Canadian home sales slowed yet again in November as the national stress test continues to take steam out of the market, resulting in a forecasted five-year low in activity for 2018.

The Canadian Real Estate Association reports the number of homes exchanging hands remains below the 10-year average, down 2.3% on a monthly basis and -12.6% from 2017, compounding the 1.7% decline recorded in October. Sales were down annually in three quarters of all markets, though most pronounced in the Greater Toronto Area, BC’s Lower Mainland, Calgary, and the Hamilton-Burlington region.

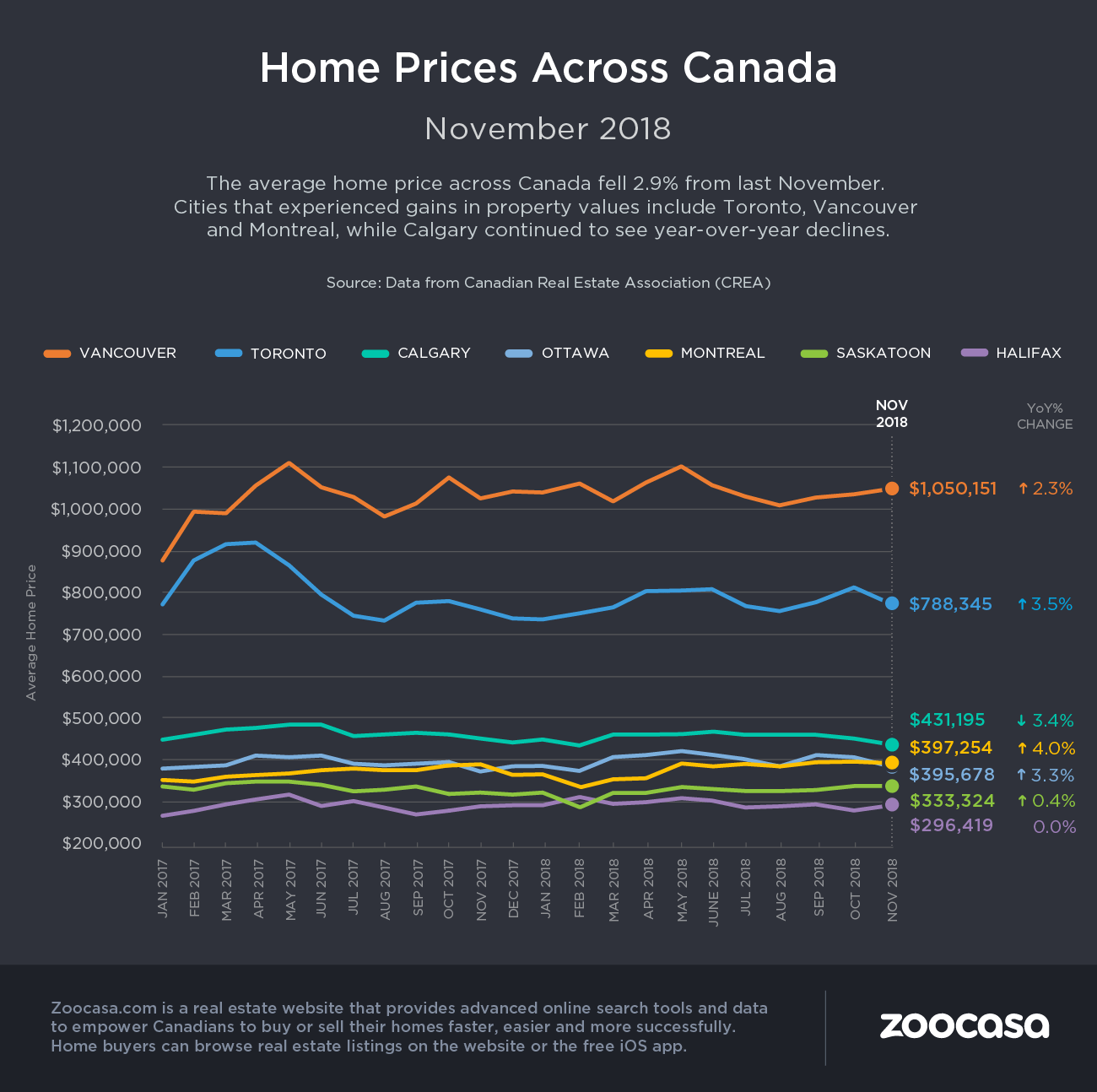

The average home price has also contracted 2.9% year over year, hitting an average of $488,000, though would be only $378,000 if Toronto and Vancouver were removed from the equation.

