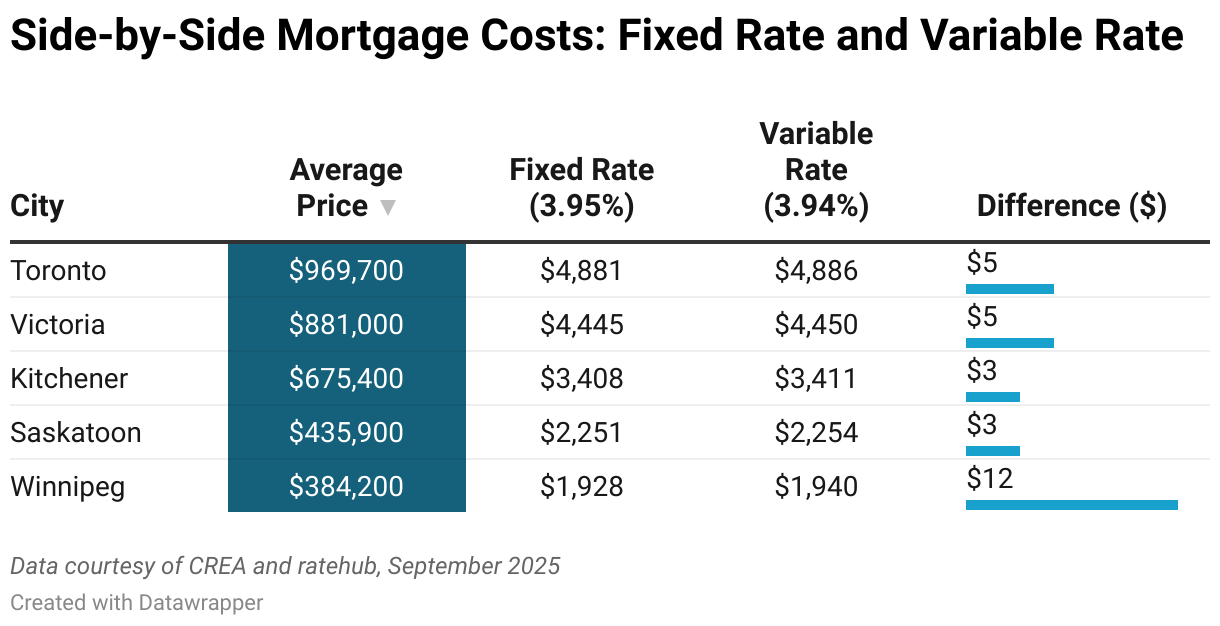

For Canadian homeowners and buyers, the question of whether to go fixed or variable is a familiar one. Yet in 2025, the decision looks different from how it has in years past. Fixed and variable mortgage rates are nearly identical, hovering around 3.94% versus 3.95%, a convergence that almost never happens. Normally, fixed rates carry a premium to reflect future uncertainty, while variable rates are priced lower to entice borrowers willing to take on economic and market risks. Here’s what this means for Canadian buyers and homeowners right now.

Why Fixed and Variable Rates Are Nearly the Same

The narrowing gap between fixed and variable rates is the product of several forces working together. Central bank stability is the priority. The Bank of Canada has shifted from aggressive tightening to signaling potential cuts, which reduces the need for lenders to price in large cushions for risk. When the central bank policy rate holds steady, both fixed and variable products move toward the middle ground.

Bond markets are also playing a central role. Since fixed rates are tied to government bond yields, recent declines in yields (driven by fears of slowing growth and cooling inflation) have pulled fixed mortgage rates down. At the same time, variable rates, which depend on the prime rate, have stayed flat because the Bank of Canada hasn’t yet made extensive cuts. Considering market volatility is muted and lenders are competing intensely in a sluggish real estate market, the result is almost no difference in pricing between the two options.

How September’s Rate Cut Might Impact You

This week, the Bank of Canada announced it is lowering the overnight lending rate by 25 basis points from 2.75% to 2.5%. It has been over three years since the overnight lending rate last stood at 2.5%, a level last seen in July 2022. That reduction would directly lower the prime rate, which in turn lowers the cost of variable-rate mortgages. Fixed rates, on the other hand, won’t react as quickly because they depend more on where bond yields move. If bond yields remain stuck above 3%, as they have in recent months, fixed mortgages could stay elevated even as variable rates decline.

