One of the biggest hurdles to homeownership is saving for a down payment while keeping up with rising rent costs. Each month, renters pay for a living place without building any equity. But just how much of that rent could have been redirected toward homeownership?

Five Years of Rent Could Cover a Down Payment—Multiple Times Over

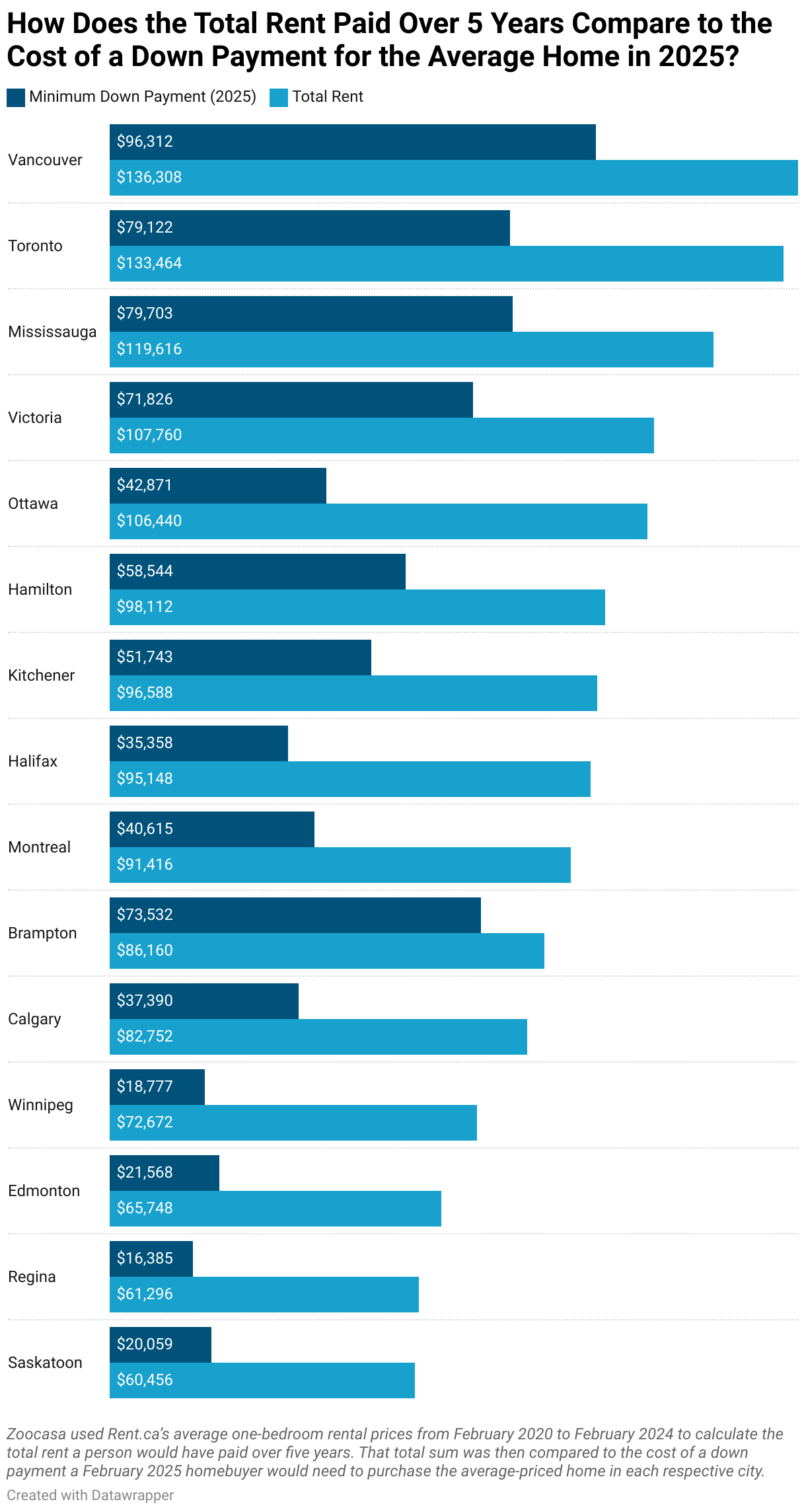

Zoocasa calculated the total rent using Rent.ca’s average one-bedroom rental prices from 2020 to 2025. The total sum was then compared to the down payment a February 2025 homebuyer would need to purchase the average-priced home in each respective city. The findings were striking: the total rent paid in every major Canadian city over that period could have covered a home’s down payment, sometimes two or even three times over.

