Slower home construction, rising interest rates, higher home prices, and stagnant wage growth have created challenging conditions for the average American homeowner. As a result, fewer Americans can attain affordable housing.

As defined by the U.S. Department of Housing and Urban Development (HUD), housing is considered affordable if an occupant spends no more than 30% of their income on housing costs. But a large percentage of Americans are overspending.

A recent Zoocasa survey of over 1,000 American renters and homeowners found that over one in three respondents (39.7%) are spending over 30% of their household income on housing costs, including rent, mortgage, and maintenance.

More Americans Are Going “House Poor”

Nearly a quarter of Americans (23.8%) spend between 30 and 40% of their household income on housing costs, and an additional 15.9% of Americans spend over 40% of their income on housing. That leaves just 60.3% of Americans who are spending within the recommended guidelines on housing.

If a household spends more than 30% of its income on housing, then it is cost-burdened or “house poor”. In this case, a household will have to reduce its spending in other areas, such as food or leisure expenses, to compensate for elevated housing costs.

But the repercussions aren’t just limited to daily life. With less money to put toward savings and retirement, cost-burdened households are particularly vulnerable if an emergency occurs.

“When housing costs take up too much of a person’s income, it’s not just about budgets. It’s about trade-offs they didn’t plan for, like savings, bill payments, or peace of mind,” explains Carrie Lysenko, Zoocasa CEO. “Over time, those trade-offs add up and reshape how people think about stability, opportunity, and what they can realistically plan for next in terms of owning a home.”

