Peel Region, located to the west and northwest of the City of Toronto, has been a booming real estate destination in recent years, fueled by strong immigration, new home development, and its status as a transportation hub. But how affordable is the local real estate for households earning the median income across the region’s municipalities?

Peel Real Estate Largely Unattainable for Median-Income Buyers

According to new analysis from Zoocasa, housing options in Mississauga and Brampton, two of the region’s largest municipalities, are quite limited for those on such an income; with median home prices well outstripping those of incomes, such a buyer would need to pull together a hefty down payment to make up for the shortfall between purchase prices, and the actual mortgage amount they’d qualify for.

To determine housing affordability for median-income households in Peel Region, median income data was sourced from Statistics Canada, and median housing prices sourced from the Toronto Real Estate Board. The maximum mortgage amount for households in each city was then calculated assuming a 3% interest rate, 25-year amortization, 1% of the home’s cost for property taxes, and a $100-heating bill. (Condo fees, loans, and other debt obligations were not factored into the calculation.)

That mortgage amount was then compared to median home prices in each city to reveal the gap the home buyer would need to cover via a down payment. The study also crunched the number of years it would take a household to save for that down payment, assuming they set aside 20% of their income on an annual basis.

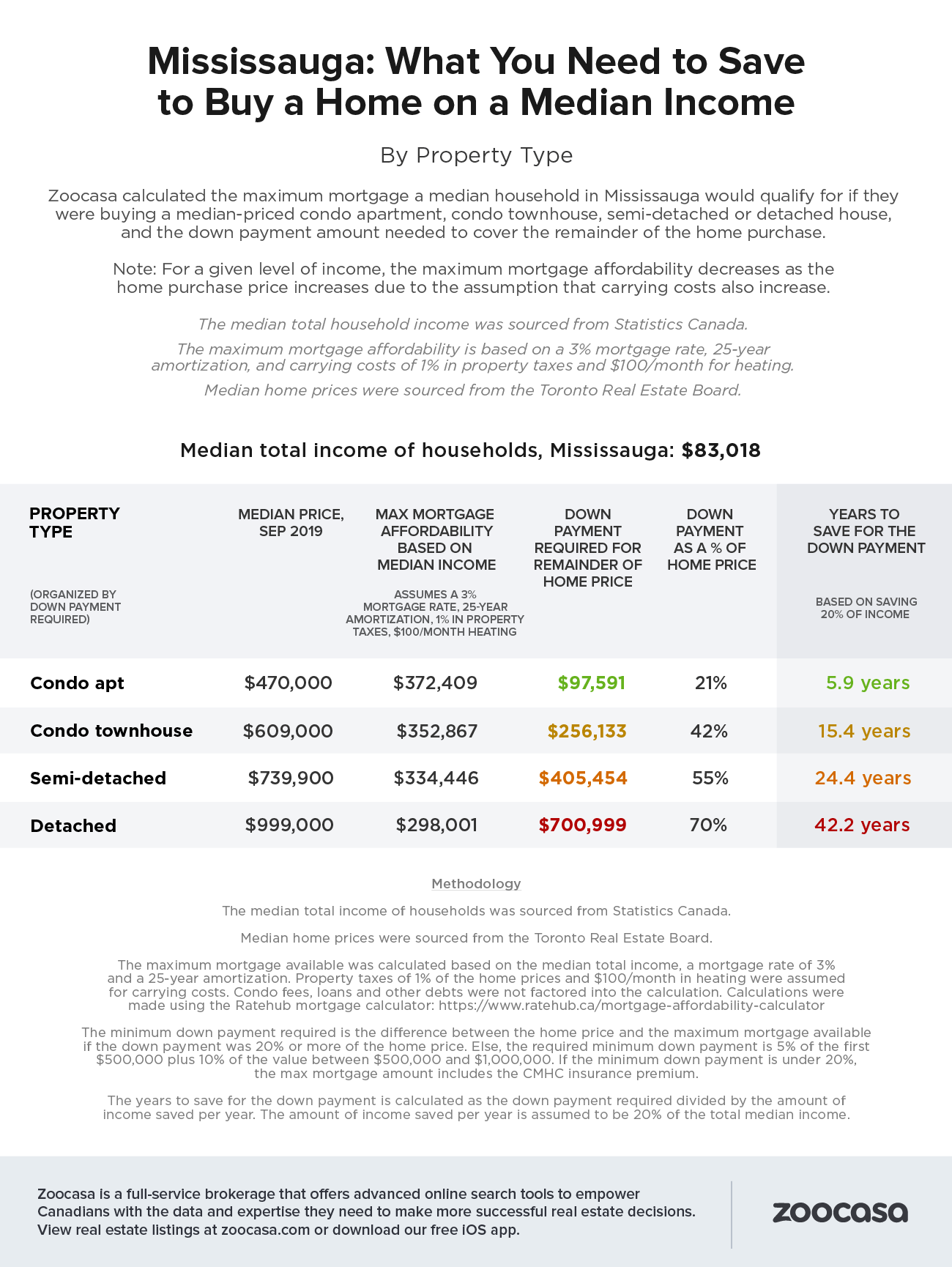

Mississauga Real Estate Well Out of Reach for Median-Income Households

The calculations reveal that in Mississauga, a household with the city’s median income of $83,018 would not be able to purchase median-priced real estate of any kind without having to save for years to amass the necessary down payment funds.

