioritizing groceries, fuel, and housing over discretionary spending.

That same hesitation shows up in a recent RBC poll of prospective buyers. Most can see the opportunity in today’s market, but uncertainty is getting in the way of acting on it. Among Canadians planning to buy within the next two years, 75% said economic uncertainty is making them more cautious, 72% called it the biggest barrier to buying, and 67% are worried it could derail their plans altogether.

In other words, the window is open, but buyers just aren’t convinced it’s safe to climb through yet.

Market Momentum Builds Despite Rate Pause

Despite the caution, several major markets posted real gains in June. The Vancouver Real Estate Board reported sales up 9.6% to 2,390, with every housing type seeing sales increases for the first time in years. Meanwhile, the Toronto Regional Real Estate Board saw a similar increase in its June report, with sales up 9.4% year-over-year to 6,770, while new listings fell 12.9% and active listings dropped 13.5%, tightening the market.

The rental market, though, is moving in the opposite direction. Canada’s average asking rent for all residential properties fell 4.3% year-over-year in June to $2,033, the 21st straight month of annual declines, according to Rentals.ca and Urbanation’s June 2026 National Rent Report.

What Comes Next for Rates and Buyers

Attention now turns to the next scheduled rate decision on Sept. 2, along with the inflation and employment data that will land beforehand. That data will determine whether a cut is still realistic before year-end.

For now, the message is one of cautious stability. Borrowing costs aren’t climbing, but they aren’t dropping meaningfully either. For many buyers, that means adjusting expectations rather than waiting for a dramatic shift.

Anyone holding out for sharply lower rates or a steep drop in home prices may want to rethink their timeline. As inventory tightens in markets like Toronto and Vancouver, opportunities may open up, but so could renewed competition. If you’re weighing a move, staying informed and having your financing ready will matter more than trying to time the exact bottom of the market.

Discover what you can afford at today’s mortgage rates. Start your search on Zoocasa to browse listings and estimate your monthly costs.

{kind=link}