As anticipation grew for interest rate cuts, and affordability challenges increased, many would-be homebuyers retreated to the sidelines this year. Subsequently, spring home sales were sluggish, and enthusiasm waned. However, after four interest rate cuts by the Bank of Canada this summer and fall—most recently lowering the overnight lending rate to 3.75%—market optimism is gradually returning. Could this pave the way for a busier spring market in 2025?

We spoke with Lauren Haw, Zoocasa Broker of Record & Industry Relations Officer, to find out what we can expect from the 2025 Canadian real estate market.

A Busy, Buoyant Spring Market Is Coming

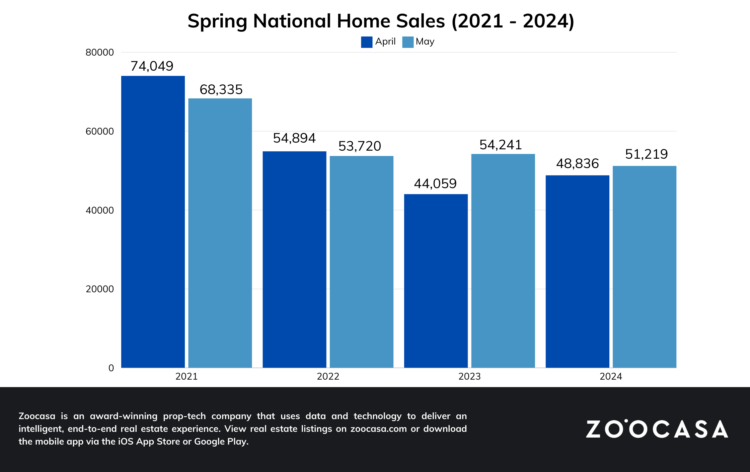

It’s been a few years since the Canadian real estate market experienced a typical spring market, with sales peaking between March and June and inventory rising to meet demand, but that may change in 2025.

“Next year, Canadians can anticipate a lively spring market kicking off as early as March,” says Haw. “With interest rates stabilizing and strong pent-up demand among buyers, we’re likely to see a return to a more traditional spring surge in real estate activity.”

According to CREA, national home sales in May 2024 were the lowest recorded for the month since 2021. On the other hand, national new listings in May 2024 were near the highs of 2021 and 2022, offering buyers more choices and reduced competition.

Buyers entering the spring market in 2025 will likely face increased competition, as many sideline buyers are expected to return. At the same time, heightened buyer activity could encourage more sellers to list their properties, potentially boosting new listings.

Mortgage Renewals Could Prompt a Wave of Downsizing

Housing supply has steadily increased throughout 2024, with national months of inventory rising from 3.6 in January to 4 months in October. At the same time, fewer buyers have entered the market compared to previous years, which has helped maintain balanced conditions in many cities. In some of Canada’s most competitive markets, such as Toronto, Vancouver, and Hamilton-Burlington, market conditions have even shifted to favor buyers.

In 2025, market conditions will be shaped by two key factors: rising demand from buyers returning to the market and the potential for increased supply from homeowners renewing their mortgages.

“There will be a lot of buyers coming off the sidelines, driving demand higher, while a wave of mortgage renewals is likely to push some homeowners to downsize, adding to supply. Although rates have recently come down, they remain significantly above the low levels of 2020 and 2021, when many of these mortgages were originally secured,” explains Haw.

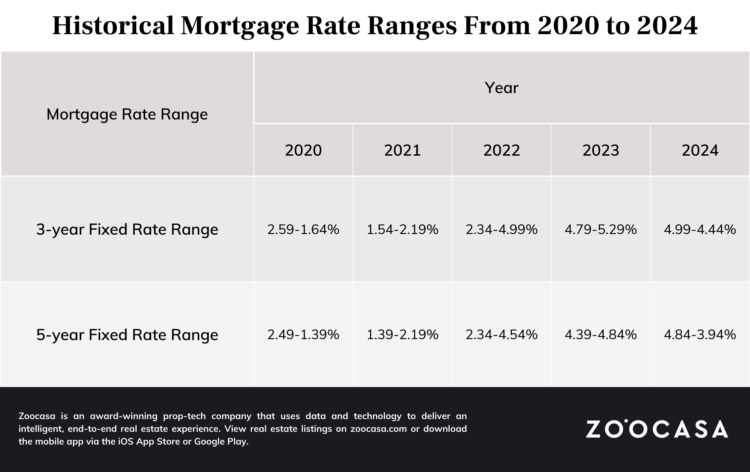

According to CMHC, 1.2 million mortgages will come up for renewal in 2025, with the majority of homeowners facing significantly higher interest rates. In 2020 and 2021, 5-year fixed-rate mortgages were as low as 1.39%, while those coming up for renewal in 2025 will likely face rates above 3%. With this in mind, some homeowners may find it beneficial to sell their current home and downsize in order to reduce their monthly mortgage costs.