Even median prices for condos for sale in Mississauga well outpace earnings and affordability at $470,000. Such a home buyer would qualify for a maximum mortgage amount of $372,409 meaning they’d need to come up with the remaining $97,591 – an amount that would take them 5.9 years to save up.

The affordability gap only widens per home type; home buyers would also be $256,133 short on a townhouse, requiring a savings timeline of 15.4 years. As well, they’d be saving for multiple decades to afford single-family Mississauga houses, at 24.4 years for a semi-detached house, and 42.2 years for a detached house, respectively.

Sandy Dhillon, a Zoocasa sales representative with expertise working in the Peel Region notes that while the market can be competitive, first-time buyers looking for a home today will find the best freehold opportunities in the following neighbourhoods:

- Malton (townhouses, semi-detached and detached houses)

- Erindale (semi-detached houses)

- Lakeview (semi-detached houses)

Check out the latest homes for sale in Mississauga:

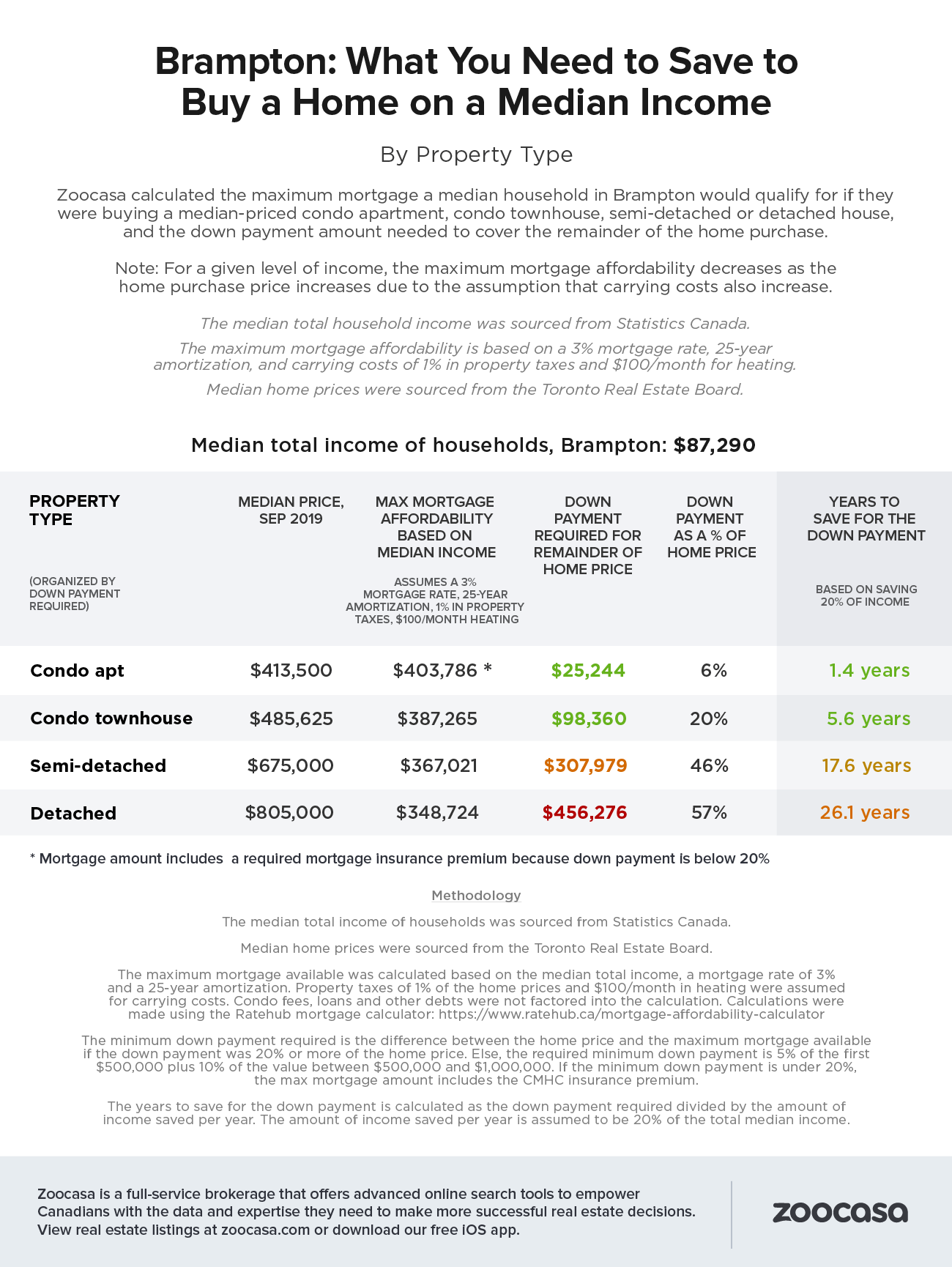

Affordability is Slightly Improved in Brampton

A slightly higher median household income of $87,290, combined with lower overall housing prices makes Brampton more accessible for aspiring home buyers, though largely still out of reach for median-income earners.

The good news for median-income households is that there are some wallet-friendly home types to be found in the city. Brampton condos remain financially accessible at a median price of $413,500; with a mortgage qualification of $403,786, buyers would need to come up with a down payment of just $25,244 – achievable within a 1.4-year savings time frame.

Townhouses could also feasibly be an option for fastidious savers, with a median price of $485,625. A median-income household would qualify for a mortgage of $387,265, leaving a gap of $98,360, which would take 5.6 years to save for. However, households would be saving 17.6 years and 26.1 years to come up with the funds for a semi-detached or detached Brampton houses, respectively.

Dhillon notes that first-time buyers looking for a home in Brampton will find the best freehold opportunities in the following neighbourhoods:

- Madoc (townhouses and semi-detached houses)

- Central Park (detached houses)

- Fletcher’s (townhouses and semi-detached houses)

Check out the latest homes for sale in Brampton:

Tips for First-Time Buyers From a Local Real Estate Agent

Dhillon offers the following tips for first-time buyers to be as successful as possible during the real estate process, particularly in competitive markets like Brampton and Mississauga:

- Always start by getting a mortgage pre-approval

- Even though you may have a sufficient income, having a pre-approval helps to set the context for your home search: when to begin search based on your budget, credit profile and down payment. This is a quick process that usually takes 3-5 days through your local bank or mortgage broker.

- Understand your monthly costs as a homeowner

