The past 24 months have ushered in dramatic change for the Greater Toronto Area housing market, from record-breaking activity in early 2017, to the sustained correction following the Ontario Fair Housing Plan. However, even as overall sales have plunged over 30 per cent from last April, condos have remained a stronghold, commanding consistent buyer demand, and the only housing type to continue to post year-over-year price increases.

Affordability is King

Condo popularity is directly connected to affordability; even accounting for softer post-FHP conditions, the average price of a detached house in the GTA clocked in at $1,045,553 in May, nearly double that of the average GTA condo price of $562,892. This has made multi-family and high-rise living increasingly attractive to move-up buyers and families – purchasers who would have been in the market for lower-density housing, such as single-detached houses or townhomes, just a few short years ago.

Growing demand from a greater buyer pool has also effectively put upward pressure on condo prices, which have surged 35 per cent between May 2016 – 2018. However, there are fewer units to go around, with available inventory falling 27.7 per cent, from 5,527 to 3,993 units, over that 24-month timeframe.

Related Read: The Most Expensive Condos in Toronto

Mid-Priced Condos Most Popular

And, as more move-up buyers comb through condo listings, demand has increased for a particular unit type – mid-priced units likely to have two bedrooms or a den, are flying off the shelves.

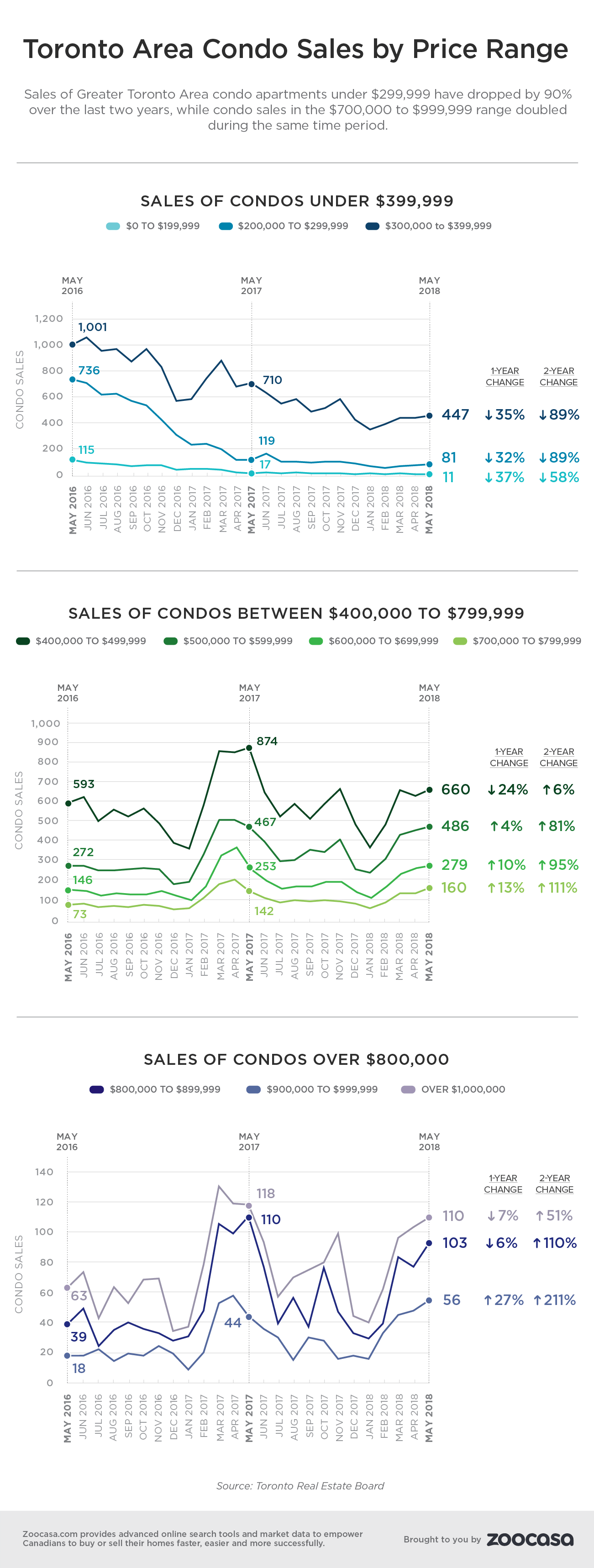

According to Statistics Canada, the median dual-or-more-income household earns $94,463, resulting in a maximum mortgage affordability of $608,590, As a result, units sales in the price range of $500,000 – $799,999 have skyrocketed between 81 – 111 per cent over the last two years.

By comparison, sales of units at the lower end of the market (under $399,999) have plunged between 58 – 89 per cent over the same time period. As these unit types are typically bachelors, or one bedrooms outside the city core, this decline could be due to the growing challenge that is purchasing a home on a solo income. (According to StatsCan, the median single-income-earning household brings in $39,560 annually, qualifying for a maximum mortgage of $206,101.)

Related Read: The Best Canadian Markets for Buying a Home on One Income

As well, overall rising prices for Toronto condos mean fewer units are available at this price point, while new mortgage qualification rules may present hurdles for most buyers with smaller budgets.

However, the luxury condo segment continues to boom – sales for units priced above $1,000,000 are up 51 per cent over the same time frame, while those between $800,000 – $999,999 have increased between 110 – 211 per cent.

Check out how sales have changed over the last 24 months for various condo price points, in the infographic below:

Toronto Area Condo Sales by Price Range