The number of available homes in Canada is still close to the lowest it’s ever been, with just 1.8 months of available inventory compared to the long-term national average of just over five months. New listings also dropped back in March, hitting a 20-year low, and with even fewer homes on the market, competition is sure to increase among interested buyers. This has left many wondering: where in Canada is the best place to buy right now, and where is the best place to sell?

Enjoying our content? Subscribe to our free weekly newsletter to get Canadian real estate market insights, news, and reports straight to your inbox.

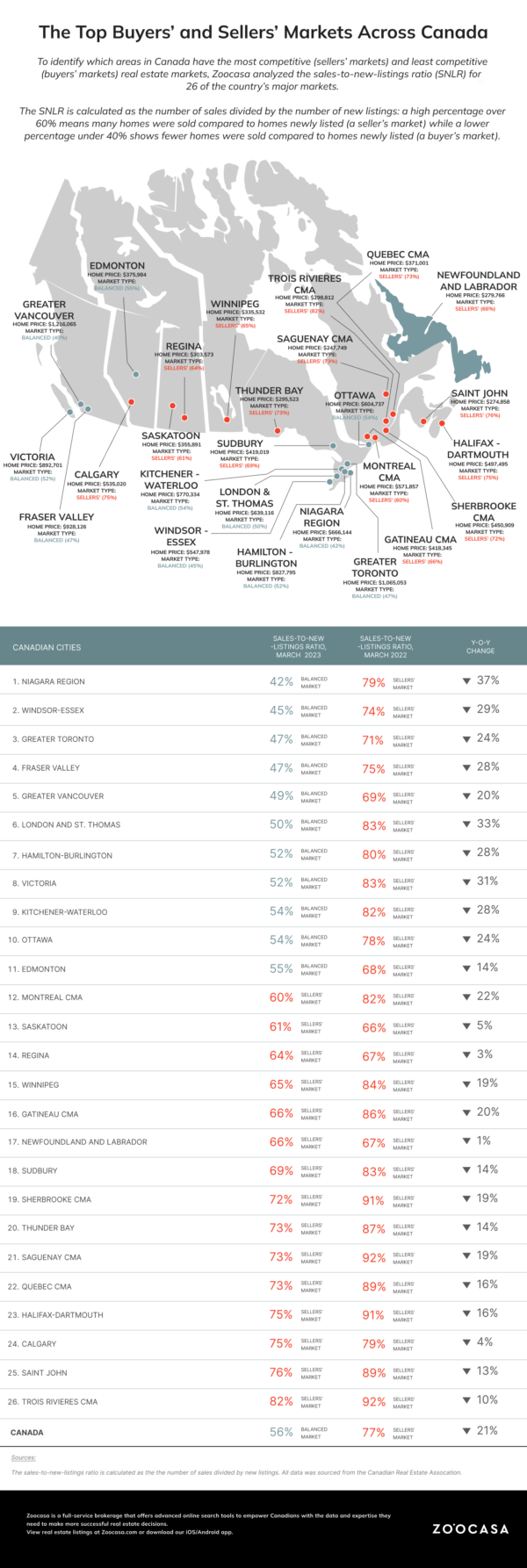

To find out, we analyzed market competition across Canada by comparing sales and new listing data for March. This data was then used to determine the sales-to-new-listings ratio (SNLR) for the month, calculated by dividing the total sales by the number of new listings in each region. The SNLR is used to effectively show the level of demand and supply in each area, and help identify how much competition local buyers face with regard to supply. The SNLR can be broken down into three percentage parameters:

- An SNLR under 40% suggests a buyer’s market: where new listings outweigh and buyers have more options

- An SNLR between 40% and 60% is a balanced market: where demand and supply are balanced

- An SNLR over 60% means a seller’s market: where demand outpaces supply, benefiting sellers

Many Canadian Markets are Favouring Sellers

According to the data, buyers would struggle to find a market in their favour. None of the markets we analyzed currently favour buyers, however 11 of the markets are in a balanced state. The closest to being in a buyer’s market is the Niagara region, with an SNLR of 42%, and an average price of $666,144. Of those 11 markets, just three have home prices below the current national average of $637,383. The other eight, including the Greater Toronto Area and Vancouver, two of Canada’s most notoriously expensive markets are above the national average. Each of those 11 markets has shifted from a seller’s market last year to a balanced market this year.

15 markets that we analyzed currently favour sellers. Each of these markets has an average price below the national average. Due to the high cost of borrowing, many buyers are seeking more affordable markets which has driven a lot of the demand. For example, Saint John currently has an average price of $274,858 and an SNLR of 76%, the second highest of the markets we analyzed. Even as prices rise, the greater affordability means buyers can stand to get more involved in a bidding war as opposed to somewhere like Vancouver where the average price is $1,216,065. In addition to this, the lack of available housing on the market means that buyers are devoid of many options.

Government Promises May Not be Enough to Solve Supply Issues

With supply so low and new listings not coming to market at the rate hoped for, inventory issues are likely to persist unless drastic changes occur. Last month, the Federal Government released its budget for 2023, and while such issues as mortgage affordability and assisting first-time buyers were addressed, plans to address the lack of available housing across Canada are still slim.

Estimates suggest that the number of available homes required to meet the demand for Canadians is between three and five million in the next ten years, particularly considering the expected influx of immigrants. The federal government has only committed to building 1.5 million homes by 2031 but the budget estimated that just 100,000 homes would be constructed every year between 2022 and 2025, barely making a dent in the required total.

If you’re looking to get into the Canadian market this year, give us a call and our agents will help you find the perfect home. Keep an eye on our market insights to learn more about real estate conditions this spring.