It’s no secret that life in Canada has become more expensive. A 2025 Wealthsimple survey of 2,500 Canadians found that even those earning $100,000 or more are still feeling stressed about money. Real estate prices show exactly why. Ten years ago, $100K in savings could open doors; today, it barely cracks them open.

The comparison between 2015 and 2025 makes the erosion of buying power painfully clear. Over the same period, the median after-tax income for Canadian families and unattached individuals rose from $56,000 to $74,200 — a 32.5% increase in eight years. But inflation, cost of living, and home prices have surged far faster, leaving a six-figure sum with a fraction of the reach it once had.

Toronto and Vancouver’s Reality Check

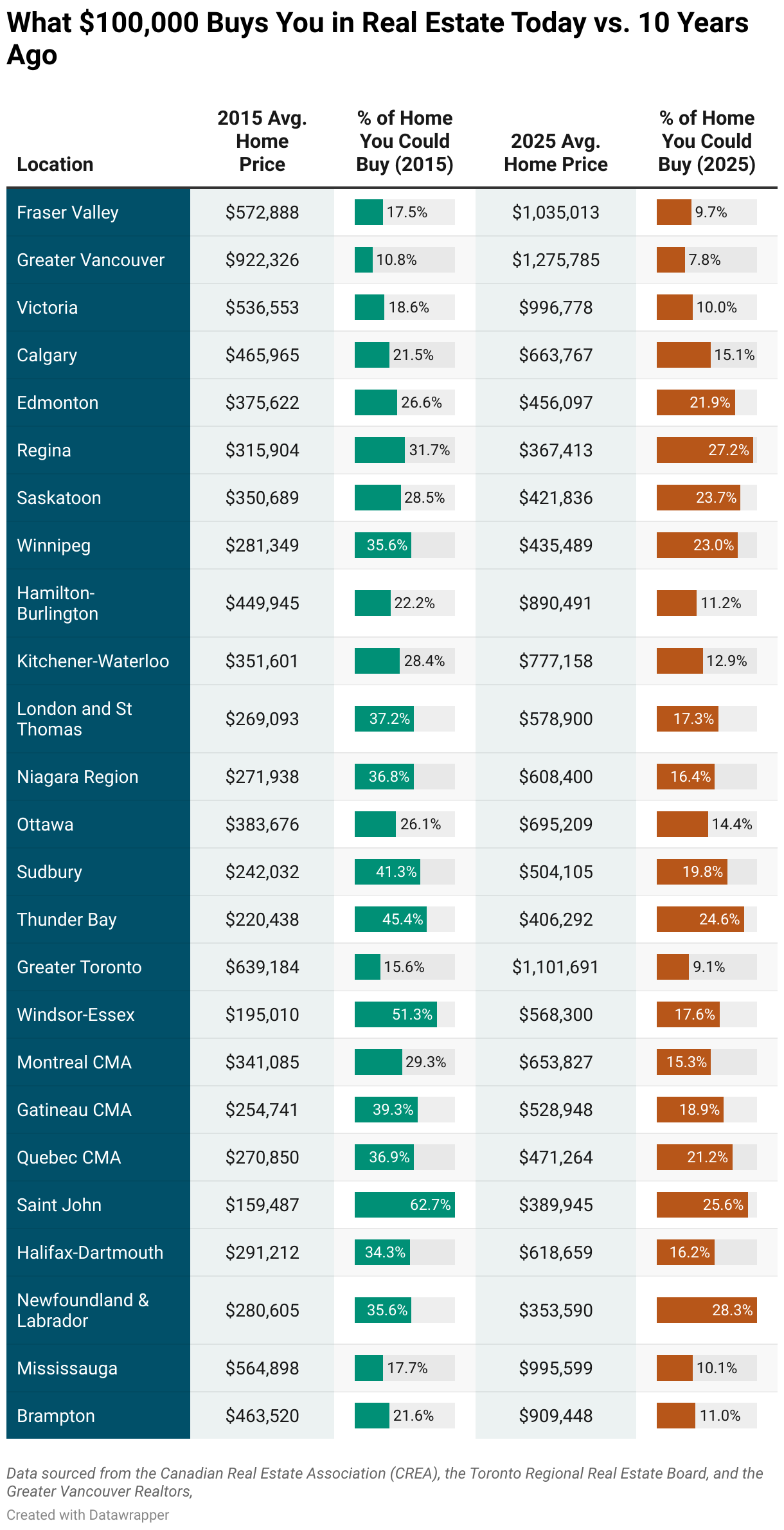

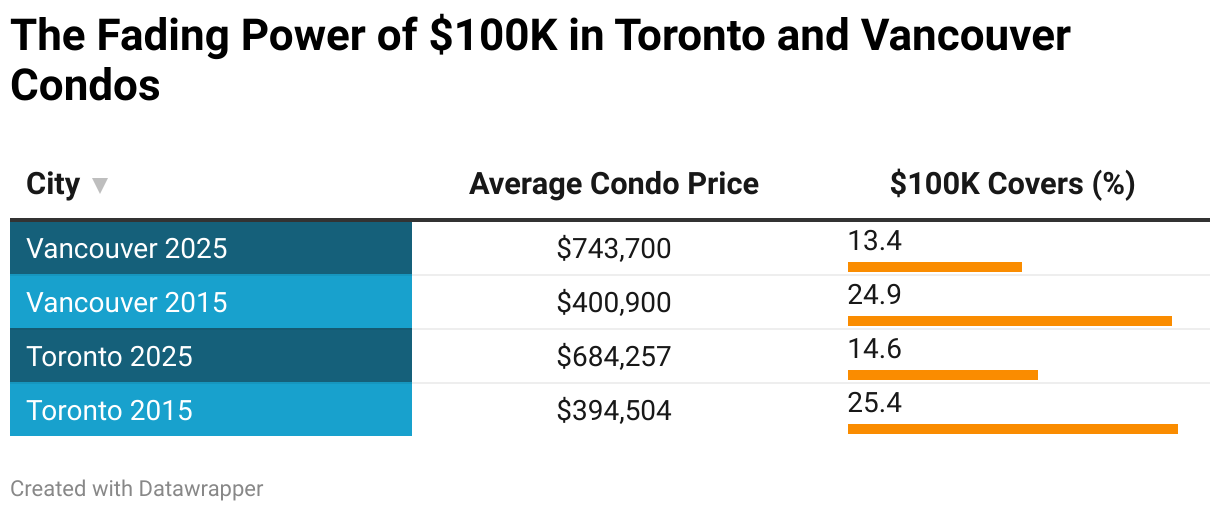

In Canada’s largest and most expensive cities, $100,000 has shifted from being a major head start to a modest boost. In 2015, that sum could cover about one-quarter of the cost of an average condo in Toronto or Vancouver, a level of buying power that could slash mortgage payments and have your pick of the market. By 2025, it barely makes a dent: in Toronto, it covers roughly one-sixth of a condo, while in Vancouver, it’s closer to one-seventh. The same shrinking power is evident across all home types, even with record-high inventory giving buyers more room to negotiate.

Pandemic Boom and Affordability Bust in Ontario’s Secondary Cities

While Toronto’s drop is steep, it’s the smaller Ontario cities that have taken the sharpest blows to affordability. Buyers priced out of major markets flooded into these regions during the pandemic, pushing up prices at unprecedented rates. In Windsor–Essex, $100,000 once bought more than half of an average home, covering 51.28% of the price in 2015. By 2025, that same amount covers just 17.59%. Niagara Region saw a similar slide, dropping from 36.78% to 16.44%, while London and St. Thomas fell from 37.17% to 17.2%. These so-called “affordable alternatives” outside the GTA have been pushed into bidding-war territory during the pandemic years, and mortgage costs have soared in parallel since.

According to a Zoocasa report published this July, Windsor–Essex recorded the largest percentage jump in mortgage payments since 2015, tripling from $903 to $2,794 per month.

Niagara Region, London and St. Thomas, and Kitchener-Waterloo all saw increases of more than 150%, with this region posting the largest dollar jump, a whopping $2,471 more per month.

The Prairie Provinces are Home to Canada’s Last Stronghold

In contrast, price growth in the Prairie provinces has been more restrained, keeping $100K’s buying power relatively intact. In Regina, it dropped only slightly, from 31.65% of the average home price in 2015 to 27.22% in 2025. Saskatoon saw a similar dip from 28.51% to 23.70%, while Edmonton shifted from 26.63% to 21.93%. In these markets, $100K still knocks a meaningful chunk off a mortgage — a rare advantage in today’s national housing picture.

