The slower spring market continues, with another year-over-year sales decline added to the books in March.

According to the latest report from the Canadian Real Estate Association, activity throughout the nation fell 4.6% from the same time period in 2018 – a six-year low for the month, and relatively unchanged from the pace of sales in February, which rose just 0.9%. Overall, national sales remain 12% below the 10-year average, though some provinces – such as British Columbia, Alberta, and Saskatchewan – are 20% below historical norms.

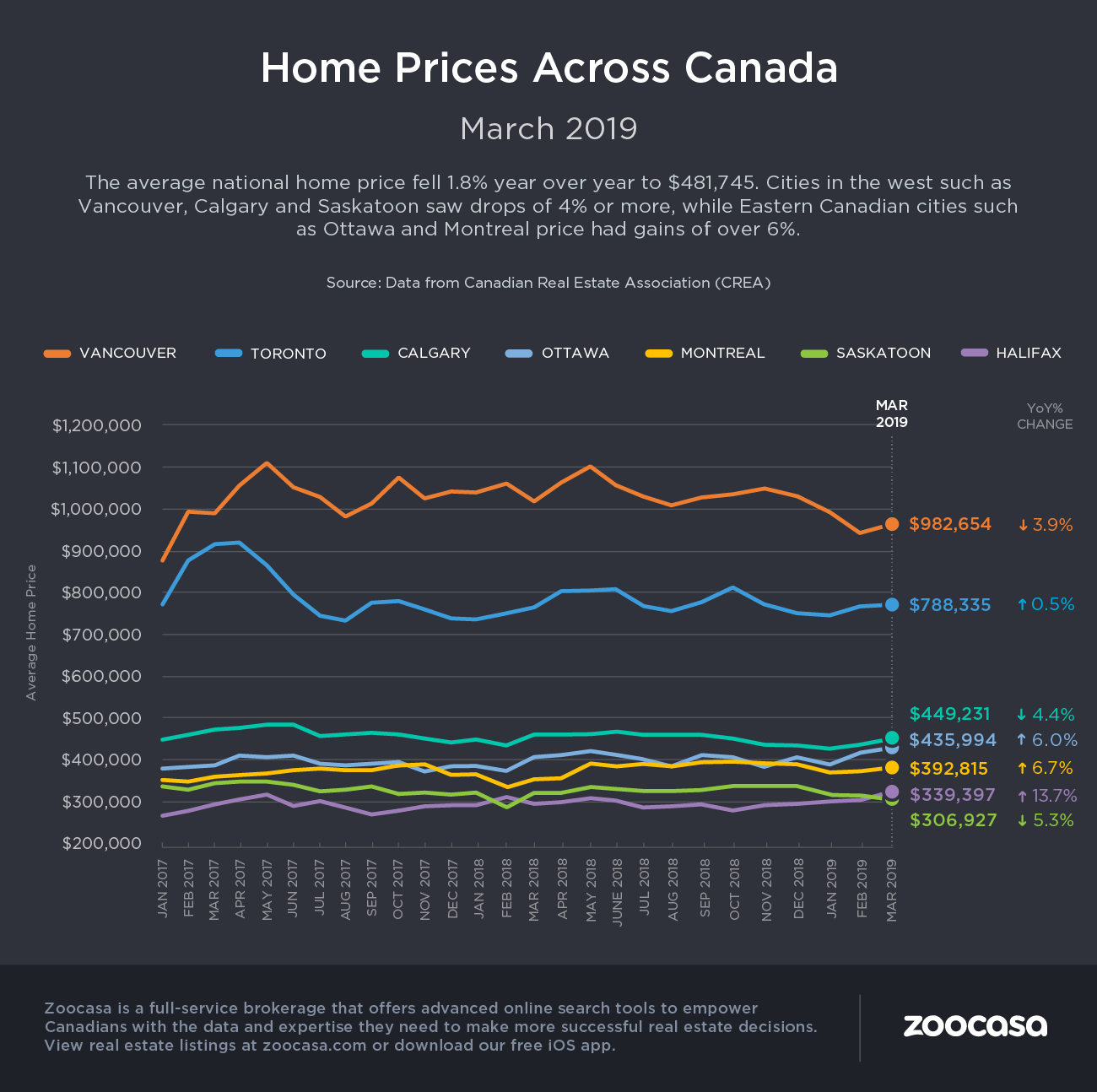

That slowing demand is now making its mark on the national home price, which dipped -1.8% to $481,745. Further, the MLS Home Price Index, which measures the value of homes changing hands, fell by 0.5%, its second consecutive monthly drop and by the largest margin since September 2009.

Market Slowdown Split Across Provinces

However, it’s not the same story across all of Canada’s market – roughly half of its urban centres, including the Greater Toronto real estate market, Oakville-Milton, Ottawa, and Victoria saw sales activity pick up, while it plunged in the Greater Vancouver real estate and Edmonton real estate markets as well as in Regina, Saskatoon, London, St. Thomas, and Quebec City.

The number of new listings also rose in

Overall, the national housing market can be considered balanced with a sales-to-new-listings ratio (

The total level of inventory – the amount of time it would take to completely sell all available homes for sale – sits at 5.6 months, a 3.5-year high, though in line with the long-term average of 5.3 months.

Still No Price Relief for First-Time Buyers

CREA’s analysts continue to point to the national mortgage stress test, which requires borrowers to qualify at an interest rate higher than the one they’ll actually pay, as the main factor behind slower real estate sales. As well, the First-Time Home Buyers’ Initiative, the mortgage equity sharing program announced last month by the federal Liberal government, is not yet in effect, postponing any potential relief for priced-out buyers.

As stated by CREA’s new President Jason Stephen, “It will be some time before policy changes announced in the recent Federal Budget designed to help first-time home buyers take effect. In the meantime, any prospective home buyers remain sidelined by the mortgage stress test to varying degrees depending on where they are looking to buy.”

