Canadian real estate ended the year on a softer note as December marked the fourth consecutive monthly decline in sales, and annual activity fell 12% below the 10-year average.

The number of homes trading hands fell 2.5% month over month, effectively wiping out any gains enjoyed during the summer market, and 19% from the same time period in 2017, reports the Canadian Real Estate Association. This slower pace was felt in three quarters of all markets, though “overwhelmingly” so in British Columbia’s Lower Mainland, Okanagan Valley, Calgary, Edmonton, Greater Toronto Area and Hamilton-Burlington region.

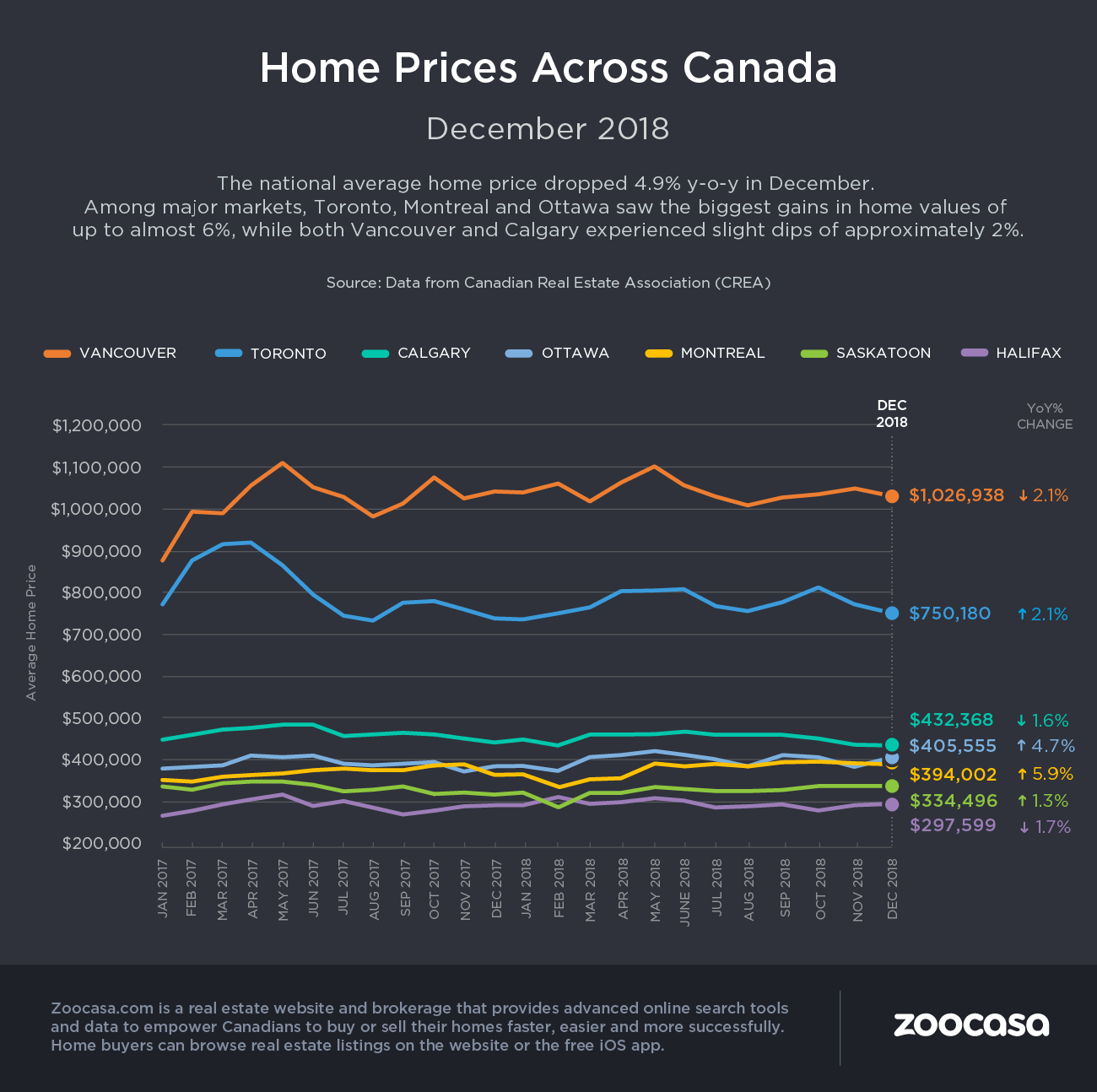

The national average home price receded by 4.9% year over year to $472,000; stripping out Toronto and Vancouver home values, however, would reduce the average to $375,000.

