By RateHub.ca

Are you thinking of refinancing your existing mortgage to consolidate other debts or take advantage of a lower interest rate? Before rushing to the bank, you should consider two things: the type of mortgage you have and the penalty fee you could potentially have to pay to do so. If you have an open mortgage, you can pay off your mortgage at any time without penalty. However, if you have a closed mortgage, paying off your mortgage beyond your prepayment privileges can result in a hefty penalty.

Let’s take a look at the two different prepayment penalties – three months’ interest and the interest rate differential (IRD) – and see how they are calculated and when you would have to pay them.

Three Months’ Interest

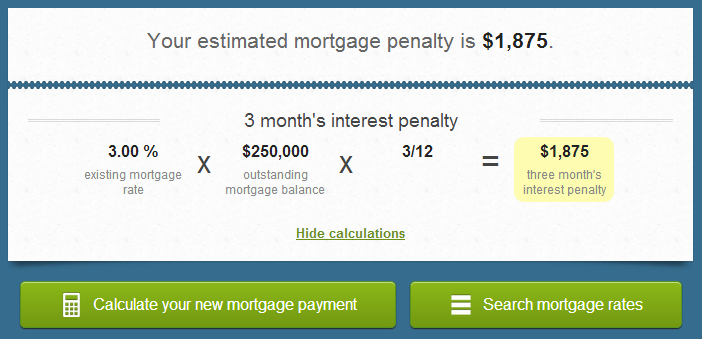

Three months’ interest is exactly that – making it much more straightforward than the IRD calculation – and it only varies slightly from lender-to-lender. Three months’ interest is calculated as three months of simple interest at your current mortgage rate on your current mortgage balance.

For example, let’s say you still owe $250,000 on your mortgage and your current interest rate is 3.75 per cent. If you were to refinance, you would calculate your penalty by multiplying 3.75 per cent by $250,000, dividing the total by 12 months and multiplying that by 3 months.

Some lenders, on the other hand, use their Prime rate instead of your current mortgage rate. CIBC is one bank that uses its own Prime rate, so the example numbers from above end up looking like this:

If you break a variable rate mortgage, the penalty is always three months’ mortgage. But if you break a fixed rate mortgage, you will pay the greater of three months’ interest or the IRD.

Interest Rate Differential (IRD)

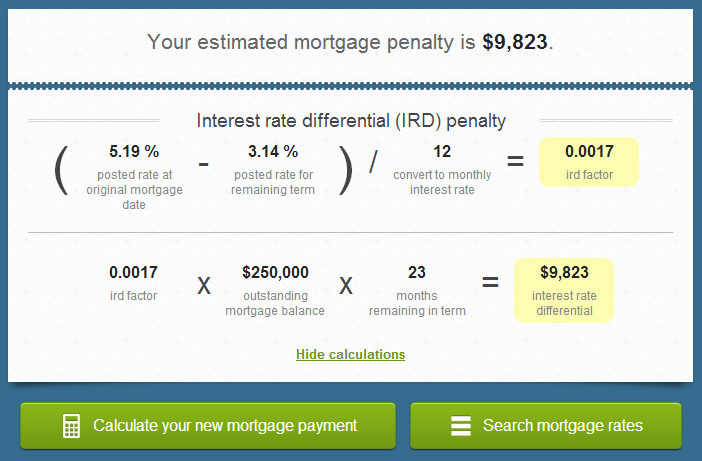

The interest rate differential (IRD) is a little bit trickier to calculate, because lenders use different rates to determine how much your penalty will be. The basic idea is that your lender wants to find the amount of interest they will lose by letting you pay off your mortgage early. To determine the IRD, your lender will first look at the difference between two rates – usually the posted rate from the day you got your mortgage and the posted rate that you would get on a similar term today.

Because these numbers aren’t always easy to come up with on your own, RateHub.ca has built a penalty calculator that finds the numbers for you and estimates what your penalty will be. Let’s use the same numbers as before and assume you’re breaking a fixed rate mortgage with CIBC. If the balance of your mortgage was $250,000 and you still had 23 months remaining in your term, your IRD for CIBC would look like this:

In this example, you’d pay the IRD penalty of $9,823 because it is greater than three months’ interest. Again, remember the IRD is only applicable for homeowners with fixed rate mortgages.

No matter how much your prepayment penalty is, it’s important to calculate whether or not refinancing is something that will save you money in the long run. To see how much a refinance could save you, run your own numbers through a refinance calculator.

—

About the contributor: