The main purpose of home insurance is to protect homeowners and tenants from unexpected risks. These risks can damage their property, their contents, or can result in other additional costs (like being sued, paying out of pocket accommodation expenses, etc.). There are many things that can negatively impact your dwelling, and risks come in all shapes and forms. From storms damaging your building to water damage inside your home, you need to be properly protected.

Our friends at InsurEye analyzed thousands of home insurance reviews related to home insurance claims submitted by Canadians in order to bring more transparency to this matter.

There are many ways to classify home insurance claims, e.g. some are human-driven (which encompasses theft and break-ins) versus nature-driven (which includes storms, particular types of flooding, etc.). This study structures home insurance claims by dividing them into six groups that are separated by the type of damaged sustained:

- The first group of claims relates to water damage, which often impacts floors on lower levels, including basements.

- The second, fire and smoke, can often lead to a total loss.

- The third, hail damage, mainly impacts the roof.

- The fourth, break-ins, often only impacts the content within the home.

- The fifth, damages through wind, mainly impacts the roof.

- Finally, the sixth claim encompasses other types of damage, including damages due to a pet, a tenant, etc.

In many cases, even these six categories can be broken down further.

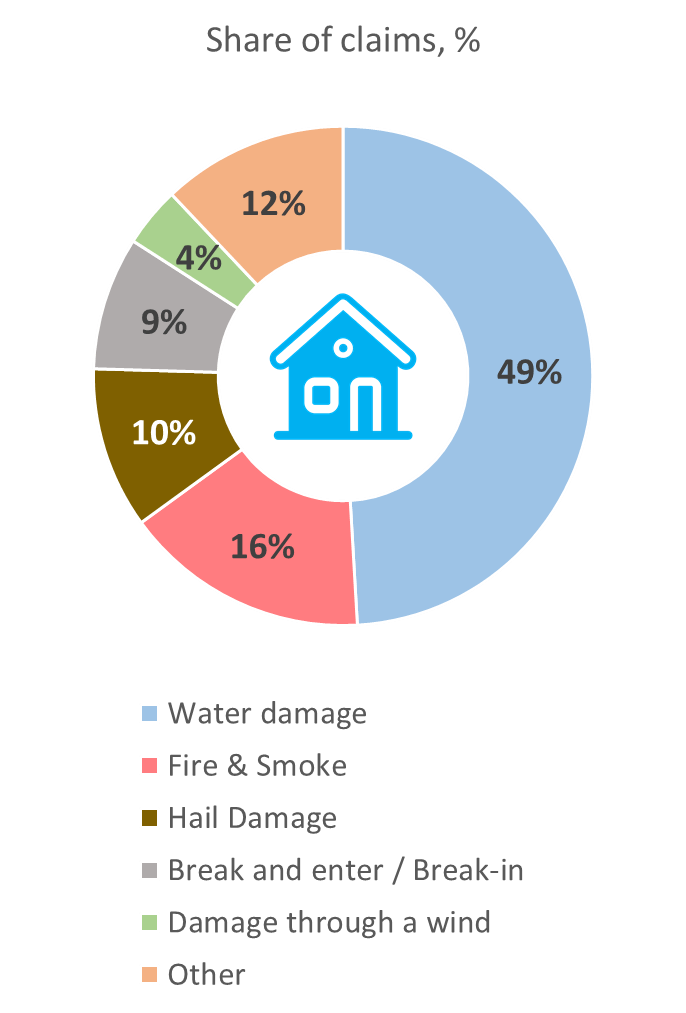

Almost Every Second Home Insurance Claim Relates to Water Damage

Although the world of home insurance claims is very broad, water damage is responsible for nearly half (around 49%) of all home insurance claims. That is why it is important to have strong protection in place for these types of claims in particular.

The second most frequent claim type are those related to fire and smoke damage. According to the study, these account for nearly 16% of all claims. This type of claim can be driven by multiple factors, including smoking, bad electrical circuits, outdated electrical wiring, and malfunctioning electronic devices.

The third most frequent claim type is that related to hail damage. This is a common risk in both car insurance and home insurance. When specifically talking about home insurance, hail damage mostly impacts the roof and siding of a home.

Approximately 9 per cent of all the claims studied relate to human-driven claims, resulting from property break-in and theft. All of the other claims categories are rather small and describe a long list of possible risks, including (but not limited to) damage from wind at ~4 per cent, damage from a fallen tree at ~3 per cent, lost jewelry at ~2 per cent, and environmental pollution (e.g. oil leakage from heating systems) at ~1 per cent.