From Mortgage-Free Dreams to Bidding Wars in Atlantic Canada

The Atlantic provinces tell one of the most dramatic affordability stories in the country. Saint John has shifted from being a place where $100K could nearly pay off a home, 62.7% of the average price in 2015, to just 25.6% today. Halifax–Dartmouth has fallen from 34.3% to 16.16%. Demand from remote workers, retirees, and investors has transformed these once budget-friendly areas into competitive, high-demand markets where the same savings go far less than before.

The Middle Ground: Quebec and Smaller Urban Centres

Quebec’s major cities and mid-sized urban centres like Winnipeg and Sudbury fall in the middle of the national affordability spectrum. In Winnipeg, $100K once covered 35.5% of the average home in 2015, but now buys just 22.9%. Sudbury saw a steeper drop, from 41.3% to 19.8%. In Quebec City, buying power fell from 37% to 21%, while in Montreal it decreased from 29% to 15%. These markets still deliver better value than Toronto or Vancouver, but the decline in affordability is unmistakable and gaining speed.

A Decade of Shrinking Buying Power

In 2015, dedicating $100K towards real estate would secure a substantial portion of a single-family home in many markets, covering a majority share in some cities and bringing even the most expensive condos in the country within reach.

This shift in financial security is not only evident in housing market data but also in how Canadians perceive their own savings goals. A 2025 H&R Block survey found that 85% now see living paycheque to paycheque as the new norm, up from 60% just a year earlier. Nearly half (46%) say they can’t save for long-term goals like retirement or homeownership because every paycheque is consumed by immediate expenses. Meanwhile, the same survey found that one in three people have stepped back from the idea of buying a home altogether, choosing instead to enjoy their money in the present, an understandable mindset in a market where even $100K in savings no longer opens doors the way it once did.

Similarly, a recent Zoocasa housing survey underscores the uphill battle many Canadians face when saving to buy a home. Nearly half of prospective buyers have managed to set aside more than $50,000, yet 15.1% have only $1,000 to $5,000 saved—well below the current average down payment of over $42,000. It’s a snapshot that helps explain why even $100K in savings no longer delivers the buying power it once did.

By 2025, that same budget will have diminished in value across nearly every market. While the Prairies remain one of the few regions offering relative affordability, Ontario’s smaller cities have been caught in pandemic-driven price surges, and the Atlantic provinces have shifted from affordable options to highly competitive markets. Ultimately, $100K acts more as the opening bid in a competition that’s tougher, faster, and far more expensive than it was a decade ago.