Even in Canada’s most expensive markets to buy a home, such as Toronto and Vancouver, renters spend far more than the total sum of five years for rent compared to a minimum down payment. In Toronto, five years of rent is 69% higher than the minimum down payment for a home. In Vancouver, renters pay 41% more than they’d need for a down payment. To put this into perspective, the amount spent on renting a one-bedroom apartment for just four years could have been enough to put a minimum down payment on a home worth over a million dollars.

Over five years, the total amount spent on rent in each city could have been redirected toward a minimum down payment, covering anywhere from one to four times the amount required.

Higher Down Payments in Low-Cost Cities

Mid-range cities like Ottawa, Hamilton, Calgary, Montreal, Kitchener, and Halifax would allow renters to save the equivalent of two to three down payments, putting homeownership more within reach.

Meanwhile, five years of rent could cover three to four down payments in more affordable cities like Edmonton, Winnipeg, Regina, and Saskatoon. This means renters in these cities could have bought a home multiple times instead of paying rent or ultimately made a more substantial down payment, which would reduce overall costs in the long run.

The Fast Track to Homeownership in Lower-Cost Cities

In Saskatoon and Regina, renters could have saved enough for a down payment in less than a year and a half. A similar trend appears in Edmonton, where renters have spent nearly three times the required down payment on rent over five years—meaning they could have purchased a home in under two years if that money had been saved instead.

Even in relatively affordable cities, rent adds up quickly. Over five years, renters have spent a significant portion of a home’s value without building any equity in return.

Regional Breakdown: How Rent Costs Compare to Down Payments

The numbers across Western Canada reveal significant disparities between rent payments and down payment requirements. Winnipeg renters have paid approximately $72,672 in rent over five years, while the minimum down payment for a home is under $19,000. Five years of rent in Calgary amounts to nearly $83,000—about 16.34% of a home’s value. In Edmonton, renters have spent $65,748, roughly one-fifth of the average home’s total price.

The trend is even more concerning in cities surrounding the Greater Toronto Area. In Mississauga, the average person would spend nearly $120,000 on rent over five years—about $13,000 less than if they were to live in Toronto. When deciding whether to put that money toward rent or a down payment, a renter must pay $40,000 more than the amount required for a down payment on a home. Hamilton renters have spent nearly $100,000 on rent in five years, while the required down payment for an average-priced home in 2025 is just under $59,000.

The East Coast tells a similar story. In Halifax, renters have spent three times the required down payment in rent over five years, making the transition from renting to homeownership even more challenging.

The Hidden Cost of Renting

These numbers paint a clear picture: while renting offers short-term flexibility, it becomes a massive financial drain over time. For example, someone renting a one-bedroom in Ottawa for five years has already spent enough to cover more than a healthy 20% of a home’s purchase price, nearly $65,000 over time.

With home prices continuing to rise, the longer someone rents, the harder it becomes to break into the housing market. While it’s easy to say renters should be saving for a home instead, housing affordability isn’t a one-size-fits-all issue.

Strategic Renting: Choosing an Affordable Market

Choosing a more affordable rental market can significantly improve long-term financial planning for those with flexible jobs or the ability to work remotely. Edmonton and Calgary are two examples. Renting in Edmonton costs $1,362 monthly, leaving more disposable income for savings or investments. A renter in Edmonton could afford a home sooner, with a minimum down payment of just $21,568 (5%).

In contrast, Calgary’s higher monthly rent of $1,699 means a larger portion of income goes toward housing expenses. Additionally, Calgary’s minimum down payment is $37,390 (5.99%), jumping from renting to owning a longer-term goal. Over five years, renting in Edmonton instead of Calgary could save $20,220—money that could go directly toward homeownership.

Programs to Help Renters Become Homeowners

For renters looking to break into the housing market, several programs can help make saving for a down payment more manageable:

- First Home Savings Account (FHSA): This tax-advantaged account allows first-time homebuyers to set aside funds specifically for a down payment.

- Lower Down Payment Requirements for Homes up to $1.5M: Previously, homes priced above $1M required a 20% minimum down payment and were not eligible for mortgage insurance. Now, homes priced up to $1.5M qualify for tiered down payments, reducing the upfront cash burden for buyers in high-cost markets.

- Building Credit with Rent Payments: The Landlord Credit Bureau (LCB) allows renters to report their rent payments to credit agencies, helping them establish or improve their credit scores. This can make qualifying for a mortgage with better interest rates easier when the time comes.

Whether you’re renting or planning to buy, understanding how much rent adds up over time can help shape your financial strategy. If homeownership is the goal, taking advantage of available programs, choosing a market with lower rent, and exploring ways to build credit can make all the difference. Speaking with a real estate professional can help you create a plan to transition from renting to owning in a way that aligns with your financial situation.

Do you have questions about buying or selling in your local real estate market? Our agents can help! Give us a call today to speak with an agent in your area and start planning your next real estate endeavor.