Ontario homebuyers are getting access to one of the biggest tax-saving opportunities in years. While home prices remain high, a temporary increase to the HST rebate on new construction gives first-time buyers another way to lower their costs. When combined with the First Home Savings Account (FHSA), the RRSP Home Buyers’ Plan, and Ontario’s land transfer tax refund, these programs can significantly reduce both your upfront expenses and your closing costs.

Why Buyers Are Looking For Every Advantage They Can Get

Affordability remains one of the biggest challenges facing homebuyers in the Greater Toronto Area. A Toronto Life/CityNews poll conducted in late 2025 found that 75% of non-homeowners in Toronto and the GTA believe they’ll never own a home. Most respondents also rated access to affordable housing as “bad” or “terrible.”

While many Canadians feel homeownership is out of reach, first-time buyers are still finding ways to enter the market. CMHC’s 2025 Mortgage Consumer Survey shows first-time buyers accounted for 12% of the mortgage market in 2025, up from 10% in 2024. The data also shows that buyers are waiting longer to make their first purchase. The share of first-time buyers aged 35 and older continues to grow, reflecting the longer savings timeline many Canadians now face.

Family wealth is playing a growing role in homeownership. CIBC’s mortgage application data shows that 31% of first-time buyers received financial help from family in 2024, compared with 20% in 2015. The average gift has also increased, reaching $115,000 across Canada, up 73% from 2019. Ontario buyers rely on family support even more, with 36% receiving gifts that averaged $128,000, a 52% increase over five years.

The FHSA is no longer just another government program. It’s becoming part of how many Canadians actually buy their first home. CMHC’s 2025 Mortgage Consumer Survey found that 80% of first-time buyers were aware of the FHSA, and most of them had already opened an account. More than one-third used their FHSA savings for a down payment, making it one of the most common ways buyers funded their purchase.

FHSA Basics, Refreshed for 2026

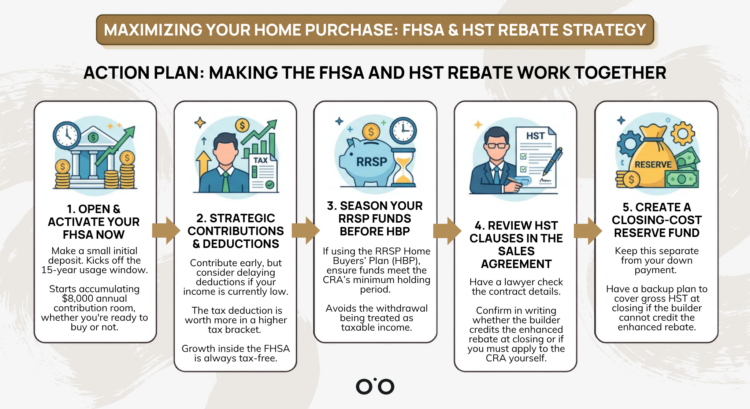

The FHSA was created to make saving for a first home more rewarding. The account combines the tax deduction of an RRSP with the tax-free withdrawals of a TFSA. According to the CRA, you can open an FHSA if you’re a Canadian resident between the ages of 18 and 71 and qualify as a first-time home buyer. That means neither you nor your spouse or common-law partner can have owned and lived in a principal residence during the current year or the previous four calendar years.

- Annual contribution limit: $8,000

- Lifetime limit: $40,000

- Carry-forward: Up to $8,000 of unused room can roll into the following year, so a buyer who contributes $3,000 in year one can contribute up to $13,000 in year two.

Canadians have been quick to take advantage of the FHSA. By the end of 2023, CRA data shows that 739,000 people had opened an account, with a combined balance of $2.79 billion. According to IG Wealth Management, that number climbed to nearly one million account holders by the end of 2024.

One of the FHSA’s most valuable features is its flexibility. Every contribution reduces your taxable income, but the tax savings depend on your marginal tax rate. Someone in a 40% tax bracket could save about $3,200 by contributing the annual maximum of $8,000, while someone in a 20% bracket would save about $1,600. If you’re just starting your career and expect your income to grow, you can still contribute now and claim the tax deduction later when it provides a bigger benefit.

If you decide not to buy a home, you can transfer the funds tax-free into an RRSP or RRIF within the account’s 15-year limit. The best part is that this transfer does not take away from your existing RRSP contribution room.

