Unlike 2021 and 2022, when real estate activity was turbulent and competitive, the 2023 real estate market was less volatile and intense. The 2023 market showed a stronger adherence to traditional seasonal trends, meaning there was a hot spring and summer market followed by a quiet fall and winter. High borrowing costs kept many would-be buyers and sellers out of the market for much of the year, however, resulting in only 443,511 homes trading hands in 2023 – down 11.1% from 2022 and -33.5% from 2021. This marks the lowest annual level for national sales since 2008, according to the Canadian Real Estate Association.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

Month-over-month, December national sales dropped -24.2% from November to 22,628 sales, while year-over-year December sales were actually up by 3.7%.

“Was the December bounce in home sales the start of the expected recovery in Canadian housing markets? Probably not just yet. It was more likely just some of the sellers and buyers that were holding onto unrealistic pricing expectations last fall finally coming together to get deals done before the end of the year. We’re still forecasting a recovery in housing demand in 2024, but we’ll have to wait a few more months to get a sense of what that ultimately looks like,” said Shaun Cathcart, CREA’s Senior Economist.

Sales and Prices Continue to Drop Across the Country

Month-over-month sales plummeted for every major market in December. The majority of markets experienced a more than 20% drop in sales from November, with Saint John, Halifax-Dartmouth, Kitchener-Waterloo, and Hamilton-Burlington all down by more than 30%. Year-over-year sales activity was more of a mixed bag. The Greater Toronto Area experienced a 10.5% increase in sales from December 2022, but markets in the Prairies and West Coast fared even better. Edmonton experienced a 24.6% jump in sales from last year, while Regina, Saskatoon, and Fraser Valley also experienced significant increases.

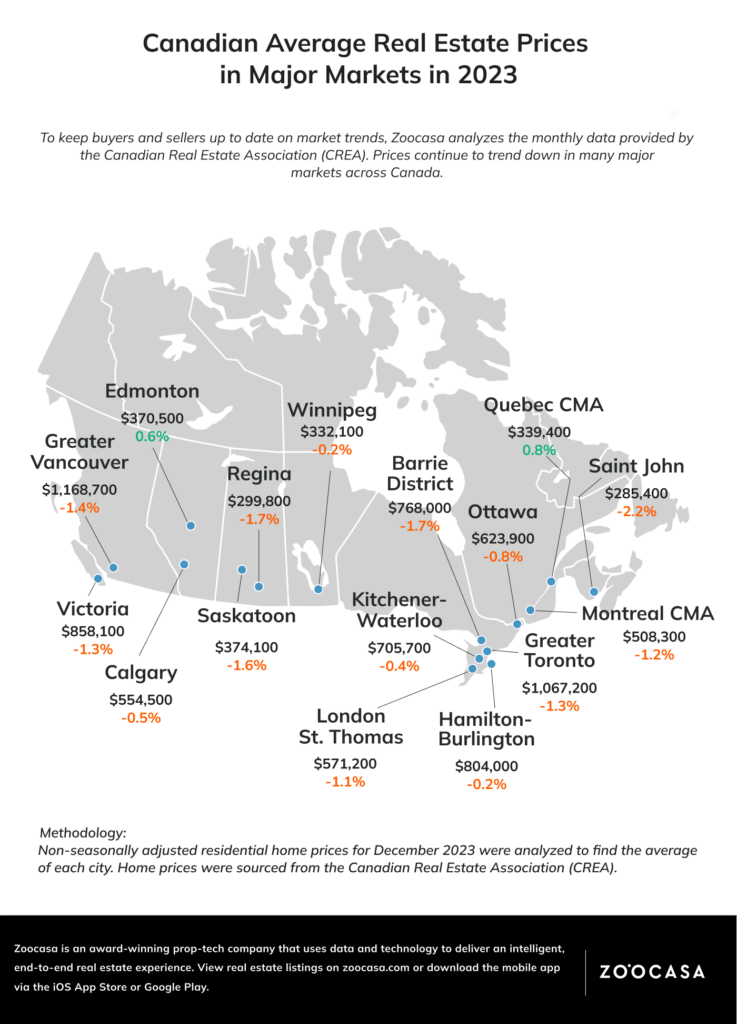

Softening month-over-month sales kept prices relatively flat across Canada, potentially creating an ideal purchasing environment for buyers who previously found the market out of reach. Saint John and Barrie District experienced the greatest month-over-month decreases at 2.2% and 1.7% respectively, while Edmonton and Quebec CMA were the only major markets to increase at 0.6% and 0.8% respectively. The national benchmark price also fell, dropping from $719,000 in November to $710,300 in December. This represents the lowest benchmark price of the year since January 2023, when the benchmark price was slightly lower at $705,000.

Inventory Shrinks Heading Into 2024

Typically, fewer sales would lead to an increase in inventory, however, with much anticipation for an active spring market, it seems sellers are holding off on listing until then. Annual new listings came in at 7.7% below 2022. Almost every major market experienced a decline in annual new listings in 2023 with several markets declining by more than 10% including Calgary, Edmonton, Kitchener-Waterloo, and Hamilton-Burlington.

Month-over-month new listings took an even greater nose-dive. New listings in Greater Toronto dropped by a whopping 63% from November to December, and Greater Vancouver’s new listings were down 61.2% month-over-month. Much of Ontario experienced similar month-over-month declines in new listings with Hamilton-Burlington down by 66.9%, Kitchener-Waterloo down by 64.5%, and Ottawa down by 61.8%.

Market conditions vary from region to region however, so if you’re planning to enter the winter or spring market, it’s important to speak with a local real estate agent to learn about conditions in your specific area. If you’re ready to talk about your 2024 real estate goals, give us a call today!