However, despite these challenges, some markets remain quite competitive, due to strong job creation and wage growth. That’s continuing to support demand, and is setting the stage for a rebound in buy activity in the future, according to CREA’s Chief Economist Gregory Klump.

“March results suggest local market trends are largely in a holding pattern. While the mortgage stress test has made access to home financing more challenging, the good news is that continuing job growth remains

Price Trends by Home Type

Multi-family homes, such as apartments and condos, were the only type to see year-over-year price growth this month, up just 1.1% on average. Townhouse prices remained flat, dipping -0.2%, while one- and two-storey single-family home prices slid 1.8% and 0.8%, respectively.

Price Trends by Region

British Columbia

BC markets remain “mixed”, with Greater Vancouver experiencing a massive year-over-year drop double-digit drop in sales, pulling prices down by -7.7%. They also fell -3.9% in the Fraser Valley; this is a sharp turnaround from the stratospheric price growth experienced in these regions throughout 2016 and 2017. Prices were down -0.8% in the Okanagan Valley as well, though they rose 1% in

Ontario

All housing markets located within the Greater Golden Horseshoe are experiencing an upward tick in prices, led by Guelph with a 6.6% increase. That’s followed by Niagara Region (6%), Hamilton-Burlington (3.7%), the GTA (2.6%), and Oakville-Milton (2.3%). Barrie and District markets, however, saw price declines averaging -7.1%.

The Ottawa market continues to boom amid extremely tight sellers’ conditions, with robust year-over-year price growth of 7.6%.

Prairies

A lingering supply-and-demand imbalance, combined with a slowing economy and job market, continue to put downward pressure on Prairie housing prices; they fell -4.9% in Calgary, -4.4% in Edmonton, -2.7% in Saskatoon, and -4.6% in Regina. “The home pricing environment will likely remain weak in these cities until demand and supply become more balanced,” states CREA’s report.

Eastern Canada

The Greater Montreal market saw a strong 6.3% increase in prices, fueled by heavy investment and domestic demand, while Greater Moncton prices rose 2.1%.