Good news for those looking to break into the Canadian housing market: the new federal First-Time Home Buyer Incentive (FTHBI) will officially be open for business as of September 2nd.

Designed to alleviate mortgage costs for first-time home buyers, the FTHBI will take a bite out of monthly payments by providing shared equity loans of 5% toward the down payment of a resale home, and 5% or 10% for newly-built homes. By boosting the size of buyers’ down payments, the FTHBI whittles down monthly mortgage costs, offering some relief on the costs of

Related reads:

Who Can Use the FTHBI?

To qualify for the FTHBI, home buyers must satisfy the following:

- At least one person in the household must be a first-time

home buyer , meaning they have not owned a home, or dwelled in a home owned by their spouse, over the last four years. (An exception is made for buyers who’ve had a breakdown ofmarriage or common-law relationship.) - Buyers must have a minimum 5% down payment saved in order to qualify for an insured mortgage.

- Buyers’ combined household income cannot exceed $120,000. This includes the income of any guarantors co-signing on the mortgage, as well as any rental income generated if part of the home is tenanted out.

- The buyers’ Mortgage-to-Income Ratio (MTI) cannot exceed four times their income, including the portion that’s provided by the

FTHBI . This means the maximum down payment for a resale home cannot exceed 14.99%, and 9.99% for a new build.

How Does the FTHBI Work?

The funds provided via the FTHBI are registered as a second mortgage, and don’t incur interest. This second mortgage must be paid back in full when the first insured mortgage matures at 25 years or when the home is sold, whichever comes first, though homeowners may pay it back as a lump sum early without penalty.

Because it is a shared equity mortgage, the amount to be paid back will fluctuate along with the value of the home over time: if the home’s assessed value rises, the loan repayment will increase by the same per cent. However, the same will occur if the home has lost value by the time it is sold or the mortgage matures.

Who Will Benefit from the FTHBI?

Since its big reveal in the March 2019 budget, the FTHBI has been the subject of debate; some mortgage experts point out that borrowers taking out a traditional mortgage would actually qualify for a larger loan based on more generous MTI criteria, while others argue that home buyers could be on the hook for a much larger loan repayment if they live in a particularly hot market where real estate prices are rising.

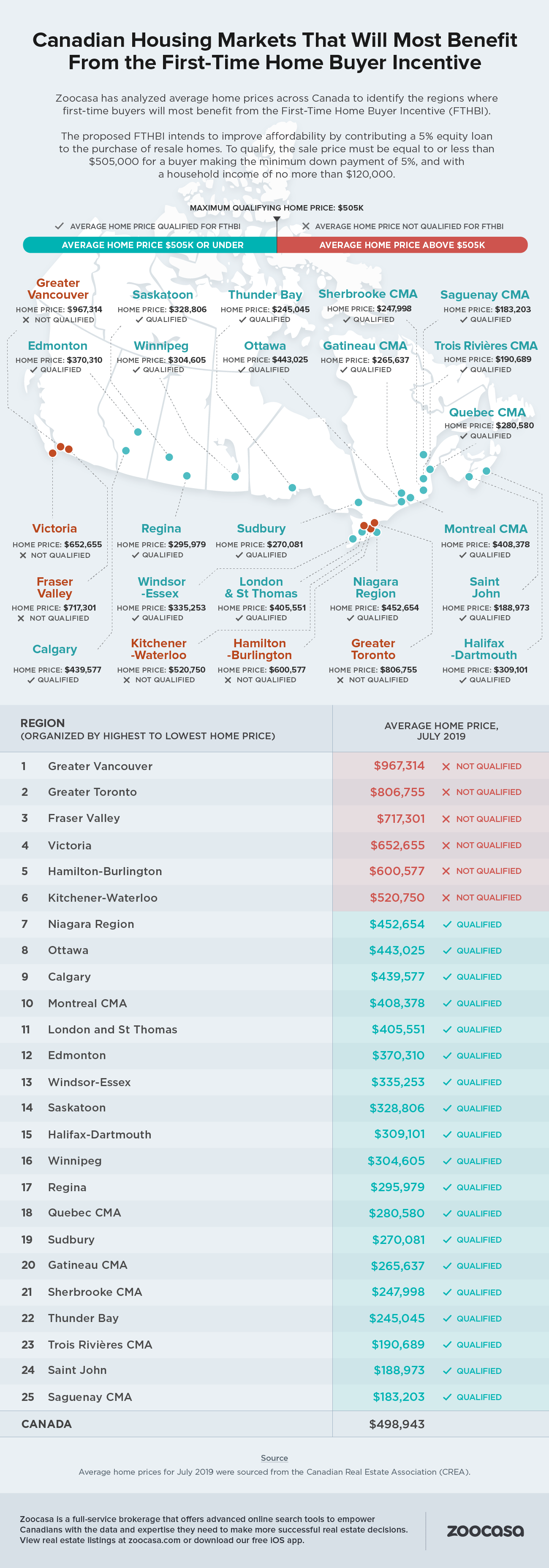

The largest points of contention are the FTHBI’s income and MTI caps; based on the criteria, a household earning the maximum income of $120,000 and making a 5% down payment would be limited to a resale home purchase price of $505,000 – an amount too low to have much traction in larger markets. For example, sold prices in Toronto and Vancouver were $806,755, and $967,314 in July, respectively.

FTHBI Could Be Used in 19 of 25 Markets

However, new analysis from Zoocasa reveals that the FTHBI may be an option in the majority of the nation’s major urban centres; a study of July 2019 average prices in 25 markets across the nation finds home buyers with the maximum income of $120,000 and a 5% down payment could feasibly qualify for the Incentive in 19 cities. These include markets in Eastern Canada, Quebec, and Prairies, as well as smaller urban centres in Ontario.

Not surprisingly, the six markets where the average home buyer would not qualify for the FTHBI include homes for sale in

However, it’s important to note that the study’s calculations are based on average home prices and maximum incomes; home buyers’ ability to use the FTHBI in each city may range based on their income, size of their down payment, and the price of their desired home.

Check out the infographic below to see where the FTHBI may be most utilized in Canada’s major cities:

Source

Average home prices for July 2019 were sourced from the Canadian Real Estate Association (CREA).

About Zoocasa

Zoocasa is a full-service brokerage that offers advanced online search tools to empower Canadians with the data and expertise they need to make more successful real estate decisions. View real estate listings at zoocasa.com or download our free iOS app.

For more information about this report or to set up a media interview, please email communications@zoocasa.com.