- It’s important to have a clear picture of all your monthly costs including an estimate of what your new home expenses would look like (e.g. mortgage, utilities, taxes, insurance, living expenses, debt repayments). This will help you understand how feasible your budget is in owning a new home. Dhillon recommends mapping all your costs, even those that may be paid out quarterly or semi-annually or annually on a monthly basis to make your expenses seems more approachable and your savings plan more attainable.

- Have funds available – but not just for a down payment

- Work with your realtor to understand how much liquid cash you with need to have on hand to comfortably secure and close on your new home. A typical deposit ranges from $15,000 – $30,000 on a home priced between $600-$650K, due 24 hours after offer acceptance. However, keep in mind that the deposit is a part of the down payment on your home, and so you only owe the balance amount at closing. Closing costs are separate costs that need to be considered and roughly amount to 3% of the sale price. These costs cover things like title insurance, transfer of home ownership certificates, lawyer fees, land transfer taxes, etc.

- Understand key timelines and make sure they work for you

- In most cases, you don’t get possession of your home immediately after your offer is accepted by the seller. There are a few steps in between offer acceptance and getting the keys to your new home, and as such the process of closing on a home may take on average 2 weeks to 30 days or longer depending on your purchase agreement. Talk to a real estate agent as soon as you begin thinking about buying, so they can help you map out a timeline that works for you.

Methodology

The median total income of households was sourced from Statistics Canada.

Median home prices were sourced from the Toronto Real Estate Board.

The maximum mortgage available was calculated based on the median total household income, a mortgage rate of 3% and a 25-year amortization. Property taxes of 1% of the home prices and $100/month in heating were assumed for carrying costs. Condo fees, loans and other debts were not factored into the calculation. Calculations were made using the Ratehub mortgage calculator: https://www.ratehub.ca/mortgage-affordability-calculator.

The minimum down payment required is the difference between the home price and the maximum mortgage available if the down payment was 20% or more of the home price. Else, the required minimum down payment is 5% of the first $500,000 plus 10% of the value between $500,000 and $1,000,000. If the minimum down payment is under 20%, the max mortgage amount includes the CMHC insurance premium. The years to save for the down payment is calculated as the down payment required divided by the amount of income saved per year. The amount of income saved per year is assumed to be 20% of the total median income.

About Zoocasa

Zoocasa is a full-service brokerage that offers advanced online search tools to empower Canadians with the data and expertise they need to make more successful real estate decisions. View real estate listings at zoocasa.com or download our free iOS app.

For more information about this report or to set up a media interview, please email [email protected].