Today, the Bank of Canada lowered its overnight lending rate for the fourth time this year, bringing the rate down by 25 basis points to 2.25%. Hotter-than-expected inflation data and trade uncertainties contributed to the Bank’s decision.

Since January, the overnight lending rate has dropped by a total of 100 basis points. However, some economists suggest we are nearing the end of the Bank’s rate-cutting cycle. How will that impact the housing market going forward?

Banks Predict Interest Rate Activity in 2026

The Bank of Canada will likely hold the overnight lending rate around 2.25% for much of 2026, according to forecasts from some of Canada’s largest banks.

BMO is the most optimistic, predicting the overnight lending rate will lower to 2.0% by the end of 2026. CIBC and TD Bank don’t anticipate any major rate changes throughout 2026, with their forecasts seeing the rate remaining at 2.25%, while Scotiabank anticipates 2026 ending with a rate of 2.75%.

Penelope Graham, mortgage expert at Ratehub.ca, says trade negotiations will play a role in determining which direction rates head next year. “The 2026 rate outlook is less certain; the risks from the evolving trade scenario still present inflation headwinds, especially if CUSMA is not renegotiated in Canada’s favour,” says Graham. “The chance that rates could point higher again in the latter half of the year is a possibility that can’t be ruled out.”

Pent-Up Demand Should Increase Housing Activity Next Year

September housing data from the Canadian Real Estate Association (CREA) showed that although sales growth slowed from August, it was the busiest September for sales since 2021. The Toronto Regional Real Estate Board (TRREB) released similarly optimistic numbers, with September sales for the region up 8.5% from 2024 and 7.3% from August.

This is a promising sign that buyer confidence is slowly returning. As long as borrowing costs remain stable and economic uncertainties ease, momentum should continue to build for a housing market recovery in 2026.

Additionally, responses from a Zoocasa survey conducted earlier this year indicated that more affordable housing options would make prospective homebuyers more confident that they could afford a home. Fortunately, in several major markets, like Vancouver, Calgary, Toronto, and Hamilton-Burlington, average home prices are seeing year-over-year drops. This could further fuel a return from sideline buyers in 2026.

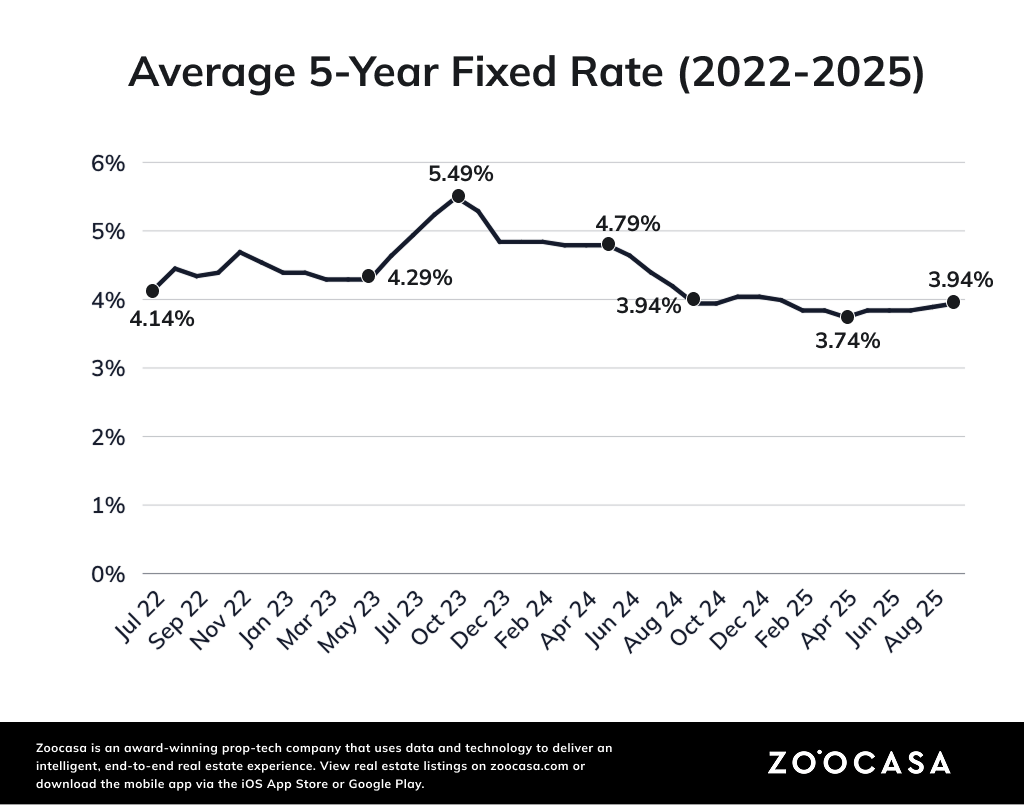

What’s Happening with Mortgage Rates

As Graham explains, expectations that the U.S. Federal Reserve will also cut rates this week — in turn pulling down Canadian bond yields — have helped keep borrowing costs low.

“Already, lenders have responded, with the lowest five-year fixed insured mortgage rate now at 3.79% — just nine basis points higher than the lowest variable-rate option,” says Graham. She advises anyone currently rate shopping to lock in a pre-approval rate in order to preserve both current rate discounts and spread to prime.

Based on the average home price of $676,154, the average mortgage payment comes out to $3,229, assuming the minimum down payment, a 25-year amortization, and a 5-year variable rate of 3.79%.

On the other hand, fixed-rate mortgage holders will pay an average of $3,480 for the same home (assuming a 5-year fixed rate of 3.79%). While variable-rate holders will currently benefit from lower monthly payments, if the Bank of Canada reverses course and raises rates in the future, payments could suddenly increase. Fixed-rate mortgage holders have the benefit of stability, which can help with long-term financial planning. Ultimately, the choice between a fixed or variable rate depends on your personal risk tolerance and financial situation.

Considering a move this year? It doesn’t hurt to start looking. Browse thousands of listings on Zoocasa and explore what’s possible in today’s market.