The broader context also matters. Canada lost 66,000 jobs recently, pushing unemployment to 7.1%. With economic momentum slowing, the Bank of Canada faces pressure to act more aggressively to stimulate growth. If further cuts come later this year, variable rates could fall below fixed for the first time in years. That would revive their traditional advantage as the lower-cost option for borrowers willing to accept some uncertainty.

“The spread between the lowest fixed and variable rates is a scant four basis points, and it’s possible both rate types will see decreases in the coming weeks,” says Penelope Graham, mortgage expert at Ratehub.”For those deciding between the two, it comes down to risk tolerance; variable rates may offer greater savings this year, but there are still economic headwinds that could push inflation higher, which would prompt the BoC to reverse course.”

How Bond Yields Shape Fixed Mortgage Rates

In Canada, fixed mortgage rates (particularly the 5-year fixed) are directly influenced by government bond yields. Lenders establish these rates by using the 5-year bond yield as a benchmark and then adding a margin (typically 1–2 percentage points) to account for lending risk and profitability. As a result, when bond yields rise, fixed mortgage rates increase, and when bond yields decline, fixed rates become more affordable.

Bond yields themselves are driven by broader market forces, including inflation expectations, economic outlook, and central bank policy signals. For example, when investors seek the security of bonds, prices increase and yields fall, leading to lower fixed mortgage rates. Conversely, when bond prices drop, yields rise, pushing fixed rates higher.

The key takeaway is that changes in bond yields can cause fixed mortgage rates to move independently of the Bank of Canada’s policy rate—often in anticipation of future shifts. For borrowers, monitoring bond market movements provides valuable insight into where fixed mortgage rates may be headed.

Could Fixed Become Cheaper Again?

There’s always the possibility that falling bond yields could drag fixed rates down further. If economic data continues to disappoint or global shocks increase demand for safer assets like government bonds, yields could decline toward 2.5%, creating room for lenders to reduce fixed rates more meaningfully. But most forecasts suggest variable mortgages will hold the edge into late 2025 and 2026.

That said, the spread will remain narrow. The days of a full percentage-point advantage for variables are unlikely to return soon. Instead, we can expect fixed and variable rates to remain tightly linked, shifting back and forth depending on how bond markets and the Bank of Canada respond to evolving economic conditions.

When Fixed Rates Are the Safer Choice

For many borrowers, choosing fixed is less about chasing the lowest rate and more about securing peace of mind. A fixed mortgage ensures predictable payments for the entire term, which makes long-term budgeting straightforward. This option is particularly appealing for households with limited financial flexibility, those on fixed incomes, or families planning to stay in their homes for many years. Even if rates fall modestly, the cost of paying slightly more for certainty may be worth it when viewed as insurance against the unexpected.

Fixed rates also protect against the possibility that forecasts are wrong. If inflation were to spike again or global pressures forced the Bank of Canada to reverse course, borrowers locked into fixed mortgages would be shielded from payment shocks. This stability can feel especially reassuring for anyone who remembers the rapid series of hikes in 2022 and 2023.

When Variable Rates Could Be the Smarter Bet

Variable mortgages, however, offer a different kind of value. If the Bank of Canada continues cutting rates into 2026, variable borrowers will see their payments drop almost immediately, creating potential savings over the life of the mortgage. This makes variables especially attractive to borrowers who have financial breathing room, are comfortable with some level of risk, or are confident that central bank easing will continue.

Variable mortgages also come with structural advantages. Penalties for breaking them are usually lower than for fixed mortgages, which can matter if you plan to move, refinance, or pay down your mortgage aggressively before the end of the term. Many variable products also allow conversion to a fixed rate mid-term without penalty, giving borrowers the flexibility to adapt if conditions change. For those who don’t mind monitoring the market, a variable can be a strategic choice with built-in flexibility.

What History Tells Us About Fixed vs. Variable

Looking back provides some useful perspective. Between the 1950s and 2000, Canadian homeowners would have saved money with a variable mortgage about 90 percent of the time. After the 2008 financial crisis, central banks cut rates sharply, and variables once again offered borrowers significant savings. During the pandemic, variable rates fell to extraordinary lows (as little as 0.88%) while fixed rates remained higher due to bond market uncertainty.

But history also shows the risks. In 2022 and 2023, variable borrowers faced painful increases as the Bank of Canada raised rates at the fastest pace in decades. For many, payments spiked by hundreds of dollars per month, wiping out the perceived advantage of going variable. That experience is still fresh in the minds of borrowers and has made risk tolerance a more important factor than ever.