A War on Home Buyers

That’s what Ontario Real Estate Association CEO Tim Hudak has to say about the whammy of changes recently introduced to cool the housing market in Ontario and across Canada. Various levels of government have brought forth changes for borrowers and buyers, including the Fair Housing Plan, a second mortgage stress test, and rising interest rates.

It’s too much, too soon Hudak argues, saying the consequences for buyers could be heftier than policy makers intend.

“In totality, it’s war,” he stated to Huffington Post Canada, adding, “When every level of government gets in on the action, it results in an attack on home buyers.”

A better approach, he says, is to call on policy makers to focus on the supply side to temper rising prices, improve infrastructure investment and making more developable lands available for builders.

The impending stress test would require buyers with down payments higher than 20 per cent to qualify for a mortgage at a rate that’s 2 per cent higher than their actual contract rate. Those paying less than 20 per cent are already stress tested, having to qualify at the Bank of Canada’s benchmark rate of 4.84 per cent. The proposed new test could be in place as early as October, and is raising concern from all corners of the housing industry, from mortgage brokers to developers.

Mortgage Professionals Canada has forecasted that the stress test, combined with other changes, could effectively shrink sales volumes by 10 –15 per cent across Canada, while the Canadian Home Buyers Association thinks it could impact the starts of 20,000 – 30,000 new units, as well as 91,000 industry jobs.

James Laird, President of mortgage brokerage CanWise Financial, believes it could cut borrower’s financing potential by as much as 21 per cent.

Related Read: How Many Homes Can You Buy Across Canada for the Price of One in Toronto?

Real Estate Data Sharing Site Gets TREB Cease and Desist

Whether past sold home data should be public domain has been a point of contention for several years in the GTA – and an independent website has been shuttered for compiling said data by the Toronto Real Estat Board.

Financial data analyst Shafquat Arefeen was served a cease and desist from the board for utilizing two years-worth of data to illustrate market trends. The site was a hit, drawing 13,000 visits within the first month alone.

However, despite a June 2016 ruling by the Competition Bureau of Canada that TREB’s protective data practices were “anti-competitive”, the board took umbrage with Arefeen’s project. He complied, shutting the site down rather than face a legal fight.

The incident has brought fresh focus on whether market data should be gated – TREB argues that revealing the price and address of past sold homes violates the privacy of sellers, though aggregate numbers are reported publicly each month. Their recent actions have drawn criticism from intellectual property experts; IP lawyer Teresa Scassa has since written that “It is a basic and fundamental principle of copyright law that facts and information are in the public domain.”

Toronto city councillor Paul Ainslie, meanwhile, tweeted, “It’s the 21st century. Get with it.”

Part of the issue is whether Virtual Online Websites (VOWs) such as Zoocasa should be able to leverage the data to create tools and education resources to improve the experience of real estate buyers and sellers.

Full disclosure: While under previous Rogers Communications ownership, Zoocasa.com complied with a similar request to cease sharing weekly sold data updates in 2013.

Montreal Bucks Downward Trend in Luxury Home Sales

Even high rollers are pausing their real estate purchases, according to the 2017 Fall Report from Sotheby’s International Realty. In finds that, with the exception of Montreal, sales of homes above $1 million and $4 million are seeing steep declines in Canada’s largest markets.

In the Greater Toronto Area, sales of homes around the $1-million mark (an average single-detached home), have fallen 44 per cent, and by 37 per cent within the city proper over the last two months. Home sales in the above-$4-million category declined 34 and 33 per cent, respectively.

Sotheby’s International Realty President and CEO Scott Henderson told the Toronto Star that the downturn can be blamed on the unprecedented amount of new borrowing regulations coming to the market, combined with rising mortgage rates and the Ontario Fair Housing Plan. The action taken by multiple levels of government hasn’t been a co-ordinated effort and so, he argues, there’s no knowing how big the market impact will be.

“No one’s modeled what all these policies and initiatives will do to the market. They’re all coming at it from their unique vantage points of their ability to influence the market,” he says.

Recent rent control rules introduced in the Golden Horseshoe could also be stemming investor interest, states the report. Overall, sales volumes for all home types above $1 million in Toronto – including luxury condos – fell by 39 per cent to 1,926 units sold. However, despite these “policy headwinds, a brisk and active top-tier real estate market is forecast for fall,” once buyers get over the initial shock of new regulations.

Vancouver luxury sales, while showing some rebound from last year’s implementation of Metro Vancouver’s 15-per-cent foreign buyer’s tax last year, is still seeing sharp declines, with luxury sales down 23 per cent year over year in the $1-million category, and 21 per cent for homes above $4 million.

Henderson states in the report that Montreal will be this year’s breakout luxury market, and an “unexpected bright light on Canada’s luxury real estate horizon,” as job gains and a strong economy support activity in la belle provence. Sales of Montreal homes over $1 million climbed a dramatic 60-per-cent year over year in July and August, a huge uptick from the 17-per-cent increase experienced in the first half of the year.

Could the fact that the city remains unencumbered by a foreign buyers’ tax have anything to do with it? The report states that “Montreal’s luxury market remains dominated by local demand, however, industry insiders anecdotally report an uptick in interest from foreign buyers seeking residences”

6.2% of Toronto Listings are Flippers

Housing data and economy think tank Better Dwelling has analyzed the new listings that have come to the Toronto real estate market in recent months, finding a full 6.2 per cent of them were purchased less than 18 months ago. That strongly suggests speculative investor or “flipping activity”.

