The national August housing numbers are in, and they’re looking rosy; the latest data from the Canadian Real Estate Association points to sustained improvement across the country with sales up for a sixth consecutive month, prompting the board to improve its forecast for the remainder of this year and next, including a turnaround for the country’s weakest markets.

Sales are up 5% year over year with a total of 44,437 transactions, marking a 17% improvement from the market’s low in February of this year. However, activity is still about 10% short of its 2016 – early 2017 peak. The average home price rose 3.9% from 2018 to $493,000, while the MLS Home Price Index – a measure of the overall value of homes sold – edged up 0.9%.

Steady Growth to Continue Into Next Year

CREA anticipates these improvements will continue with steady sales growth throughout the remainder of this year and 2020; sales are to increase 5% and 7.5% over the next two years, respectively. That includes robust improvement in the beleaguered British Columbia market, where sales are to rise by a whopping 14.3% in 2020, as well as a 5% uptick in Alberta. The national average sale price is forecast to stabilize at 0.5% this year (compared to a previously predicted -0.6% decline), before increasing 2.1% to an average of $501,400 in 2020.

Lower Mortgage Rates Improve Stress Test Chances

CREA attributes this positive growth mainly to today’s uber-low interest rate environment, which has reduced the criteria for the federal stress test considerably; as fixed mortgage rates have been slashed by consumer lenders, that has in turn lowered the five-year benchmark rate used by the Bank of Canada to qualify prospective home buyers for mortgages. Under current rules, borrowers of new mortgages must prove they could qualify for a mortgage at this rate, or their lender rate plus 2 per cent, whichever is higher.

“The recent marginal decline in the benchmark five-year interest rate used to assess home buyers’ mortgage eligibility, together with lower home prices in some markets, means that some previously sidelined home buyers have returned,” stated Gregory Klump, CREA’s chief economist.

“Even so, the mortgage stress test will continue to limit home buyers’ access to mortgage financing, with the degree to which it further weighs on home sales activity continuing to vary by region.”

Supply Dipping Below Long-Term Average

August sales gains were actually strongest in Winnipeg – which experienced a record-setting month – and also saw promising improvement in the Fraser Valley, while Moncton saw the greatest decline in activity. The markets with year-over-year sales increases include BC’s Lower Mainland, Winnipeg, the Greater Toronto Area, Ottawa, Montreal, and Calgary real estate markets.

The supply of new listings increased 1.1%, roughly in line with sales, keeping the national sales-to-new-listings ratio (SNLR) even keel at 60.1%, up from 60% in July. That’s just on the edge of a sellers’ market, and up considerably from the long-term average of 53.6%. CREA defines an SNLR (which is calculated by dividing the number of sales by the number of new listings during the month) of 40 – 60% as a balanced market. A percentage above or below that threshold indicates a sellers’ or buyers’ market, respectively. According to this criteria, three quarters of all markets could be considered balanced in August.

However, the months of inventory – a measure of how long it would take to liquidate all available homes for sale on the market – currently sits at 4.6 months, the lowest level since December 2017, and below the long-term average of 5.3 months. As has been the case, inventory levels are split across the country, remaining much higher than typical in the Prairie provinces as well as in Newfoundland and Labrador, and much higher than usual in Ontario, Quebec, and the Maritimes. British Columbia is considered “well centred”, setting the stage for price stabilization.

BC and Prairies Starting to Improve

In fact, according to CREA, Vancouver real estate and the Prairies are already experiencing a slowdown from the price declines that have plagued these markets over the medium term, though still far from the rebounding values occurring in the Greater Golden Horseshoe markets and much of eastern Canada.

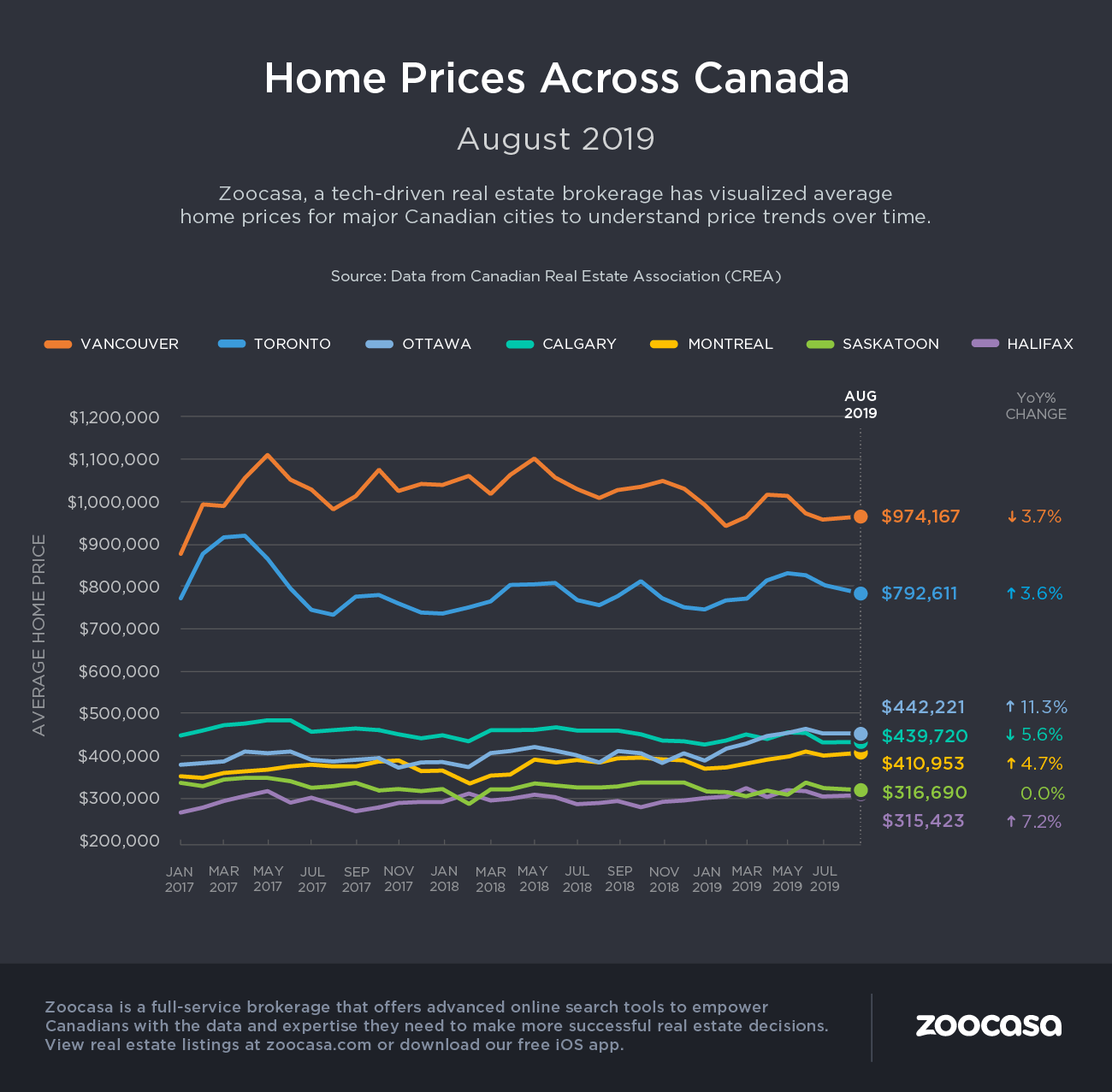

Check out the infographic below to see how prices changed in Canada’s major markets in August.