2018 to Have Fewer Sales than Expected

Slower activity has prompted the national association to again revise its final forecast for 2018, calling for 458,200 homes sold over the total year – an 11.2% decline. The downward revision is due to a lack of forecasted recovery in BC, and the belief that Ontario’s rebound has ended, while Alberta sales continue to soften. It calls for sales to remain roughly flat throughout 2019 at a total of 456,200 units, and for prices to rebound only 1.7%.

National Stress Test to Blame

Gregory Klump, CREA’s chief economist, puts the blame for slower activity squarely on the national mortgage stress test, which requires borrowers of new mortgages to prove they can qualify at a rate roughly 2% higher than the one they’ll actually receive from their lender. That’s slashed purchasing power, despite strong employment and migration fundamentals that would otherwise support the market, he says.

“The decline in homeownership affordability caused by this year’s new mortgage stress test remains very much in evidence,” he states in CREA’s release. “Despite supportive economic and demographic fundamentals, national home sales have begun trending lower. While national home sales were anticipated to recover in the wake of a large drop in activity earlier this year due to the introduction of the stress test, the rebound appears to have run its course.”

Fewer New Listing Put Pressure on Buyers

However, while sales are down, so too are the number of newly-listed homes, which has put tighter pressure on buying conditions; shorter supply in 70% of all markets has pushed the national sales-to-new-listings ratio up slightly to 54.8%, from 54.2% in October – still balanced, but leaning more-so toward a sellers’ market. This ratio, which is calculated by dividing the number of sales by new listings, is used to determine how many newly listed homes are sold over the course of the month. A ratio between 40 – 60% indicates a balanced market, while below and above that threshold reveal buyers’ and sellers’ markets respectively, according to CREA.

According to the November report, 60% of all markets remain in balanced territory, with the total months of inventory – the amount of time it would take to sell all available homes – coming in at 5.4%. While that’s in line with the long-term average of 5.3%, inventory levels are varying widely between markets. CREA points out that while the supply of homes remains below average in Ontario and most of eastern Canada, it is “well above” average in the prairie provinces and Newfoundland and Labrador.

Price Trends by Region

Based on the variances in available inventory and sales activity, CREA points out that price trends are also differing widely across the country.

BC: On the west coast, prices are still up, though the pace of gains continue to diminish. Home values are up 4.7% in the Fraser Valley, 7.2% in Victoria, and 12.6% on Vancouver Island. However, price gains are down for the first time in five years on the Greater Vancouver MLS, posting a decline of 1.4% year over year.

Ontario: The Greater Golden Horseshoe continues to see steady price gains, up 9.3% in Guelph, 7.2% in Niagara Region, 6.3% in Hamilton-Burlington, 3.4% in Oakville Milton, and 2.7% for MLS listings in Toronto and the GTA. Barrie and District was the only region to post a decrease, at 2.1%.

The Ottawa market continues to boom, with prices up 6.6%, led by a 7.3% uptick in two-storey home prices.

Prairies: Home prices continue to soften in Canada’s oil patch and bread basket, down 2.9% for Calgary homes for sale,1.9% in Edmonton, 4% in Regina, and 0.3% in Saskatoon.

Eastern Canada: Price growth has been rosy in la belle province, up 6.2% in Montreal, fueled by a 9.4% increase in townhome and rowhouse values. Greater Moncton also experienced a 4.2% increase.

Price Gains by Home Type

Apartments continue to lead the market in terms of price gains, with values up an average of 6%, followed by townhouses at 4%. Single-detached home prices remained flat, up 0.4% and 0.1% among one- and two-storey houses.