The factors fueling supply and demand in the Greater Toronto Area’s housing market widened further last month, as sales continued to slow amid a flood of new listings. As a result, prices declined in May for the first time in years, reports the Toronto Real Estate Board.

The TREB May resale numbers reveal GTA sales dropped 20.3 per cent year over year to 10,196 units with detached homes leading the slide at 26.3 per cent, and the condo market down 6.4 per cent. Active listings – the number of properties available for sale – at the end of May were up by 42.9 per cent compared to the record low a year earlier.

While home prices rose 14.9 per cent year over year, they became 6.2 per cent cheaper between April and May, the first full month-long period following the implementation of the Ontario Fair Housing Plan rules. The average sale price is now $863,910 in the region, from $752,100 in May 2016.

A Reaction to the Fair Housing Plan

TREB stated that it still remains to be seen how the changes, which included Ontario’s own 15 per cent foreign buyer tax, rent controls, and a crackdown on speculators, have impacted the market. While buyers appear to be taking a more cautious approach to the market, sellers have reacted to the Plan by listing their homes in greater numbers.

However, Jason Mercer, TREB’s director of market analysis, believes the influx of new inventory is motivated by sellers looking to cash in on years’ worth of impressive returns, rather than by fear of change in the market.

“In the past, some housing policy changes have initially led to an overreaction on the part of homeowners and buyers, which later balanced out,” he says. “On the listings front, the increase in active listings suggests that homeowners, after a protracted delay, are starting to react to the strong price growth we’ve experienced over the past year by listing their home for sale to take advantage of these equity gains.”

Related Read: Why Are Home Sales Slowing in York Region?

The Month-Over-Month Picture

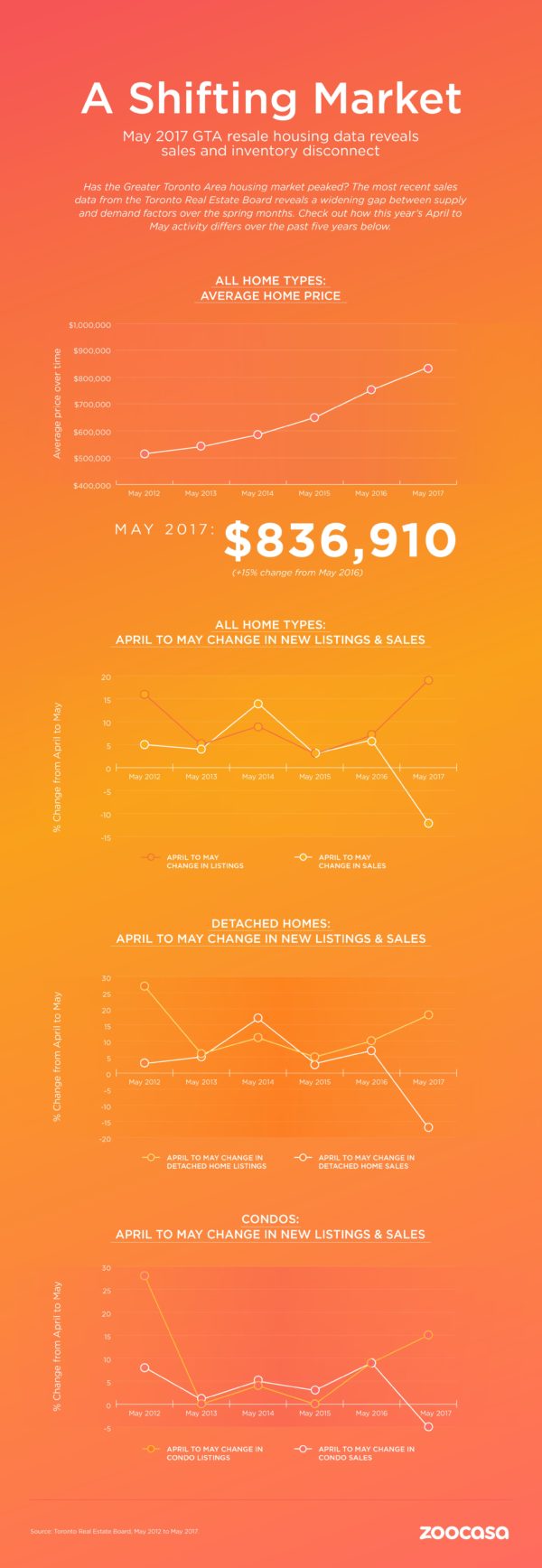

TREB’s data raises a pressing question for anyone with a vested interest in real estate – did the market reach its peak in March? While year-over-year numbers show Toronto real estate is still historically strong, a look at month-to-month data does reveal the slowest spring performance since 2013. Check out Zoocasa’s infographic of April – May month-over-month trends, between 2012 – 2017, below:

While the market always experiences a flood of listings between March and April, available homes for sale rose 27 per cent during that time period this year, before increasing a further 19 per cent from April to May. Sales, meanwhile, fell 4 per cent from March to April, and 12 per cent last month, respectively.

