The Home Buyers’ Plan (HBP) is one of several tools offered by the federal government to make it easier for first-time

How Does the Home Buyers’ Plan Work?

Eligible buyers can pull up to a maximum of $35,000 from their RRSP savings for their home purchase, though if two individuals are buying together and both qualify as first-time home buyers, they can each access the maximum to a total of $70,000. To be eligible as a first-time home buyer, the Government of Canada requires that you have not owned a home, or occupied one that your spouse has owned, in the four consecutive years before this home purchase is made. (However, there are exceptions in the case of a marriage or common-law relationship breakdown where former partners can restore their first-time buyer status.)

Participants must also have a signed agreement to purchase or build a home to use the HBP and intend to dwell in it as a principal residence, living there within one year of its purchase or completion. As well, the HBP funds must be sheltered within the RRSP for a minimum of 90 days before they can be accessed. They also need to be repaid to your RRSP in annual

How Effective is the HBP?

However, using the HBP to access funds for a new home isn’t without its criticisms, in

According to Statistics Canada, while 35% of all Canadians contribute to RRSPs, they are most used by households with a major income earner bringing in $80,000 – $99,999 (50.8%), and between the ages of 35 – 54. In contrast, only 20.1% of lower-earning Canadians use RRSPs, seeming to prefer Tax-Free Savings Accounts (TFSA) instead, which come with far fewer restrictions. For example, funds put in a TFSA can come from anywhere (only earned income is eligible for an RRSP contribution) and there are no requirements to shelter funds for a minimum time period, or pay them back.

