It’s been more than three months since the Office of the Superintendent of Financial Institutions (OSFI) implemented its infamous stress test, requiring those paying more than 20 per cent down on their home purchase to qualify at a higher mortgage rate.

Under Guideline B-20, these “low-ratio” borrowers must prove they can carry their mortgage payments at either the Bank of Canada’s benchmark rate (currently 5.14 per cent), or at their contact rate plus 2 per cent – whichever is higher. While this applies only to the qualification stage – the actual mortgage payments are made at their contract interest rate – this new hurdle has reduced affordability for the average home buyer by 20 per cent, say experts.

The fallout has certainly been evident in the form of cooler market conditions; according to the March report from the Canadian Real Estate Association, sales fell 22.7 per cent in markets across the nation, led by the most expensive urban centres such as Toronto and Vancouver, with home prices softening 10.4 per cent to an average of $491,000.

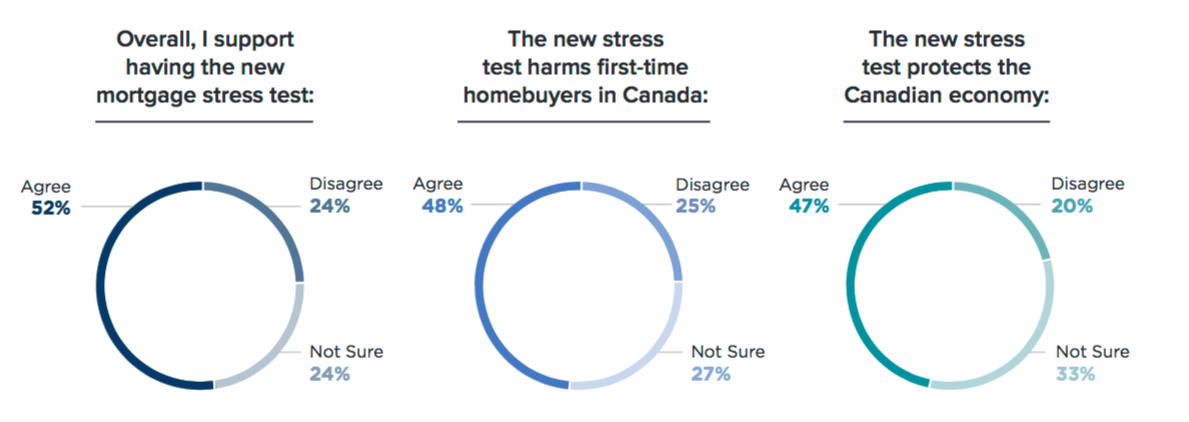

However, while the stress test has undoubtedly made it tougher for many Canadians to afford a home, they don’t appear to be harbouring hard feelings: according to the 2018 edition of Zoocasa’s Housing Trends Report: Hot Issues, which polled over 1,400 respondents from across Canada, 52 per cent say they support the stress test. Twenty-four per cent said they did not, while the remaining 24 per cent aren’t sure.

Another 47 per cent feel that the measures protect the Canadian economy, with 20 per cent disagreeing, and 33 per cent unsure.

Related Read: Report Findings – Growing Legal Marijuana in the Home

The B-20 Fallout

However, some respondents confirmed they’ve been negatively impacted financially, or have changed their minds about buying as a result of the new regulations. Of those who purchased a home between October 2017 (when B-20 was first announced, with a January 1st implementation date) and March 2018, the majority of respondents (48 per cent) indicated it did not change their purchasing timeline.

A full 27 per cent, though, said they rushed to purchase their home sooner as a result, while 6 per cent delayed buying a property. An additional 19 per cent who closed real estate deals within that timeline stated they were not aware of the stress test whatsoever.

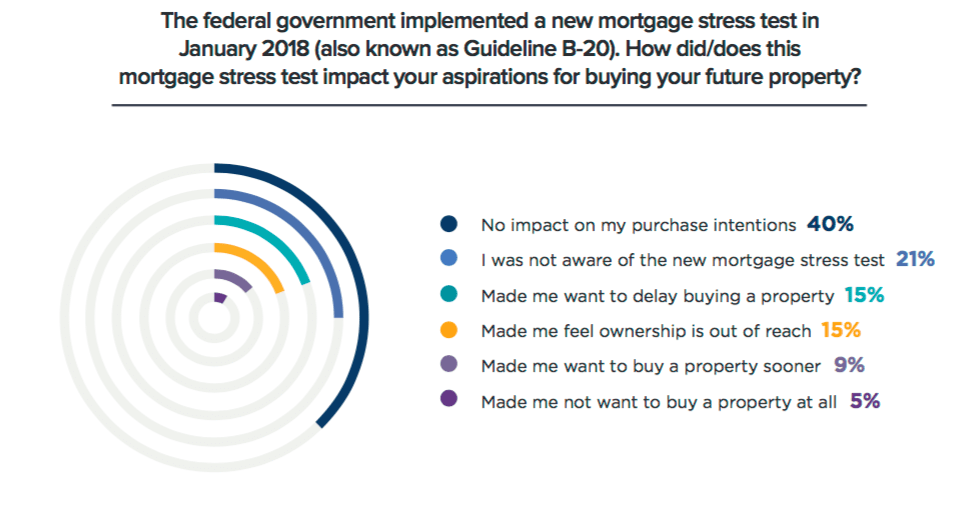

In terms of buying intentions, 40 per cent stated the stress test had not influenced their plan to buy a home – however, 15 per cent of respondents feel that it has pushed the possibility of ownership out of reach, while another 5 per cent have changed their mind altogether.