This November was the second-strongest on record for national home sales with transactions falling just a few hundred short of the 2020 record, according to the Canadian Real Estate Association (CREA).

The latest numbers released by the national housing body reveal a total of 54,222 residential sales occurred last month, up 0.6% from October, and just -0.7% below last year’s activity. Year-to-date, a total of 630,634 homes have traded hands, well bypassing the 2020 record that was broken last month.

The market also benefited short term from some sorely needed new supply as 70,406 homes were brought online, a 3.3% uptick from the previous month, though still -4.6% below 2020’s November levels.

However, those new listings fell short of making a dent in today’s fierce, seller-friendly market; the average home price continued its record-breaking trajectory, rising 19.6% to $720,850 (stripping Vancouver and Toronto out of the equation would lower that average to $562,820), while the MLS Home Price Index rose 25.3% year over year.

Related Read: GTA Home Prices and Sales Smash 2020 Record in November

While the market showed some slight easing compared to October’s record breaking frenzy, Cliff Stevenson, CREA’s Chair, says an unprecedented supply and demand imbalance continues to underpin current market trends.

“November provided another month of evidence that the housing supply/demand issues facing the country have not gone away,” he stated in the association’s release. “Even at what is traditionally the slow time of year for housing, conditions and price trends are at the same record levels we saw this spring. Things may calm down a bit through the balance of December and January, but next year’s spring market will no doubt be an interesting one.”

November’s uptick follows an extremely volatile year for sales with CREA noting a roller coaster of activity, from a record-breaking 807,250 sales in March, plunge to 585,250 in August, and rebound to 650,000 in the late fall.

New Listings Ease Short-Term Pressure, But Make No Dent in Supply Scarcity

The scant 3.3% increase in new supply improved conditions very slightly for buyers, with the national sales-to-new-listings ratio (SNLR) dipping to 77%, from 79% in October. This ratio, which is calculated by dividing the number of sales by the number of new listings over the course of the month, determines the level of competition in the housing market. A range between 40 – 60% indicates a balanced market, with above and below that threshold indicating sellers’ and buyers’ markets, respectively.

According to CREA, two-thirds of all local markets can be considered to be in sellers’ territory, with the remaining experiencing balanced conditions. Currently, there are no markets in Canada that can be considered in favour of buyers.

Overall inventory – the number of months it would take to completely sell off all homes for sale in current conditions should no new listings be introduced – currently sits at 1.8 months, tied with March levels as the lowest in history, and well below the long-term average of 5.5 months. CREA notes this metric has fallen below the two-month mark four times this year, first in February – March, and again in October – November, which has contributed significantly to this year’s record price growth.

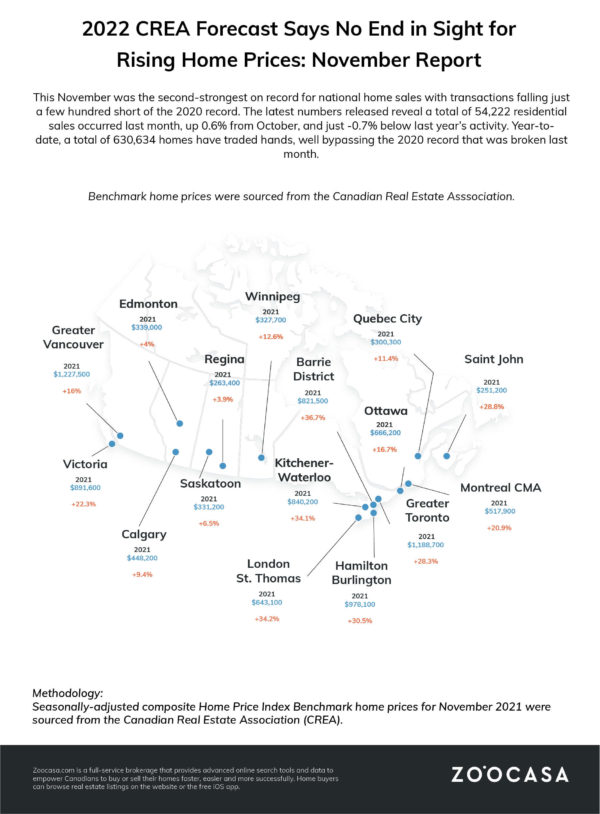

Check out the infographic below to see how prices trends in Canada’s major urban centres in November:

Ontario Market Breakdown:

As has been the year-long trend, the bulk of price growth has occurred in the nation’s east and west ends, up 25% in British Columbia, 20% in Montreal, and between 10 – 30% in the Maritimes, with mid – high single digit growth in the prairies. In Ontario, prices surged 30%, led by a rebound in the Greater Toronto Area.

The GTA: Ontario’s largest urban centre posted a 2.9% increase in sales year over year with 9,508 transactions, a welcome increase of 7.6%. That has helped lower the region’s SNLR to 73.2% from the 80.8% it sat at in October, taking some steam out of the area’s fraught sellers’ markets. However, the benchmark home price still rose 3.9% month over month and 28.3% year over year to $1,188,700.

Ottawa: The nation’s capital remains a highly competitive sellers’ market, as new listings dipped 2.8% from October, and are down -13.1% year over year. Coupled with a 1% increase in sales from October (with 1,693 transactions, -9.1% year over year), that’s pushed the city’s SNLR up by 3% to 79.9%, and the benchmark price by 16.7% year over year to $666,200.

Kitchener-Waterloo: While still mired in a steep sellers’ market with an SNLR of 82.8%, the KW market enjoyed a 12% monthly increase in new listings in November, also marking a 6.4% uptick year over year. That in turn fuelled a 5.7% increase in sales with 664 transactions, and a whopping 34.1% year over year increase in the benchmark price, to $840,200

Hamilton-Burlington: Conditions cooled slightly in the Hammer thanks to a 13.5% increase in new listings in November, which pulled the region’s SNLR down to 75.9%. Sales also dipped on a monthly and year-over-year basis by -1.8% and -3.3%, respectively, though the benchmark price rose 2.5% MoM and 30.5% YoY to just under the million-mark at $978,100.

London-St Thomas: A 12.3% surge in new listings last month helped boost sales over the short term, with 969 homes trading hands (+2.2% MoM and -4.2% YoY). It also let some of the steam out of the region’s SNLR, which eased to 79.2%, while the benchmark price rose 3.2% MoM and 34.2% YoY to $643,100.

CREA Updates Forecast: Prices to Continue to Rise into 2022

CREA also updated their take on the coming year, predicting 2022 will usher in more of the same; there’s no price relief for buyers on the horizon as supply will remain historically scarce, which in turn will continue to constrain sales.

Buyers’ affordability will also be further challenged by a rising interest rate environment as the Bank of Canada scales back its pandemic stimulus and starts raising its trend-setting Overnight Lending Rate as early as April.

Related Read: Bank of Canada Leaves November Rate Untouched

As a result, CREA anticipates a total of 610,700 transactions will occur next year, an -8.6% decrease from the forecasted final 2021 number of 668,000 (marking a 21% increase from 2020). The average home price will settle this year at $687,500, an increase of 21.2%, before rising another 7.6% next to $739,500.

Another major factor to impact the 2022 market is the resurgence of immigration, which could surge to record levels post-pandemic, “turbocharging” buyer competition amid the ongoing supply crunch. Other “wildcards” include a potential re-evaulation of the existing mortgage stress test, which pads in a buffer between the contract rate and the qualifying rate for borrowers depending on their equity, and the potential for the federal Liberal government to exact their housing election promises into policy including a ban on blind bidding, a two-year pause on foreign investment, and a focus on new supply.