Housing affordability has long been a hot-button issue across Canada and will take centre stage in the upcoming October Federal Election as a top priority for voters. However, given the vast geographical size of the nation, and its many market nuances, buyers’ ability to purchase a home varies widely depending on local prices and incomes; in fact, the Canadian Real Estate Association has noted a growing gap between price growth in eastern and western Canada, with improved affordability concentrated in the Prairie markets, as well as parts of the Maritimes.

8 of 15 Markets Could Be Considered Affordable

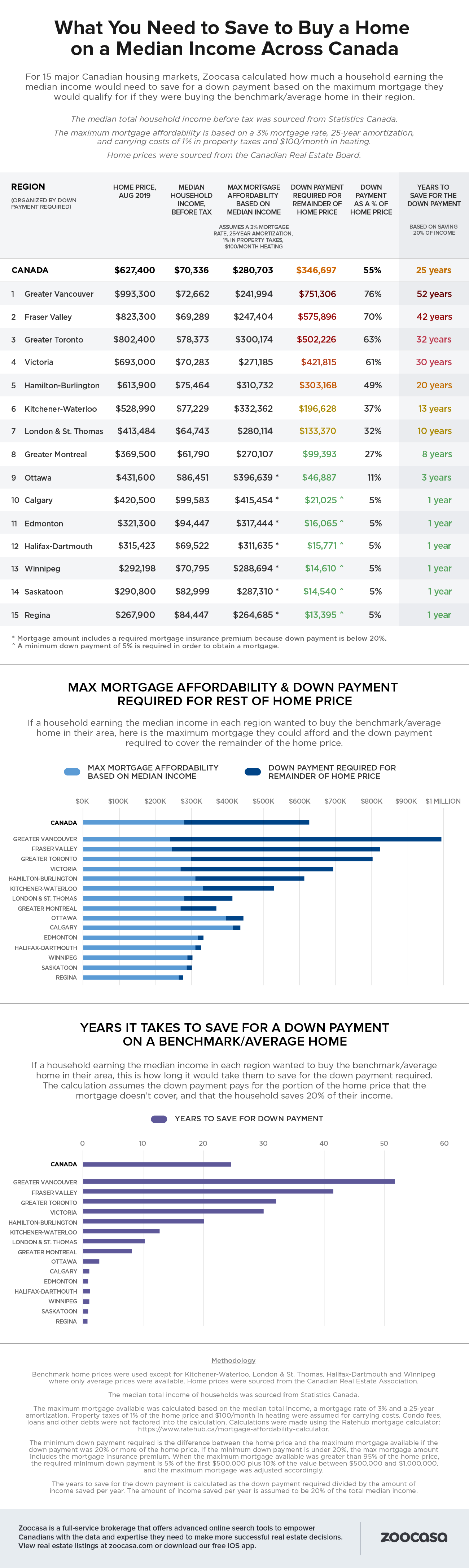

Just how feasible would it be for a household on a median income to purchase real estate in Canada? According to a new study by Zoocasa of 15 major urban centres across the country, such a household would be able to afford the local benchmark-priced home in their region in a total of eight

To determine the extent of affordability for median-income households, Zoocasa calculated the maximum mortgage they’d qualify for in each region, assuming a 3% interest rate, 25-year amortization, and that the equivalent of 1% of the total home purchase price would be put toward annual property taxes. An additional $100 per month for heating costs was also factored into the calculation.

Cities Where Median-Income Households Can Best Afford a Home

Similar to CREA’s observations, Zoocasa’s calculations reveal housing affordability is most prevalent in the Prairies, accounting for five of the most affordable markets. In these locales, home buyers with a median income would qualify for a large enough mortgage to purchase the average or benchmark-priced home, so long as they have the required minimum down payment of 5%.

Alternatively, a median income wouldn’t get far in the British Columbia and Ontario real estate markets. In Greater Vancouver, where the benchmark home price costs $993,300, a median-income household earning $72,662 would qualify for a mortgage of only $241,994, leaving a shortfall of $751,306 – a total of 76% of the total purchase price. That would take a household setting aside 20% of their income annually a total of 52 years to save the required funds. Fraser Valley and the Greater Toronto real estate markets round out the steepest three, requiring median-income households to come up with 70% and 63% of total purchase prices of $823,300 and $802,400, respectively – requiring prospective buyers save for 42 and 32 years.

Check out how housing affordability differs for median-income households in the infographic below:

Most Affordable Cities for Median Income Households

1 – Regina

Average home price: $267,900

Median household income (before tax): $84,447

Maximum mortgage: $264,685

Remaining required down payment: $13,395

Saving timeline: 1 year

2 – Saskatoon

Average home price: $290,800

Median household income (before tax): $82,999

Maximum mortgage: $287,310

Remaining required down payment: $14,450

Saving timeline: 1 year

3– Winnipeg

Average home price: $292,198

Median household income (before tax): $70,759

Maximum mortgage: $288,695

Remaining required down payment: $15,771

Saving timeline: 1 year

4 – Halifax-Dartmouth

Average home price: $315,423

Median household income (before tax) $69,522

Maximum mortgage: $311,365

Remaining required down payment: $15,771

Saving timeline: 1 year

5– Edmonton

Average home price: $321,300

Median household income (before tax): $94,447

Maximum mortgage: $317,444

Remaining required down payment: $16,065

Saving timeline: 1 year

6– Calgary

Average home price: $420,500

Median household income (before tax): $99,583

Maximum mortgage: $415,454

Remaining required down payment: $21,025

Saving timeline: 1 year

Methodology

Benchmark home prices were used except for Kitchener-Waterloo, London & St. Thomas, Halifax-Dartmouth and Winnipeg where only average prices were available. Home prices were sourced from the Canadian Real Estate Association.

The median total income of households was sourced from Statistics Canada.

The maximum mortgage available was calculated based on the median total income, a mortgage rate of 3% and a 25-year amortization. Property taxes of 1% of the home price and $100/month in heating were assumed for carrying costs. Condo fees, loans and other debts were not factored into the calculation. Calculations were made using the Ratehub mortgage calculator: https://www.ratehub.ca/mortgage-affordability-calculator.

The minimum down payment required is the difference between the home price and the maximum mortgage available if the down payment was 20% or more of the home price. If the minimum down payment is under 20%, the max mortgage amount includes the mortgage insurance premium. When the maximum mortgage available was greater than 95% of the home price, the required minimum down payment is 5% of the first $500,000 plus 10% of the value between $500,000 and $1,000,000, and the maximum mortgage was adjusted accordingly.

The years to save for the down payment is calculated as the down payment required divided by the amount of income saved per year. The amount of income saved per year is assumed to be 20% of the total median income.

About Zoocasa

Zoocasa is a full-service brokerage that offers advanced online search tools to empower Canadians with the data and expertise they need to make more successful real estate decisions. View real estate listings at zoocasa.com or download our free iOS app.

For more information about this report or to set up a media interview, please email [email protected].