Canada’s housing market is cooling, and for the 6 in 10 homeowners nearing the end of their term, that could spell trouble. Prices are down across major regions like Toronto, Vancouver, Fraser Valley, and Kitchener-Waterloo, with Toronto’s MLS Home Price Index falling 4.4% since December and Vancouver down 1.8% year-over-year, as reported by RBC. Even Calgary posted its first annual price drop in five years.

As inventory rises and buyers gain leverage, home values are expected to keep sliding. That’s good news for shoppers, but for current owners, it could mean less equity, tougher refinancing, and limited options when renewing or switching to a new lender. In some cases, homeowners with small down payments could even face negative equity. If your mortgage is due for renewal soon, understanding how your local market has shifted is more important than ever.

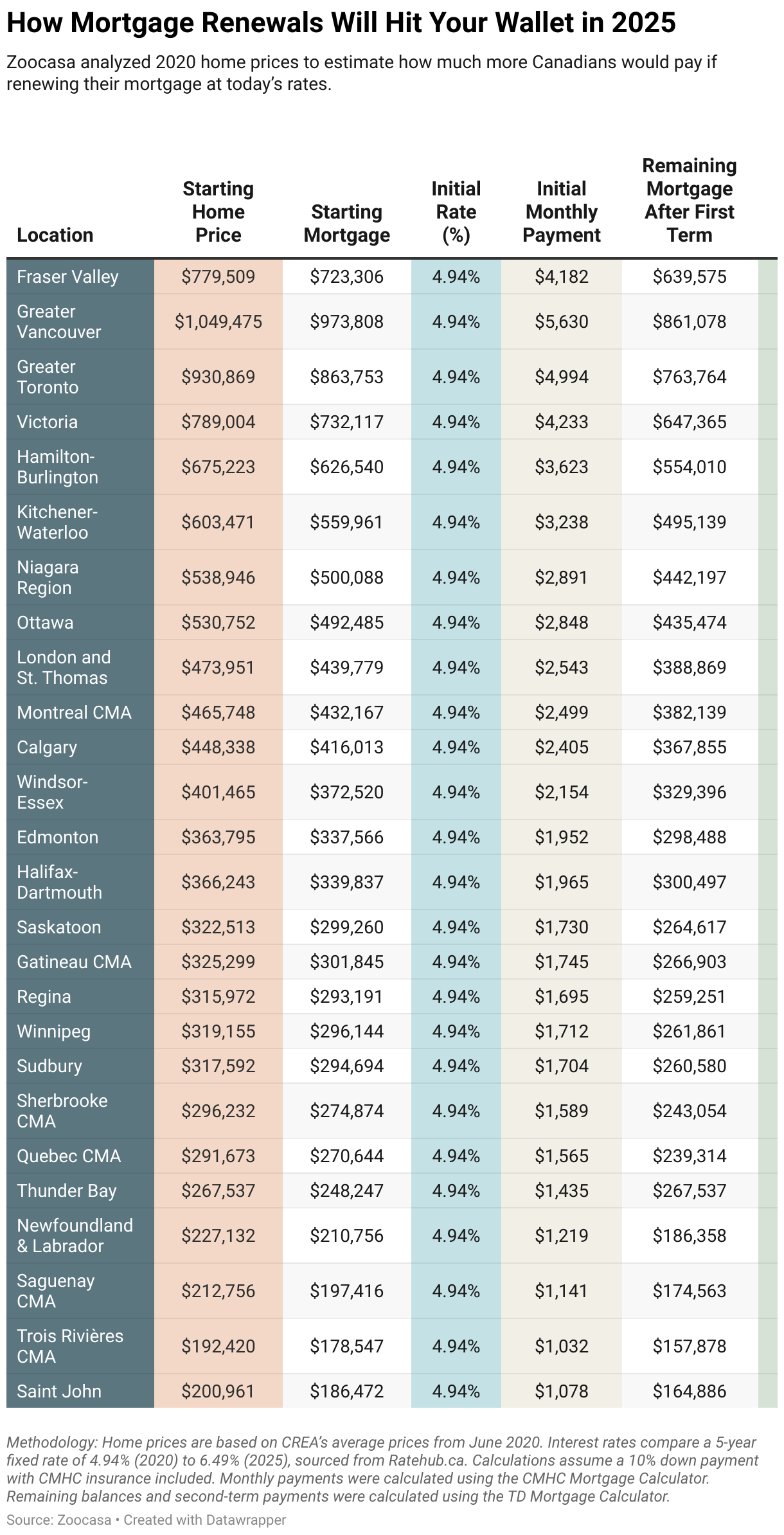

Zoocasa analyzed average home prices from 26 major markets in June 2020 to estimate how much more Canadians would pay when renewing their mortgages at today’s higher interest rates. The comparison uses a 5-year fixed rate of 4.94% from 2020 and a current rate of 6.49%, assuming a 10% down payment with CMHC insurance included. Monthly mortgage payments were calculated using the CMHC Mortgage Calculator, while remaining balances and projected second-term payments were determined with the TD Mortgage Calculator.

Of the 26 real estate markets analyzed, Fraser Valley saw the most significant jump in mortgage payments at renewal. Despite having a lower average home price than major cities like Toronto or Vancouver, the region is experiencing the most considerable annual increase in mortgage costs. That’s because Fraser Valley started with a lower monthly payment ($4,182), so when rates increased, even a $208 rise per month translated into a nearly 5% increase. Over a year, that’s an extra $2,496 out of pocket.