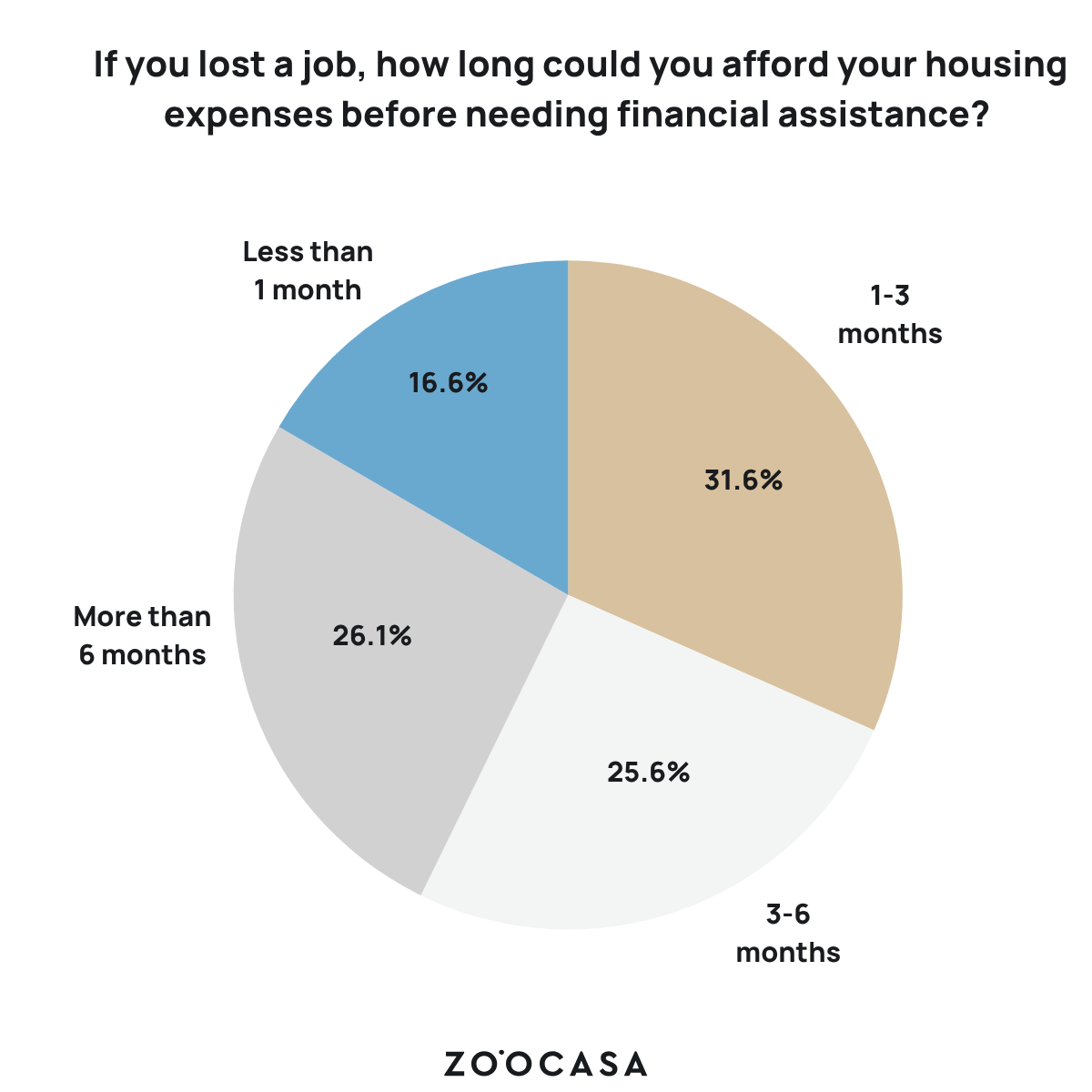

For some, one missed paycheck could mean falling behind on mortgage payments. According to our survey, 31.6% of respondents would only be able to pay their housing expenses for 1-3 months if they lost a job, and an alarming 16.6% of respondents could pay their housing costs for less than 1 month. Only 26.1% of respondents could afford their housing expenses for more than 6 months, leaving a large portion of Americans vulnerable to unexpected changes.