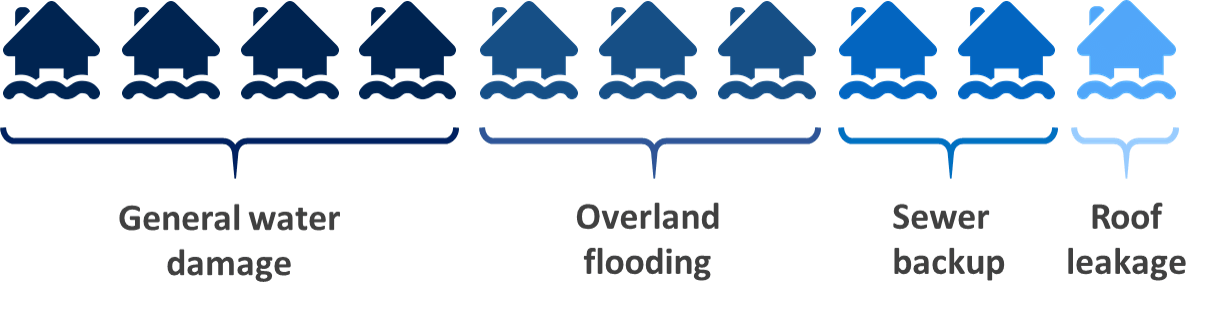

Water Damage Has Many Faces

There are many ways in which water can damage your home, and there are many sources from which this damage can result. It is important to know all of these sources and to protect yourself against any potential damages. In simple terms, for 10 water damage claims the frequency of each claim type would break down as follows:

- 4 of 10 claims will relate to general water damage. These damages may result from bad plumbing, burst pipes, or any other water-related accidents that originate inside your house.

- 3 out of 10 claims will result from overland flooding (e.g. due to strong rains, melting snow, etc.), where water enters your dwelling from the outside. Most of the damage in these cases will occur in your basement. Some regions are more susceptible to this danger. Home insurance in Ontario is of the utmost importance, as well as in Alberta, including home insurance in Edmonton and Calgary; all of these areas have a history of extensive overland flooding.

- 2 out of 10 claims will relate to sewer backup, where the municipal sewage system cannot cope with a large volume of water, pushing everything back into your home.

- 1 out of 10 claims will relate to roof leakage, which could either be due to storm damages or to a lack of maintenance.

There are a few minor claims categories, including water seepage through building fundament (e.g. due to groundwater), but it is rather negligible when considering the bigger picture. Even if you are only able to protect yourself against the first three water damage categories, you have already covered about nine of 10 of the most common potential water damage claims.

How Can You Protect Yourself Against Water Damage?

Given the fact that water damage is responsible for the overwhelming majority of home insurance claims, it is important to know how to protect yourself. The following are suggested approaches to some of the most common claims that are related to water damage:

General water damages: Most existing policies will cover this risk already, but you need to make sure that you have enough coverage and that you are comfortable with the deductibles you choose. The deductible is the amount that you pay before your insurance coverage kicks in. If you have water damage that results in $10,000 in damages to your home and your deductible is $2,000, that means you will have to pay $2,000 and your insurer will pay the remaining $8,000.

Damages through overland flooding: Preparation in this case actually starts before you purchase your home. Make sure that you understand where your future house will be located, and find out if that area is considered to be a dangerous flood zone. Municipal authorities will provide these maps. The second step is to get overland flooding coverage. This is a separate endorsement (also called a rider) that is either sold separately from other endorsements, or that can occasionally be bundled with sewer backup coverage. Insurers may call this either Overland Flooding Endorsement or Overland Water Endorsement.

Sewer backup: When you are buying your house, you should find out if there is a sewer backup valve that has been installed. If not, it is a good idea to install one. The device itself costs somewhere between $50 and $150 plus installation fees, but it will provide solid protection against unexpected sewer backups. To be entirely sure that you are covered even if a sewer backup occurs, you will need a separate endorsement for Sewer Backup. As previously stated, this is occasionally bundled with overland flooding coverage. This coverage may only add up to a few more dollars on your home insurance bill, and it is definitely worth the additional cost.

Our last tip, which relates to all claim types, is to walk through your house at least every six months. While doing so, take photos or videos of all the key items within your home, including any upgrades that have been made. This will help you in the event that you have a claim to discuss the size of the claim with your insurer.

We hope that you found these tips helpful and that they allow you to feel better prepared when it comes to unexpected insurance claims. These insights have been offered by InsurEye, the largest Canadian insurance review platform, offering access to home, auto, life, and disability insurance quotes.