Ontario’s HST Rebate

1. The Legacy New Housing Rebate

New construction buyers can access two separate HST rebates that reduce the tax burden on a newly built home. The federal GST rebate returns 36% of the 5% GST paid, up to a maximum of $6,300, and gradually phases out for homes priced between $350,000 and $450,000.

Ontario’s provincial rebate covers 75% of the 8% provincial portion of the HST, up to $24,000, with no price phase-out. This means eligible buyers can still receive the provincial rebate even on higher-priced homes.

2. The First-Time Home Buyers’ (FTHB) GST/HST Rebate

The new GST rebate introduces one of the largest affordability incentives available to first-time buyers purchasing new construction. The federal program eliminates the 5% GST on homes valued up to $1 million and phases out for properties up to $1.5 million.

With a maximum federal benefit of $50,000 and Ontario’s matching provincial rebate of up to $80,000, eligible buyers could see substantial savings at a time when closing costs remain a major barrier to entering the market.

3. The 2026 Expanded HST Rebate

Ontario has introduced a separate, broader HST rebate program that goes beyond first-time buyers. Confirmed in the 2026 Ontario Budget, the province announced a temporary rebate covering the full 13% HST on new homes priced up to $1 million.

Unlike the first-time buyer GST rebate, this program applies to all eligible buyers, including move-up buyers and investors purchasing homes for long-term rental. The rebate applies to purchase agreements signed between April 1, 2026 and March 31, 2027.

Stacking Strategies for First-Time Buyers

FHSA + RRSP Home Buyers’ Plan (HBP)

The HBP allows first-time buyers to withdraw up to $60,000 tax-free from their RRSP to purchase or build a home, with repayment required over 15 years. Combined with the FHSA’s $40,000 lifetime limit, a single buyer can build a $100,000 pool of tax-advantaged funds. Couples who both maximize these programs could access up to $200,000 toward their purchase.

Land Transfer Tax Refunds

Closing costs can add thousands of dollars to a home purchase, but first-time buyers may be able to reduce one of those expenses. Ontario offers a land transfer tax refund of up to $4,000, and Toronto buyers may qualify for an extra municipal rebate of up to $4,475. Together, eligible first-time buyers in Toronto could save as much as $8,475 on land transfer taxes.

Regional Down Payment Assistance

Municipal programs are becoming an important part of the affordability conversation in Ontario. Brantford’s B-Home program offers qualifying first-time buyers additional purchasing power through an interest-free, 20-year forgivable loan worth 5% of the home’s purchase price.

The current maximum is about $16,710, although income thresholds and program limits may change. These local incentives can provide meaningful support when combined with broader programs like the FHSA, HBP, and HST rebates.

The Risks That Come With the Upside

The closing-day cash-flow trap. As of mid-2026, many builders have chosen not to credit the rebate at closing because updated CRA forms were still being introduced. Builders may also want to avoid the cash flow impact and potential liability if a buyer is later found to be ineligible. If the rebate is not credited at closing, buyers must pay the full HST upfront and apply directly to the CRA afterward using Form GST190.

Lenders don’t count future rebates as assets. Mortgage lenders generally require down payment funds to be in the buyer’s account and “seasoned” for at least 90 days before closing. Because of this, an expected HST rebate cannot be counted toward the required down payment.

Construction timelines matter. To qualify, construction must begin by December 31, 2028, and the home must be substantially completed by December 31, 2031. If those deadlines are missed, buyers lose access to the expanded rebate and instead qualify only for the existing rebate of up to $24,000. On higher-priced homes, that difference can exceed $100,000.

Residency rules are enforced. To keep the rebate, you or a close family member usually need to move into the home within a year of closing and live there as your primary residence for at least 12 months. If you sell, flip, or rent out the property too soon, you may have to repay the entire rebate. If you’re buying as a long-term rental investment, you’ll need to apply through the New Residential Rental Property Rebate instead, which requires a signed one-year lease.

The mortgage stress test hasn’t gone anywhere. In early 2026, OSFI confirmed that the minimum qualifying rate for uninsured mortgages remains the greater of your contract rate plus 2% or 5.25%. The rebate can reduce your upfront costs, but it does not change the mortgage stress test.

Make Your FHSA Work Even Harder

The real advantage comes from stacking available incentives. An FHSA, the Home Buyers’ Plan, land transfer tax rebates, and the expanded HST rebate can all reduce the cost of buying a home. Since some builders are not crediting the rebate at closing, buyers should confirm the process before signing an agreement.

Ready to put your FHSA and Ontario’s homebuyer incentives to work? Start your home search with Zoocasa today.