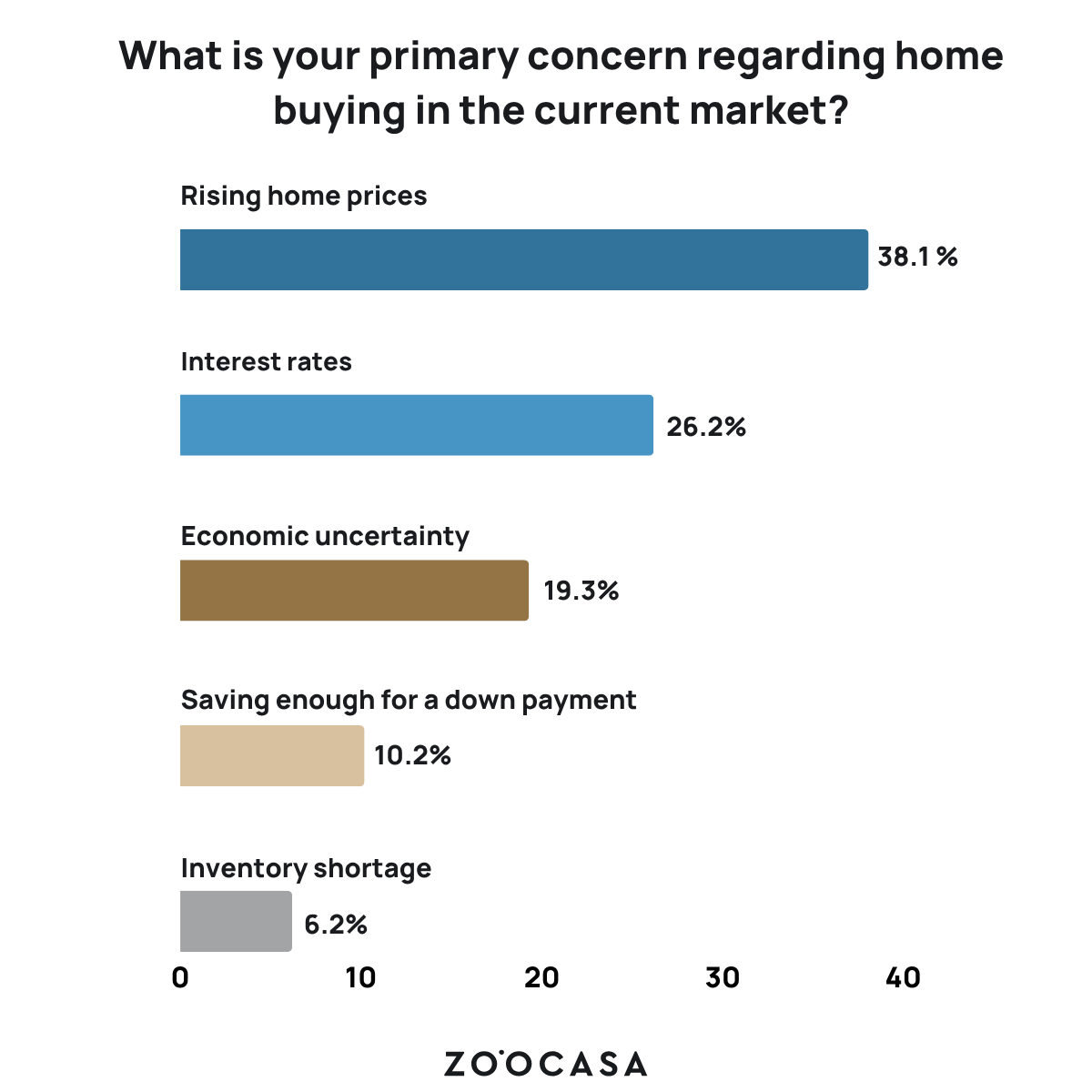

Rising Home Prices Are the Number One Housing Concern

The biggest concern for home buyers in the current market is rising home prices (38.1%), followed by interest rates (26.2%), economic uncertainty (19.3%), and saving enough for a down payment (10.2%).

The national median single-family home price currently stands at $429,400, according to the National Association of Realtors. This marks a 1.7% increase from last year and an 87% bump from 2015.

