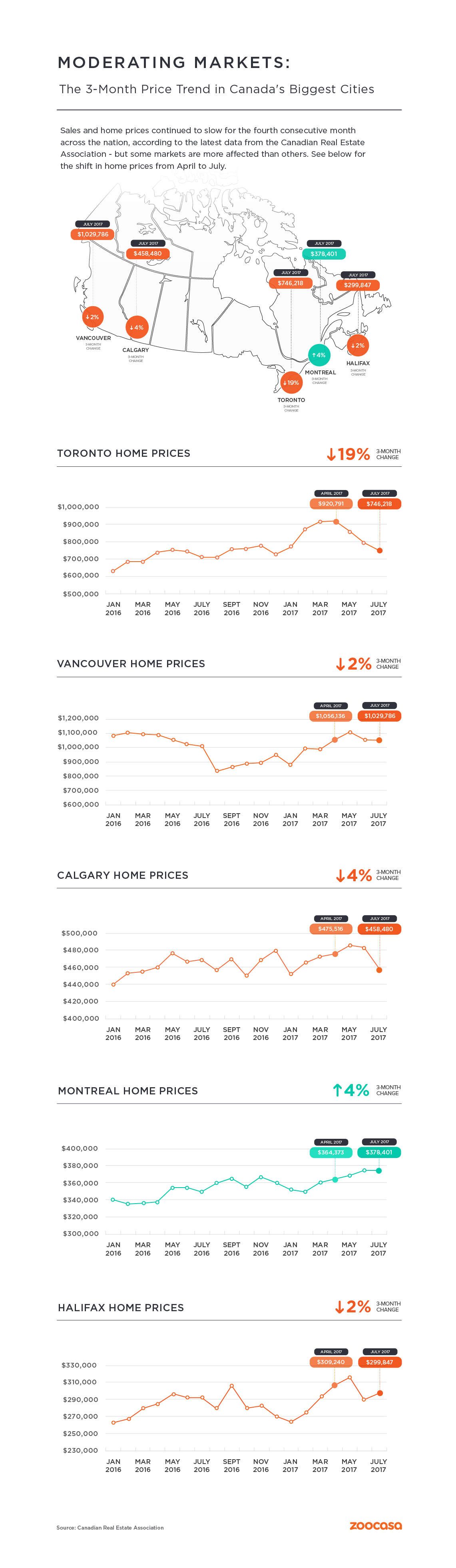

National home prices have fallen as a whole year over year for the first time since 2013, reveals the latest data from the Canadian Real Estate Association. The July report finds the new national average home price is $478,696 – a 0.3 per cent decrease – as sales softened for the fourth consecutive month, by 2.1 per cent, and 12 per cent from last July.

Much of the decline is being felt in the Greater Toronto Area, though sales fell in two thirds of all markets from June, including Calgary, Ottawa, and Halifax-Dartmouth.

However, the pace at which sales are slowing has substantially calmed since the panicked early summer market, down to only a third of what was seen in May (though still 15.3 per cent below the record set at the March peak).

Prices followed suit in the most affected markets:

Signs of a Calming Market?

A reduced slowdown could indicate the initial rush to list following recent housing market rule changes may be subsiding: sellers swamped the market with new homes for sale in response to Ontario’s Fair Housing Plan, just as buyers decided to take a “wait-and-see” approach.

That flood of new supply, combined with slower sales activity, has effectively tipped the Toronto real estate market into buyer’s territory. The number of months of available inventory – the amount of time it would take to completely sell all homes on the market – hit 5.2 nationally, the most since January 2016. In the GGH, it’s 2.6 months, which is more than triple the all-time low of 0.8 months recorded in February-March.

However, that new supply is starting to slow, moderating by 1.8 per cent across Canada, led by the GTA, Calgary, Edmonton, Montreal, and northern B.C., which has been impacted by wildfires throughout the summer season.

Related Read: GTA Home Sales Plunge 40% in July

Rising Interest Rates Play a Role

CREA President Andrew Peck says the July market may also have benefited from a small buying bump due to rising interest rates, as those with pre-approvals may have been prompted to make a move. “July’s interest rate hike may have motivated some homebuyers with pre-approved mortgages to make an offer,” he said. “Even so, sales activity continued to soften in the Greater Golden Horseshoe Region.”

Gregory Klump, CREA’s chief economist, adds that while this may indicate the market is improving, “Time will tell whether that’s indeed the case, once the transitionary boost by buyers with pre-approved mortgages fades.”

Will Buyers Return for Back-to-School?

The industry has been holding its breath to see if slowdown symptoms are indeed temporary; in addition to the Bank of Canada effect, they’re looking to September, which is usually a busy time for buyers. If buyers don’t show up for the back-to-school season, that could indicate there’s more at play than a market tantrum.

However, it appears new rules have had a positive effect; CREA reports that the majority of markets are now in balanced territory, at an average sales-to-new-listings ratio of 53.5 per cent. (A ratio between 40 – 60 per cent indicates a balance, while above and below are seller’s and buyer’s markets, respectively.) In contrast, the ratio was in the high 60s range in the first quarter of the year.

However, the GTA remains below the 40-per-cent mark.

“In the Greater Golden Horseshoe region, housing markets that recently favoured sellers have become more balanced, with some beginning to tilt towards buyer’s market territory.”

“A Perfectly Balanced Market”

Lauren Haw, Broker of Record at Zoocasa Realty, adds that buyers and sellers shouldn’t be deterred by Toronto’s new status, as it has led to overall healthier conditions.

“What is interesting is there’s less good inventory; buyers are starting to get excited again, but they’re being incredibly picky,” she says. “We are seeing very active buyers who are making offers on great properties, for example, a good house on a quiet street, luxury lofts, and condos with great layouts. Previously inactive buyers, who were priced out the market, are seizing the opportunity to get back in. It’s no longer the days of insane growth and buyers saying, ‘I’ll buy anything.’ As a result, we’re in a perfectly balanced market – if you have premium unit, you will get better buyers.”