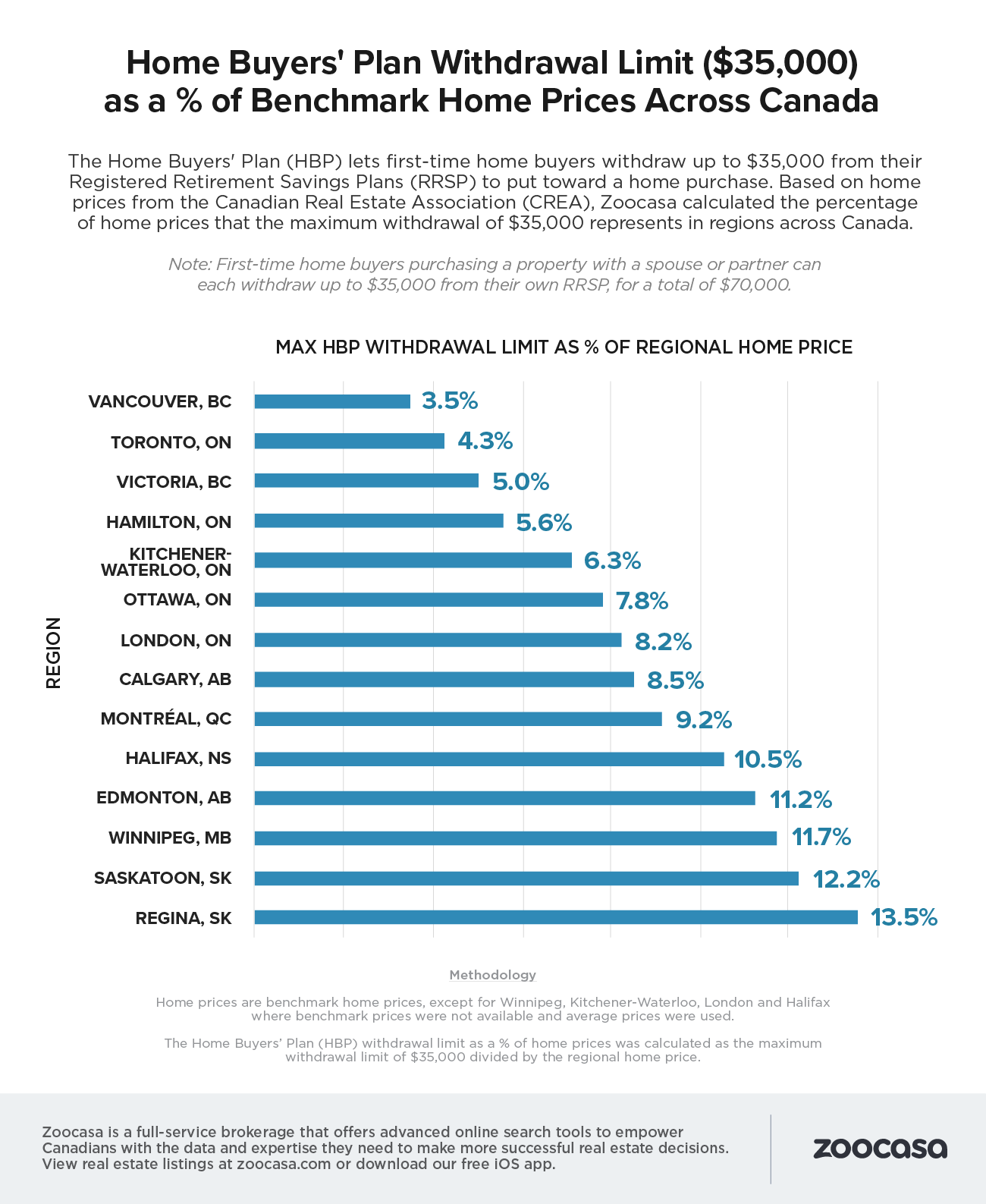

The HBP Limit as a Percentage of Local Home Prices

As well, while the federal government increased the maximum withdrawal limit to $35,000 for the HBP from the previous $25,000 in the 2019 budget, housing analysts have questioned whether this amount is enough to truly aid buyers in Canada’s largest markets.

For example, assuming a home buyer has saved and accessed the maximum $35,000 from their RRSP, that would account for just 3.5% of a home purchase in Vancouver, and 4.3% of the benchmark price for Toronto real estate – less than the minimum 5 – 7.5% down payment required to purchase a home. However, in Canada’s most affordable markets, such as in Regina, a buyer could fund up to 13.5% of their purchase with their HBP funds:

