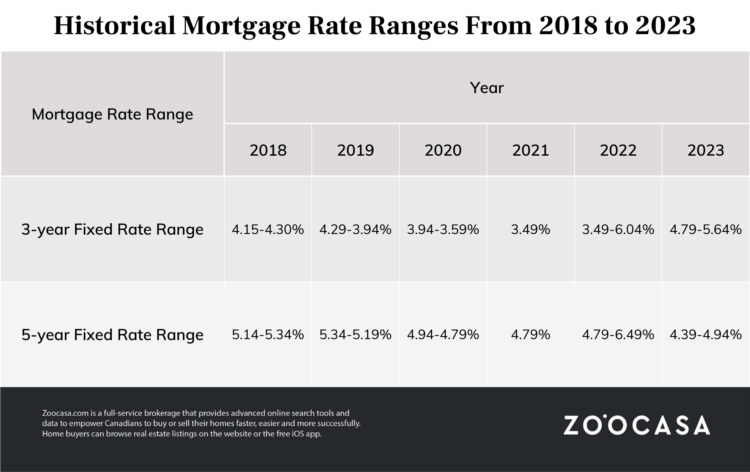

Amidst the Bank of Canada’s battle with inflation, one of the of the worst affected parties of consistent rate hikes are prospective and current homeowners. Mortgage rates continue to grow as interest rates increase, and with another announcement to come from the Bank next week, it’s easy to understand why some homeowners are nervous about renewing their mortgages.

Anyone who had a three to five-year term and is up for renewal this year is likely going to experience an increase in monthly payments as both variable and fixed mortgage rates have increased significantly during this time. The nine rate hikes since March of last year have pushed the overnight lending rate up to 4.75%.

If you are set to renew your mortgage this year, all hope is not lost. While it is likely to cost you, there are a few methods you can apply which may help you save a little in the long run.

Tips For Your Mortgage Renewal

Speak to your mortgage broker early. Ideally, you don’t want to go through the process of renewing alone and you should have a professional aid you in your search. If you’re looking to switch lenders, it’s best to start your search 120 days before renewal, as this is the earliest a lender will allow the process to begin. It can also help to speak to someone over the phone or in person as they are sometimes able to offer a loyalty or branch discount.

If you do choose to switch lenders, you will be stress tested again, likely at a much higher rate than you were last time. Alternative lenders could be an option but your rate may be higher, while other qualification requirements may help make payments more manageable.

Consider a short-term fixed rate. A fixed-rate mortgage will bring your greater stability and knowledge of consistent payments. It does mean, of course, that your payments won’t change if the lending rate decreases, but if it increases then a fixed rate will protect you from higher fees on your mortgage payments. A shorter term also means there’s potential that when it’s time for renewal again, you’ll benefit from better rates.

Extend the amortization period. You may not be locked into paying your mortgage over a 25-year period. When it comes time to renew, you can extend the amount of time it takes to pay back your mortgage, which may make your monthly costs more manageable. There are some downsides to this, however – namely that it’ll take longer to pay it off. Additionally, your equity will build slower and you’ll be paying more interest in total.

If you’d like to discuss a new or existing mortgage, give us a call. Our qualified real estate agents are eager to help you meet your real estate goals.