The Bank of Canada’s fifth rate announcement of this year is scheduled for this upcoming Wednesday. Although inflation was moving in the right direction in May, consumer spending remains high, causing many to assume that the overnight lending rate will reach the inevitable 5%. One of the major topics of conversation is how this continues to affect mortgage rates in Canada. New and existing homeowners have felt the brunt of higher borrowing costs, but how will this change as the year goes on, and how much will it cost you?

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

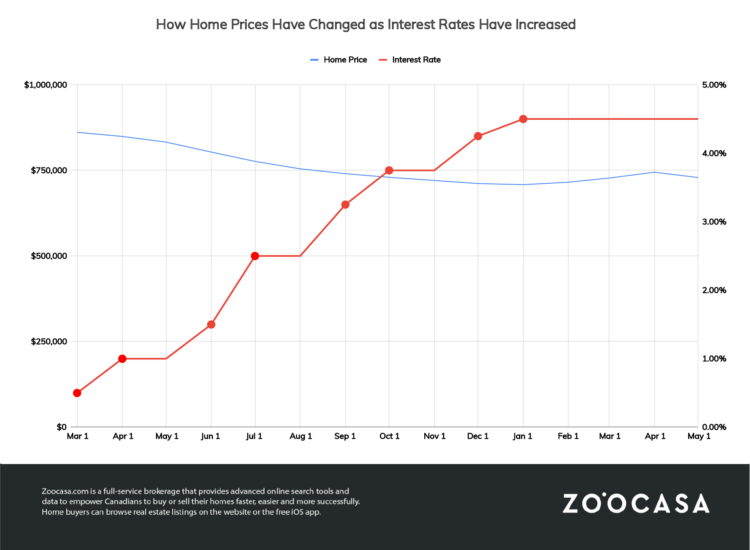

What Do Higher Rates Mean for My Mortgage?

In the simplest terms, if rates go up, your mortgage payments will as well. While those on a fixed rate have security if they’re not up for renewal, those with a variable rate will be paying more each month. For those looking to secure a mortgage this year, a fixed-rate mortgage will likely be above 5%, while variable rates will likely be up over 6.5%, and may reach close to 7%.

For example, the average price of a Canadian home is currently $729,044 according to the Canadian Real Estate Association. At an interest rate of 5%, a homeowner would pay $3,392 a month in mortgage payments on a fixed-rate mortgage. Those on a variable rate would likely end up paying more in the short term, but if we do meet the Bank’s inflation target of 2%, rates could begin to decrease, meaning your mortgage payments decline as well.

A few variables could affect this later in the year. Aside from inflation, unemployment is another important factor that impacts rates. Following record levels of low unemployment in 2022, unemployment did increase in May, rising to 5.2%. The economy isn’t infallible but if you’re hoping for lower mortgage rates, don’t hang your hat on it weakening.

How High Can Rates Go?

Theoretically, rates could continue to escalate forever, however, this is extremely unlikely. The greater likelihood is that they will continue to climb until inflation is under control without damaging the economy. Assuming rates increase again this week to 5%, that number would be 100 to 200 basis points over what the Bank would consider neutral for the economy. Rising rates have already slowed real estate sales in some major Canadian markets. In June, the Toronto Regional Real Estate Board announced that prices and sales activity were down from May’s numbers.

As we move towards the fifth rate announcement of the year, preparation is key. If you’re renewing your mortgage this year or shopping for a new home, speak to a lender and secure a rate approval knowing that it’s tough to predict if rates will increase this month and/or again in September.

Our real estate agents are here to discuss how rising rates are affecting home prices in your real estate market. Give us a call today to learn more about interest rates, home prices and real estate activity.