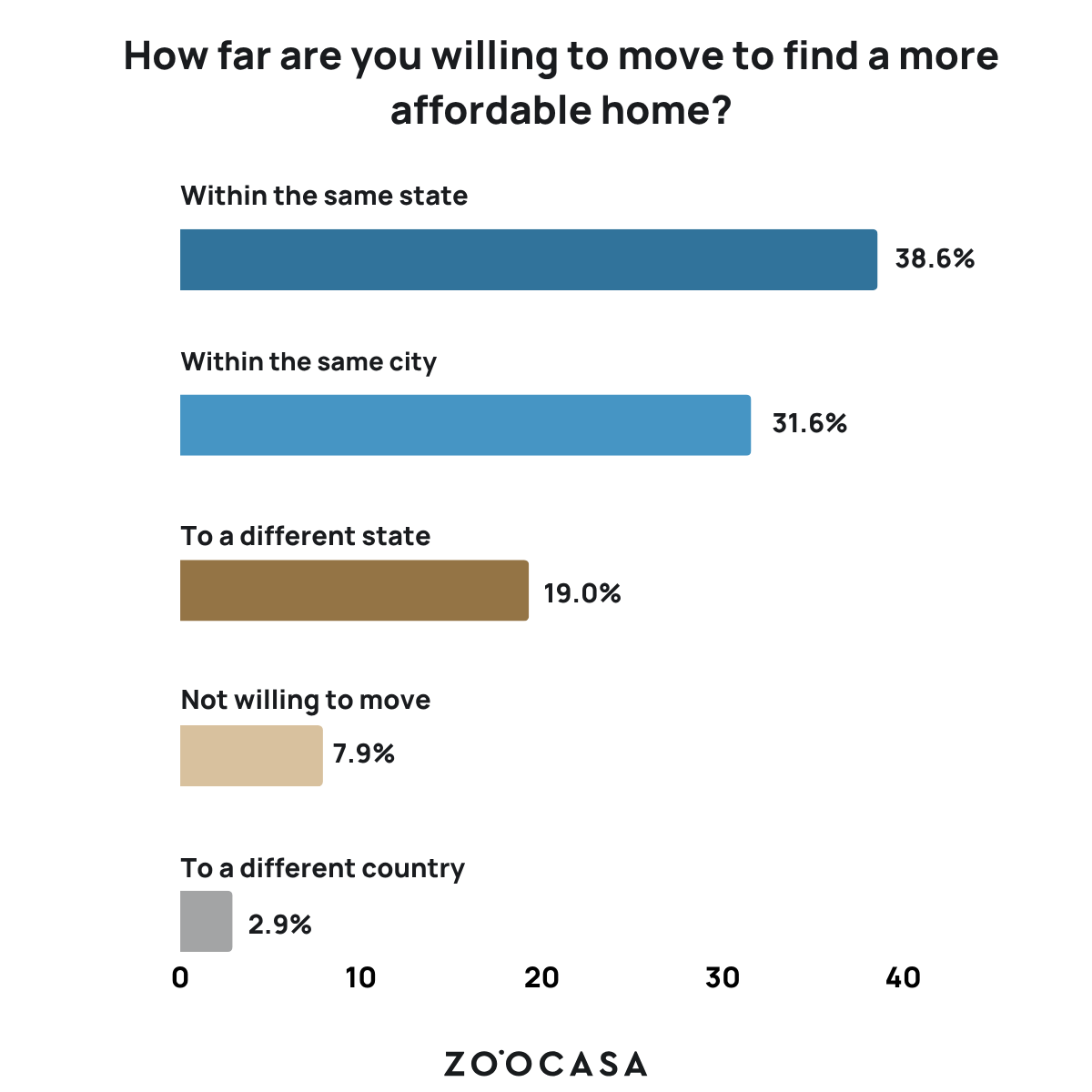

But despite affordability being top of mind for homebuyers, most are not willing to move very far to find an affordable home.

Just 19% of respondents said they are willing to move to a different state to find an affordable home, while an even smaller percentage (2.9%) said they’d be willing to move to a different country. Nearly 40% of respondents are only willing to move within the same state, and a similar portion of respondents (31.6%) are only willing to move within the same city.

A significant majority of respondents (63.3%) indicated a willingness to commute longer distances in exchange for lower housing costs. This suggests that Americans are open to making compromises on location, provided it does not take them too far from their current community.

“Data shows that people are willing to bend on their commute, not their community,” adds Lysenko. “Buyers want affordability, but not at the cost of leaving behind their support systems, schools, or sense of belonging. That’s a powerful reminder that home is more than just a price tag.”

Grocery Costs Straining Household Finances

The more a household spends on rent or mortgage payments, the less it has to spend on other necessities, like food and transportation. And as the saying goes, the rent eats first.

But with grocery costs rising concurrently with housing costs, households have noticeably less to spend on food. The average price of eggs has increased by 170%, bread by 23%, chicken by 29%, and oranges by 38% since 2020.

As a result, 41.3% of survey respondents said groceries were the increasing cost they were most concerned about, followed by housing (32.1%), health (12.1%), transportation/gas (6%), insurance (5.9%), and childcare (2.5%).