The detached market is feeling the brunt, with listings surging 32 per cent in April, before moderating to a softer – but still high – 18 per cent in May. The last time the detached segment fluctuated this drastically was five spring markets ago, when listings grew 28 per cent and 6 per cent. Similarly to current events, the 2013 market was reeling from hefty changes to mortgage qualification, such as mandating a minimum 5 per cent down, shortening high-ratio amortizations to 25 years, and upping required income and debt servicing ratios. The changes were found to knock a significant number of potential buyers – namely first timers – out of the market, while sellers rushed to list.

The difference between then and now, though, is that sales kept pace, increasing 31 and 5 per cents, respectively. In contrast, sales fell three per cent in April and 17 per cent in May of this year, with prices down 5 per cent.

The condo segment, while not as drastically impacted, has still seen some slight softening, with 15 per cent new listings in May, 5 per cent fewer sales, and prices down 2 per cent across the GTA region.

A Better Time to Be a Buyer

The narrative has certainly changed from March, when GTA prices rose a mammoth 33 per cent, fueling concerns of unsustainable demand that was supported by speculation rather than true buyer activity.

However, while recent increases in inventory mean buyers are enjoying greater choice on their home search, the GTA market remains firmly in sellers’ territory maintains TREB President Larry Cerqua.

“Home buyers definitely benefitted from a better supplied market in May, both in comparison to the same time last year, and to the first four months of 2017,” he said. “However, even with the robust increase in active listings, inventory levels remain low. At the end of May, we had less than two months of inventory. This is why we continue to see very strong annual rates of price growth, albeit lower than the peak growth rates earlier this year.”

Zero to five months of inventory generally signal sellers’ conditions, while five to seven months are indicative of a balanced market, says Zoocasa CEO Lauren Haw, who points out that in the medium term, the market has reached the same levels seen in the second quarter of 2016 – still extraordinarily hot price and sales growth.

“Sellers who need to do so urgently are anxious – they’re concerned they missed the window. However, prices have still gone up,” she says. Buyers, on the other hand, are increasing their “move-in ready” expectations, and maybe be less pressed to purchase a home needing renovations. “Buyers are less likely to overlook things they would later fix post-sale,” she says. “The seller needs to focus on greater preparation of the home, and great marketing, to net a great sale result.”

Drawing Parallels to Vancouver

Keep in mind, two months does not a trend make; it’s impossible to say to what extent the market is being affected by the Ontario government’s new rules specifically, or whether it’s simply reacting to change for change’s sake.

It’s tempting to look to Vancouver – which has been absorbing the impact of its infamous foreign buyers’ tax since last August – for hints as to how the dust will settle. Sales dropped 26 per cent by September, trending 3.5 per cent below the city’s 10-year average. Like Toronto, the majority of the slowdown was in the low-rise segment, with the detached market careening by 44.6 per cent year over year. In comparison, Vancouver’s condo market fell 10.1 per cent.

Stated then-Real Estate Board of Greater Vancouver President Dan Morrison at the time, “In aggregate, we continue to see an imbalance between supply and demand in most communities. However, we’re also seeing fewer detached sales in the highest price points and fewer detached home sales relative to all residential sales. This is causing average sale prices to show a decline in recent months, while benchmark home prices remain virtually unchanged from July.”

Now, Vancouver’s May numbers show a market that’s back on track to smashing price records, with a strong rebound in sales. Jennifer Oudil, current president of REBGV, says the high-rise and townhome segments are leading growth, as first time buyers and people looking to downsize compete over those housing types.

“Home buyers are beginning to have more selection to choose from in the detached market, but the number of condominiums for sale continues to decline,” she stated. The composite benchmark price reached $967,500, up 8.8 per cent year over year, and 2.8 per cent month over month.

However, it’s still a tale of two markets – a key difference between Toronto and west-coast conditions is that Vancouver supply shrank alongside sales, as nervous sellers yanked their product from the market, which kept prices stable and on an upward track.