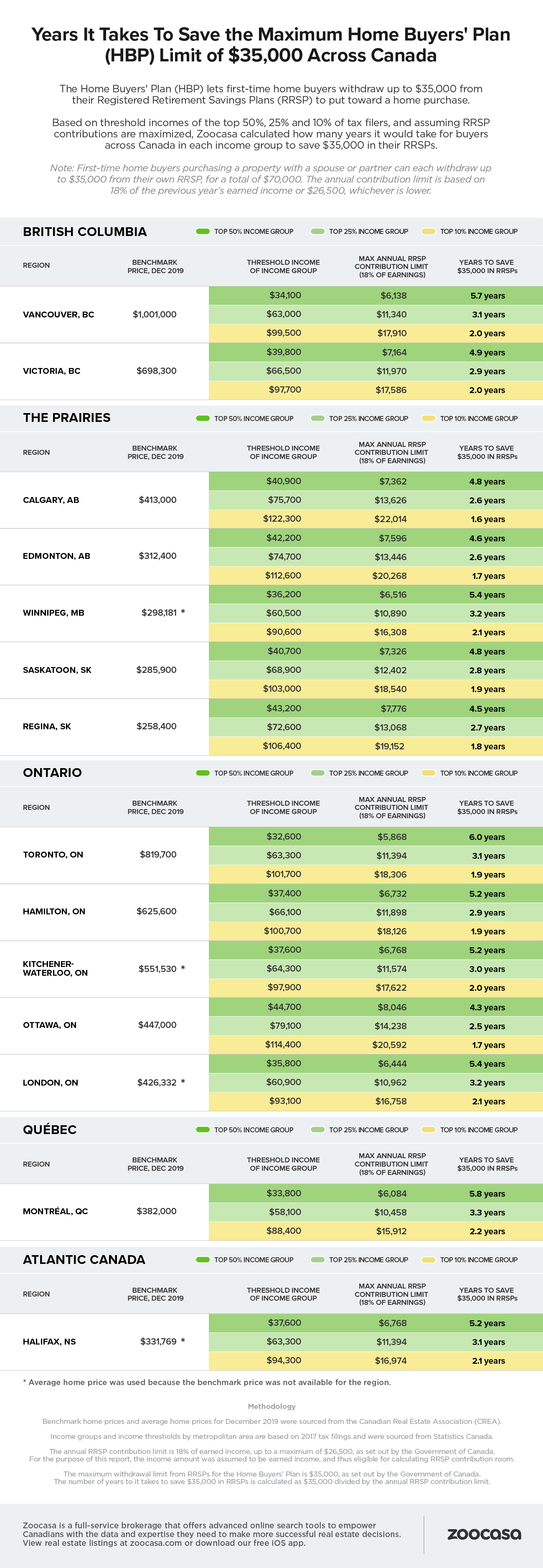

How Long Would it Take to Save the Maximum Funds for the HBP?

Using the HBP comes with the caveat that RRSP funds must be saved in the first place – not always an easy feat in markets where incomes haven’t kept pace with housing prices and other inflationary pressures.

With this in mind, how long would it actually take for

To find out, Zoocasa analyzed individual income thresholds in 14 regions across Canada, based on 2017 tax filings from Statistics Canada, assuming the income was earned income, eligible to create RRSP contribution room, and that individuals contributed the maximum to their RRSP annually (18% of earned income, to a maximum of $26,500). The study also compared how long it would take for those in the top 50%, 25%, and 10% income groups to save $35,000.

The study finds that for those earning median incomes across Canada, it would take between 4.3 – 6.0 years to save $35,000 for the HBP.

It would take those looking to buy Ottawa real estate the least amount of time to save; due to the city’s strong public service and government sectors, median incomes are higher than in other major regions at $44,700, making it possible for savers to set aside a maximum of $8,046 annually. In contrast, it would take the longest in Toronto, where the median income is comparably lower at $32,600, allowing for a maximum RRSP contribution of $5,868.

Those timelines are roughly halved for those earning within the top 25% of incomes to between 2.5 – 3.3 years. Montreal residents will be saving the longest, due to an income of $58,100, allowing for a contribution of $10,458, while the shortest timeline is again in Ottawa, with incomes of $79,100 and a maximum contribution of $14,238.

However, it would take those in the top 10% of income earners just 1.6 – 2.2 years to set aside $35,000; again, the longest timeline occurs in Montreal, with an income of $88,400 and a maximum contribution of $15,912. Meanwhile, those earning $122,300 in Calgary face the shortest timeline to put funds away, as they’re able to make a contribution of $22,014 annually.

Check out the infographic below to see how long it would take to save $35,000 in an RRSP across Canada:

Methodology

Benchmark home prices and average home prices for December 2019 were sourced from the Canadian Real Estate Association (CREA). Income groups and income thresholds by metropolitan area are based on 2017 tax filings and were sourced from Statistics Canada. The annual RRSP contribution limit is 18% of earned income, up to a maximum of $26,500, as set out by the Government of Canada.

For the purpose of this report, the income amount was assumed to be earned income, and thus eligible for calculating RRSP contribution room. The maximum withdrawal limit from RRSPs for the Home Buyers’ Plan is $35,000, as set out by the Government of Canada. The number of years it takes to save $35,000 in RRSPs is calculated as $35,000 divided by the annual RRSP contribution limit.

About Zoocasa

Zoocasa is a full-service brokerage that offers advanced online search tools to empower Canadians with the data and expertise they need to make more successful real estate decisions. View real estate listings on zoocasa.com or download our free iOS app.

For more information about this report or to set up a media interview, please contact [email protected].