The Ripple Effect Home Costs Have on Life Decisions

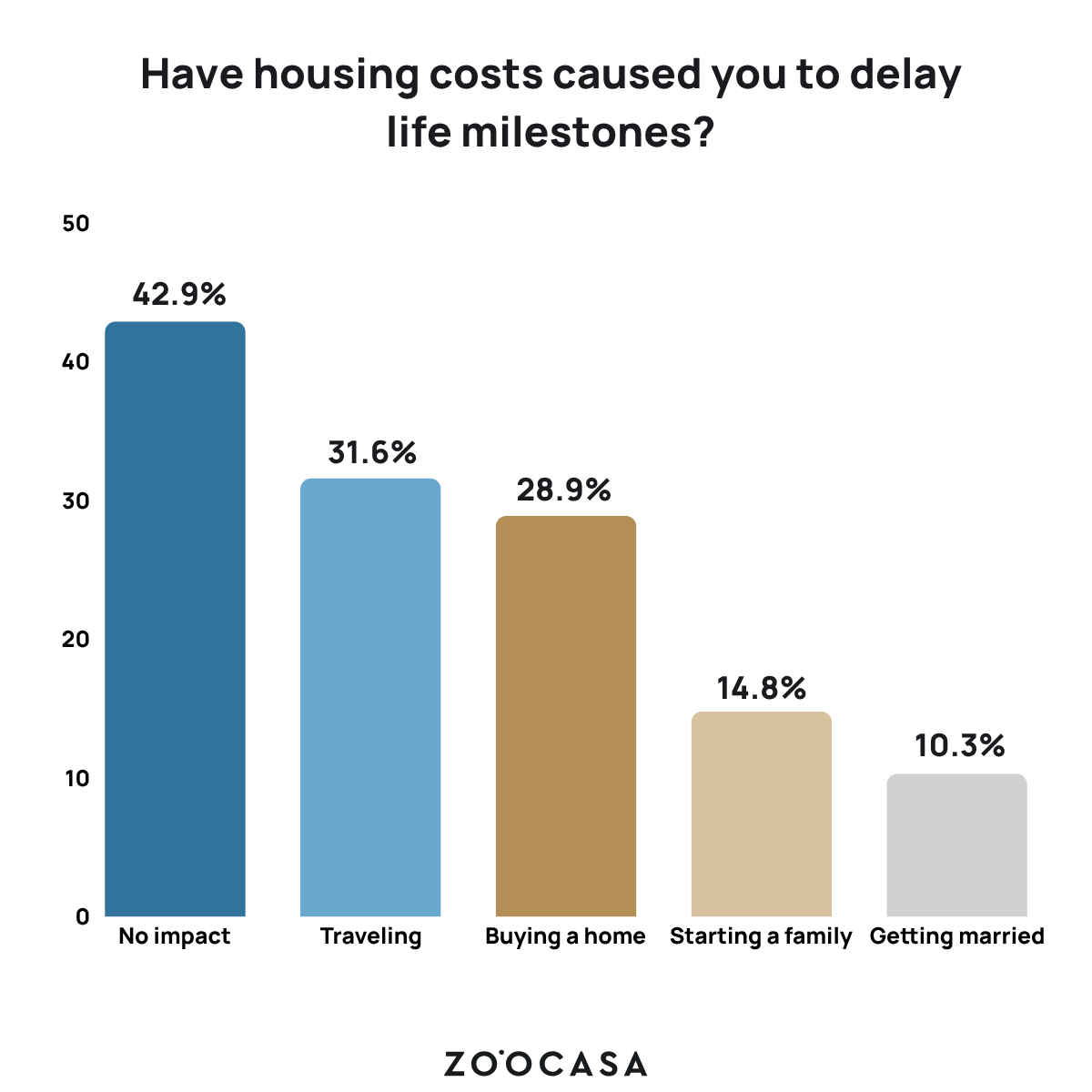

High housing costs don’t just impact day-to-day expenses like groceries; they may also force some Americans to postpone or forgo long-term financial goals. Among respondents, 31.6% reported postponing travel due to housing costs, suggesting that leisure and recreation expenses are the first to be cut when finances are strained.

Record-high home prices are also keeping some prospective buyers from entering the housing market altogether, with 28.9% saying they’ve delayed buying a home. This is causing the homeownership rate for young adults and millennials to slip.

In the first quarter of 2025, 36.6% of those under 35 years old were homeowners, compared with 40.5% in 2000. The homeownership rate for individuals aged 35 to 39 also experienced a significant decline, dropping from 64.1% in 2000 to 56.7% in 2025.

As Americans buy homes later in life, the traditional pathway to adulthood is shifting. It was once expected for young adults to go to college, get married, buy a house, and have a baby, in that order. But 14.8% of respondents have delayed starting a family, and 10.3% have delayed getting married, further complicating the route to adulthood. While 42.9% of respondents have not had their life milestones impacted by housing costs, this number could grow if historically high home prices don’t ease.