Stress Test Means Fewer Qualified Buyers

CREA says weaker annual activity is due to a combination of fewer sales as a result of tougher mortgage requirements introduced last year, as well as the fact that sales during the previous December were unusually strong.

“What a difference a year makes. Sales trends were pushed higher in December 2017 by home buyers rushing to purchase before the new federal mortgage stress test took effect at the beginning of 2018,” said CREA President Barb Sukkau. “Since then, the stress test has weighed on sales to varying degrees in all Canadian housing markets and it will continue to do so this year.”

CREA also points to the economic and interest rate update released by the Bank of Canada this month, which forecasted a weaker housing market this year as the pain from overall higher interest rates are compounded with the fallout from the stress test.

“The Bank of Canada recently said that it expects housing activity will stay ‘soft’ as households ‘adjust to the mortgage stress test and increase in mortgage rates’ even as jobs and incomes continue growing,” says CREA Chief Economist Gregory Klump. “Indeed, the Bank’s economic forecast shows it expects housing will undermine economic growth this year as the mortgage stress test has pushed home ownership affordability out of reach for some home borrowers.”

A Slightly Easier Buyer Environment

Because new listings stayed relatively the same on a monthly basis, up just 0.2% from November, they did little to offset slower sales activity, resulting in eased buyer conditions. The national sales-to-new-listings ratio, which measures the number of homes sold out of newly available listings during the course of the month, was 53.3% in December; still within balanced territory, but below the 54.8% recorded the month before, and slightly below the long-term average of 53.5%. According to this metric, two thirds of all Canadian markets can be considered balanced.

The amount of inventory clocked in at 5.6 months in December – slightly higher than the long-term average of 5.3 months. However, this was steeply uneven across the nation, with some markets – especially in the Prairies and Newfoundland and Labrador – with inventory much higher than average, while remaining below the average in Ontario and PEI.

Price Growth by Home Type

As has been the long-term trend, apartments continue to post the strongest year-over-year price gains, up 4.9%. That’s followed by townhouses and rowhouses at 3.1%. House price growth was more subdued; two-storey single-family homes saw values rise just 0.4%, while one-storey homes are down 0.3%.

Price Growth By Province

British Columbia: It has been a period of pain for Canada’s notoriously priciest market, with price growth down 2.7% for Greater Vancouver real estate– that’s a sharp turnaround from the robust increases experienced over much of the past two years. However, prices rose 2.5% in the Fraser Valley, 6.4% in Victoria, and 11% elsewhere on Vancouver Island.

Ontario: Price growth continued to be steady throughout the Greater Golden Horseshoe markets, rising 6.8% in both Guelph and the Niagara region, 6.4% in Hamilton-Burlington, 3.3% in Oakville-Milton, and 3% for MLS listings in Toronto and the GTA Barrie and District was the only Ontario market to post a decline, at -01.1%.

Eastern Ontario continues to see strong growth with prices up 6.9% in Ottawa, fueled by an 8.3% uptick in townhouse prices.

Prairies: Home values continue to lag in Canada’s bread basket as supply remains “historically elevated” relative to sales. Calgary real estate listings are down 3.2%, followed up a 2% drop in Edmonton, -5.2% in Regina and -1.2% in Saskatoon. “The home pricing environment is likely to remain weak in these housing markets until elevated supply is reduced and becomes more balanced in relation to demand,” writes CREA.

Eastern Canada: The Greater Montreal housing market has been a bright spot for national sales activity, and continues to see robust growth, up 6% in December. Greater Moncton is also seeing booming home values, rising 12% last month.