In Greater Vancouver, the average mortgage of $973,808 results in a monthly payment increase of $132, from $5,630 to $5,762, totaling $1,584 more per year. And while the increase isn’t as steep as Fraser Valley’s, the higher loan amount means Vancouverites are still carrying over $778,836 in mortgage debt after 10 years.

Meanwhile, in Greater Toronto, homeowners are paying an extra $117 per month (or $1,404 per year) with a remaining mortgage of just under $691,000 after 10 years.

Across the country, this pattern repeats. Throughout all regions analyzed in the report, seven will see their annual mortgage payments rise by a total of over $1,000, including Victoria, Hamilton-Burlington, and Kitchener-Waterloo. Another 14 regions, including Calgary, Ottawa, Montreal, and Halifax, are considering moderate increases ranging from $500 to $999 per year. The remaining five regions, including Thunder Bay, Quebec City, and Trois-Rivières, will experience minimal annual increases of under $500.

In Saguenay and Saint John, the yearly increase is as little as $324 or $300, which adds up to barely a dollar a day. But for regions like Fraser Valley, where affordability was already stretched, these changes represent a more dramatic shift in household budgets. This highlights a crucial point for homebuyers: it’s not just about the sticker price of the home. The long-term cost of borrowing can vary widely depending on where you live and how much room you have in your budget when the rates inevitably change.

With this report in mind, here are some additional essential factors that Canadian homeowners should consider when planning their finances.

Mortgage Truths Canadians Can’t Afford to Ignore

1. A wave of renewals is coming

If your mortgage is coming up for renewal soon, you’re not alone. According to the Bank of Canada’s 2025 Financial Stability Report, about 60% of all outstanding mortgages in Canada will come up for renewal in 2025 or 2026. Most of these are five-year fixed-rate mortgages that were secured during the pandemic, when interest rates were historically low. As a result, a large number of households will see their monthly payments increase, with some experiencing a significant rise.

However, the Bank notes that the average increase is now expected to be smaller than previously projected, thanks to interest rate declines over the past year. This shift presents homeowners with an opportunity to reassess their financial strategies. Whether it’s refinancing early, negotiating better terms, or switching lenders, proactive planning can make a big difference.

2. Delinquency rates are rising fast

Falling behind on debt payments is becoming more common in Canada. A Money.ca report titled Canada’s Rising Debt Crisis and Record Delinquency Rates shows that non-mortgage debt delinquencies rose 19.14% year-over-year in Q3 2024, hitting 1.43% nationally. This spike signals mounting financial pressure in households, particularly in urban hubs such as Toronto, Vancouver, and Montreal, where housing and living costs are the highest.

Young adults aged 18–25 are facing the steepest challenges, with delinquency rates soaring by 24.3% and average debt reaching $8,345. Pre-retirees (ages 56–65) are also struggling. Delinquency rates in that group rose 16.9%, with average debts surpassing $30,000. The combination of inflation, stagnant wages, and high interest rates is leaving more Canadians struggling to pay their bills. After all, one in four Canadians are going house poor regardless of income.

3. Mortgage renewals drive debt higher

Canadians across the country are feeling the pressure, not just from rising grocery and gas prices, but from increasingly costly mortgages. Higher interest rates are hitting homeowners hard, especially those facing renewals after the low-rate pandemic period.

A new Equifax Canada report highlights a growing financial strain, as total consumer debt has surged to a whopping $2.55 trillion, a 4% increase from the previous year. More than 1.4 million Canadians missed at least one credit payment, and mortgage delinquencies have reached their highest level since 2009.

The driving force? A wave of mortgage renewals is underway, with originations spiking 57.7% as pandemic-era borrowers reach the end of their terms. Nearly 30% of borrowers switched lenders, many seeking better rates—almost half of them moving between the Big Five banks.

Meanwhile, first-time buyers are back in the market, up 40% year-over-year, but higher loan amounts are testing the limits of affordability. According to Equifax, Ontario currently leads the country in mortgage and credit delinquencies, followed by Alberta and Quebec.

4. Rent is falling in major cities

April 2025 data from Rentals.ca shows a surprising drop in rental prices in Canada’s most expensive cities. One-bedroom asking rents in Toronto fell 5.8% year-over-year to $2,317, while Vancouver rents dipped 4.2% to $2,536. These shifts suggest a softer rental market, where high costs have pushed tenants to stay put longer or negotiate more favorable lease terms. For landlords, this means higher vacancy risk, more competition, and tighter margins, especially those facing rising mortgage payments or upcoming renewals. If rental income no longer covers carrying costs, some may be forced to sell their property.

5. Condo markets are cooling

Since early 2024, Toronto’s condo market has drawn attention as falling prices and growing vacancies dominate headlines. The Toronto Regional Real Estate Board’s Q1 2025 report now confirms what many suspected: the market is undergoing a significant shift. As explained in the report, condo apartment sales across the Greater Toronto Area dropped 21.7% year-over-year, totaling 3,794 units. Meanwhile, new listings surged 25.2%, hitting 14,544. The average selling price fell to $680,146, a 2.2% decline from the same period last year.

All in all, the rental-income squeeze is eroding investor cash flow. This plays a significant role in the market because, according to the Canadian Housing Statistics Program (CHSP), 41.9% of condominium apartments in Ontario are owned by investors. Ultimately, this might encourage more leveraged landlords to resort to forced sales and add supply to a market that is already softening.

Thinking of buying or selling? A local Zoocasa agent can help you find the right home in your budget.