Marking a continued period of stability, the Bank of Canada held its policy rate steady at 2.25% in its June announcement. By opting for another hold, the Bank is exercising strategic caution, balancing newly confirmed data on a technical recession against the threat of energy-driven inflation stemming from the war in Iran.

What the Rate Hold Means for Borrowers

On the surface, the case for rate cuts looks compelling. Canada’s economy has now contracted for two consecutive quarters, meeting the technical definition of a recession. But the Bank of Canada is not ready to move.

“That the Canadian economy has been newly minted as in a technical recession will do little to sway the Bank of Canada from its rate hold stance,” says Penelope Graham, mortgage expert at Ratehub.ca. “While the latest GDP numbers indicated the economy has contracted over the last two quarters, the headline number masks a mixed performance, and it’s already anticipated that growth will resume in April; the Bank won’t be rushing to ease interest rates while it awaits that result.”

The Iran conflict remains the central complicating factor. “However, this sluggish growth highlights the challenges the Bank has grappled with over the last year: supporting Canadians who are already struggling with a higher cost of living, and growing inflation pressures due to the war in Iran,” Graham adds. “The Bank has stated it’s willing to ‘look through’ the impact of spiking oil prices, but this particular headwind hasn’t yet resolved, and the threat of rate hikes will linger as long as the Strait of Hormuz remains closed.”

In its June report, the Parliamentary Budget Officer projects the Bank will maintain its current rate through 2026, then gradually raise it toward 2.75% in 2027. For borrowers, that means current borrowing costs are likely to remain elevated for an extended period, with the longer-term risk tilting toward higher rates rather than lower ones.

What’s Happening with Mortgage Rates

Variable rates remain the most affordable option heading into summer. Five-year variable mortgage rates are currently in the mid-3% range, making them the lowest-cost choice available in Canada. That advantage should hold as long as the Bank maintains its current stance, though borrowers considering a variable rate should have the flexibility to absorb potential increases or a clear plan to convert if needed.

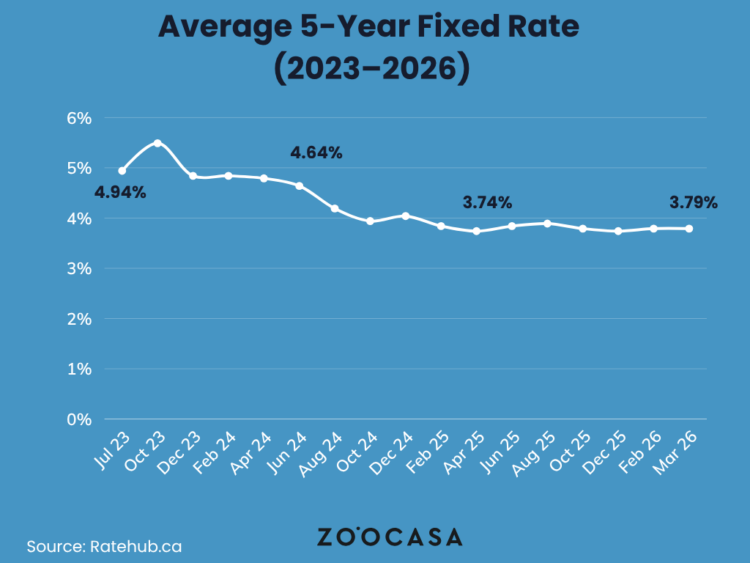

Fixed rates, however, face more pressure. Five-year insured fixed mortgage rates are sitting just above 4%, but upward pressure remains. Rising bond yields, driven by global inflation uncertainty, are prompting Canadian lenders to reprice, with the five-year Government of Canada bond yield holding near 3%.

For mortgage shoppers and those nearing renewal, Graham’s advice is consistent: prioritize protection over prediction. Securing a pre-approval and rate hold can provide up to 120 days of rate security while borrowers compare their options, a meaningful buffer in a market where conditions can shift quickly.

Canada’s Real Estate Market is Cautiously Turning a Corner

A recent RBC monthly update report suggests Canada’s housing market is stabilizing rather than rebounding sharply. Markets like Toronto and Hamilton are showing early signs of recovery, while previously strong regions in Saskatchewan, Manitoba, parts of Quebec, and Atlantic Canada appear to be peaking. Nationally, those opposing trends have largely balanced out: home sales in April came in essentially flat at approximately 426,900 units on a seasonally adjusted annualized basis, up just 0.7% from March, marking the third consecutive month of flat activity.

Graham acknowledges the push and pull at play. “While spring real estate data has shown demand is returning, economic anxiety continues to hold would-be buyers back – and a technical recession won’t help ease those concerns, especially if the next labour market report indicates a downturn in jobs. However, there is a growing narrative that Canada’s housing market may have hit its bottom in terms of affordability, and that mortgage rates are poised to rise,” she explains.

How Canadian Homeowners 45+ Are Securing Their Financial Futures

New survey findings from EQ Bank provide a useful window into how Canadian households are adapting to today’s economic environment. In a national poll of homeowners aged 45 and older, 69% said they are cutting expenses due to retirement affordability concerns, while 68% of respondents aged 45-54 reported supporting family members while trying to secure their own financial future.

Taken together, those numbers point to a cohort that is carefully managing cash flow, juggling intergenerational obligations, and making trade‑offs around spending and saving. For many, decisions about downsizing, using home equity, or helping adult children enter the market are being shaped not just by interest rates but by a broader mix of cost‑of‑living pressures, retirement timelines, and family needs.

A Narrow Window for Prepared Buyers

For motivated buyers, this summer may represent a genuine window of opportunity. Stable borrowing costs, softer prices in select segments, and a less competitive landscape are creating openings, particularly for first-time and move-up buyers who are ready to act. Rather than waiting for lower rates, the focus should shift to preparation: tightening budgets, securing a rate hold, and staying flexible on what and where to buy.

See exactly what you can afford at today’s mortgage rates. Start your search on Zoocasa to browse listings and estimate your monthly costs.