They also found those who may have tried to play and profit from the Toronto market haven’t been successful as of late, given the short-term sales and price softening the city has experienced since May.

“While some have ask prices that might prove profitable, we estimate one in three of these listings are currently looking at a loss,” Better Dwelling writes in the Huffington Post.

The analysis found that, across all home types, sellers waited an average of 209 days before relisting their homes, at an average ask price of $159,477 over what they originally paid. And, while the practice of flipping traditionally involves improving a home to sell it for more, very few properties had had any updates made at all – only 2.3 per cent had received renovations. The ratio was even smaller for detached homes, the most popular segment for flipping – only 0.15 per cent had renos, with unimproved properties listed at an average of $188,980 more.

“If the unrenovated unit sells for anywhere near ask, there’s very little incentive to have it renovated,” Better Dwelling writes.

Related Read: How to Profit From a House Flip

Start Up Trades Down Payment for Airbnb Profit

Would you accept a helping hand with your down payment in exchange for hosting strangers for a year? That’s the concept a Seattle-based startup is banking on: called Loftium, it gives up to US$50,000 to prospective home buyers in exchange for Airbnb short term rental income.

Home buyers must commit to listing a spare bedroom in their home for a period of one to three years in exchange for the cash, with two thirds of the profits going to Loftium. To get out of the deal, they must pay out the company the forecasted income for the remainder of contracted nights, plus a 15-per-cent surcharge.

Loftium founder, 29-year-old Yifan Zhang, told the Financial Post she came up with the idea after realizing the income potential of renting out the spare bedroom in her new Seattle townhouse. She partnered with fellow entrepreneur Adam Stelle to bring the idea to fruition, saying the arrangement is a viable alternative for aspiring buyers who don’t receive help with their down payments.

“It’s for the people who don’t have the parents to help, or the high income to save while paying rent,” she tells the Financial Post. “They are just stuck trying to save for a decade or more before they give up.”

While not yet available in Canada, Loftium is looking to expand their services to a total of four cities this year, considering Chicago, Denver, or Raleigh as potential markets.

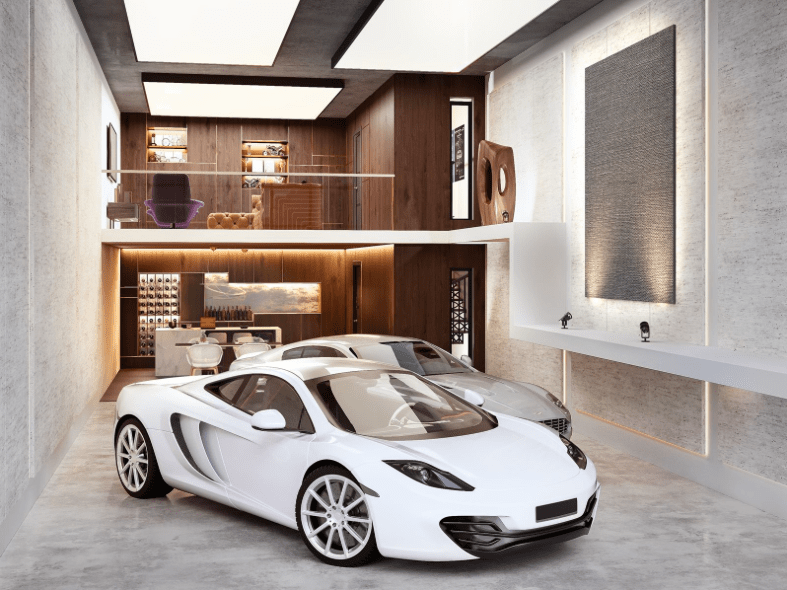

When a Garage Just Won’t Do

In a city where residential real estate is infamously unaffordable and building space is at a premium, high-income earners have a new way to showcase their wealth: high end “condo” lofts for their luxury vehicle collections.

The TROVE development, created by Hungerford Properties, is slated for completion in Richmond in 2019. It will feature 45 luxury units starting at $600,000 – and you won’t find any industrial cement facades here. Each unit includes one of four design packages (including décor and furniture from BB Italia), so Lambos and Maseratis can neighbour each other in style.

“TROVE is a smart real estate investment and a limited opportunity in commercial condo real estate in Vancouver,” stated Hungerford in a release. “Commercial condo investments provide excellent appreciation in value.”

And don’t worry – your luxury vehicle will be safe from any Gone In 60 Seconds hijinks, with gated access and 24-hours security and concierge services.

Millennial Parents Less Likely to Help Kids Buy a Home

Looks like days are numbered for the “bank of Mom and Dad”: While 51 per cent of Boomer parents with adult children financially support them in some way, that generous spirit hasn’t been passed down to the next generation. Only 43 per cent of parents of “centennials” (those born after the year 2000), plan to help out with a home purchase, compared to 65 per cent of their own parents, reports the Children and Financial Dependence Survey by the Financial Planning Standards Council.

The willingness to help kids out with a home purchase also varies by region – the survey found that Quebec parents were the least likely to provide financial home buying aid, compared to 21 per cent nationally. As well, men were reported to be 44 per cent more likely to chip in on their kids’ real estate ambitions, compared to just 32 per cent of women.