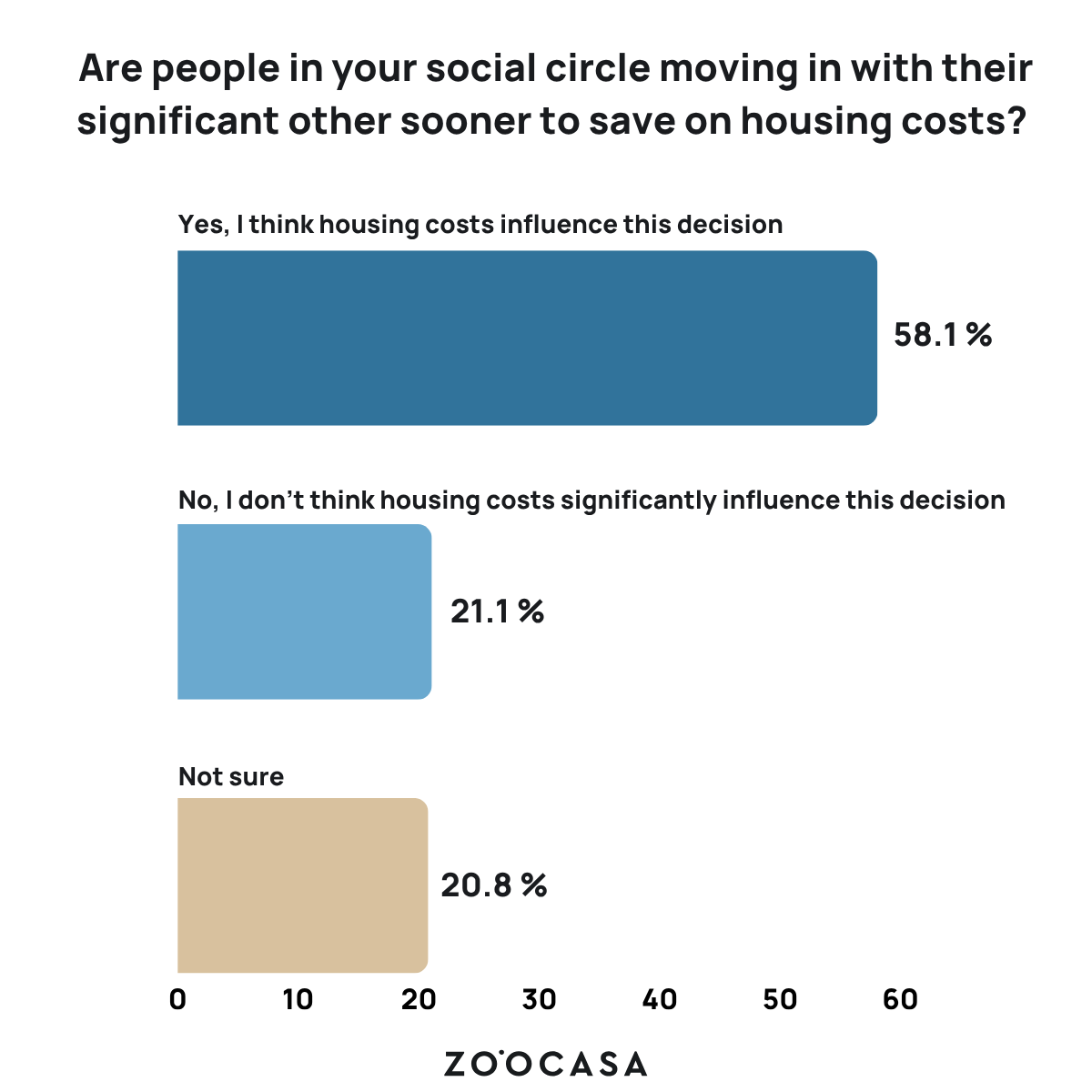

Additionally, home costs may play a role in accelerating the decision when a romantic couple decides to move in together. A majority of Americans (58.1%) believe that people in their social circle have moved in with their significant other sooner to save on housing costs.

Finding a Home Within Budget is Still Possible

Despite economic concerns, homeownership is still within reach. A majority of respondents (59.6%) said that they feel owning a single-family home is realistic for the average homebuyer in their region. A similar percentage of respondents (52%) said that they’re able to afford the average home in their area right now.

These responses reveal that Americans are generally optimistic about the reality of homeownership. In fact, 53.5% of renters said they’re planning to buy a home within the next 2-5 years, and 15.7% plan to buy within the next year. However, 22.2% of renter respondents said financial reasons prevent them from buying, and 8.7% said they aren’t interested in buying.

Stability is the leading reason renters want to become homeowners, cited by 59.6% of respondents. The desire for more space is the second most common reason, followed by the desire to build equity.

“The survey shows what many are already feeling; Americans are overspending on housing, delaying major life milestones, and bracing for financial strain,” says Lysenko. “But what’s striking is their continued belief that homeownership is still within reach. That tells us the market isn’t just stretched but rather it’s hopeful for solutions that meet people where they are.”

While homeownership may not be a financial goal for everyone, it’s still in the cards for most people if affordability improves. Like many of our survey respondents, are you thinking about buying or selling a home in the near future? Zoocasa has thousands of up-to-date listings near you. Start your search today!

Methodology:

The future of housing in the U.S. survey was conducted between April 22, 2025, and September 2, 2025. Over 1,000 American homeowners and renters were surveyed. The survey consisted of 41 multiple-choice questions to learn about the current real estate outlook of Americans. The margin of error is roughly 2%.