FOMO May Return As a Motivator For Buyers to Act

During the pandemic years of 2020 and 2021, the Canadian real estate market was ablaze with competition, driven by buyers eager to seize what felt like a once-in-a-lifetime chance to secure a home with record-low mortgage rates.

But as many buyers learned, increased competition led to rising home prices. With mortgage rates expected to decline further next year, some homebuyers may feel even more motivated to enter the market early to avoid potential price spikes.

“First-time buyers and end-users will drive next year’s sales. With mortgage rates hovering below 4% and expectations that they may continue to fall, buyers could find themselves motivated by concerns of rising prices, potentially sparking a renewed sense of FOMO (fear of missing out) in the market,” explains Haw.

In a recent Zoocasa survey, 42.3% of respondents said that rising home prices were their primary concern regarding home buying, followed by interest rates (25.6%) and economic uncertainty (14.9%). Fortunately, average home prices in British Columbia and Ontario have been mostly flat in 2024, while average condo prices in many markets have experienced year-over-year decreases, possibly offering up a window of opportunity for buyers.

Conditions Will Be Tight for Condo Investors

In October 2024, active condo listings in Toronto rose 26% from 2023 and 90% from 2022, according to the Toronto Regional Real Estate Board. Similarly, in Vancouver, active apartment listings increased 29.3% year-over-year and 46% from 2022, according to Greater Vancouver Realtors.

This rise in supply is driven by investors listing properties as high borrowing costs make profits harder to achieve. In 2025, condo market challenges will likely persist for investors.

“Investors will continue to have a lot of supply as multi-residential mortgage renewal rates push many condos and multiplexes underwater,” says Haw. “At the same time, the challenges of making land investments financially viable continue to discourage new development.”

According to an Urbanation and CIBC Economics report, while rents on leases of newly completed condos rose 8% in 2023, average monthly ownership costs rose by 21%. Since 2020, ownership costs have climbed by almost 60%. As a result, investors are pulling back, leaving new condo sales nowhere to go but down. In Q3 2024, Urbanation reported that new condo sales in the GTA and Hamilton Area fell 81% year-over-year to 567 sales, representing the lowest quarterly total since Q1 1995.

Advice to FTHB: Get Into The Market Any Way You Can

Younger homebuyers are finding it increasingly difficult to buy real estate, especially as income growth fails to keep up with the cost of housing. In 2011, the homeownership rate for those between the ages of 25 to 39 was 38.9%, but in 2021, the homeownership rate dropped to 33.8%—the largest drop among any age group according to Stats Can.

With home prices likely to remain high for a while, where does this leave young buyers? While saving up for your forever home may be out of reach, putting a down payment on a more affordable property type (even one that needs some DIY love), could pay off in the long run, allowing you to build equity and eventually move up to a more desirable home.

“For first-time buyers, I continue to believe that the most important step is simply getting into the market and owning land. A livable but unpolished home can be a solid investment, as the value of the land will appreciate over a young person’s lifetime,” advises Haw. “Adding a basement apartment or garden suite can generate extra income or further boost the property’s value. Ultimately, it’s about owning land and building equity."

For example, if you bought a condo in London in 2019 for the benchmark price of $244,900 and sold it in 2024 for the current benchmark price of $412,300, you would have built $167,400 in equity. With $167,000, you could cover a down payment and then some on a higher-priced detached home.

Investing in a townhouse can also benefit those able to save up for a slightly larger down payment. In 2019, the benchmark price for a townhouse in Kitchener-Waterloo was $381,300, and by 2024 the benchmark price rose by 55.9% to $594,500. This results in over $200,000 of equity built. First-time home buyers should consider their long-term homeownership goals when planning to buy their first home. Thinking of your first home as just one step toward your ultimate dream home, rather than as a permanent home, can better help you climb the ladder of homeownership.

Ready to start planning for the 2025 real estate market? We’re here to help! Give us a call today to speak to a local real estate agent.