At first glance, the Canadian and American real estate markets seem very similar. However, differences in terminology and legal processes can create confusion for cross-border buyers and investors. Familiarity with Canadian vs. American real estate terms can help avoid unexpected challenges and make more informed decisions.

Real estate terminology differs between Canada and the U.S. because the systems behind it are different. American transactions are shaped by state-level regulations and private title insurance, while Canadian transactions rely on provincial land registration systems and federally regulated mortgage lending. Add in foreign buyer and speculation taxes, and it becomes clear why some familiar terms carry different meanings.

Locking In the Deal: Deposits, Escrow and Contracts

Earnest Money vs. the Deposit

Earnest money in the United States and a deposit in Canada serve the same purpose: they show that a buyer is serious about completing a transaction. However, the way those funds are handled differs significantly.

American earnest money is typically held by a neutral third party while financing, inspection, and appraisal conditions are satisfied. Once those conditions are removed, the transaction moves toward closing.

In Canada, deposits are usually held in a brokerage trust account overseen by provincial real estate regulators. This system protects the funds, but it can also create complications if a transaction does not proceed as planned.

APS vs. Purchase and Sale Agreement

In Canada, the legally binding contract is known as the Agreement of Purchase and Sale (APS). Once a seller accepts the buyer’s offer, the agreement becomes enforceable. Most APS documents are based on standardized provincial forms, making the process relatively uniform within each province.

One feature that often surprises American buyers is irrevocability. Canadian offers typically include a deadline during which the buyer cannot withdraw the offer. If the seller does not accept or counter before that deadline, the offer expires automatically.

The U.S. equivalent may be called a Purchase and Sale Agreement, Real Estate Purchase Contract, or Contract of Sale. Although these contracts perform the same function, their structure often varies by state and may be drafted or revised by legal professionals.

Canada also uses several terms that are less common in the United States. An assignment sale allows a buyer of a pre-construction property to transfer their purchase rights to another buyer before the project is completed. A discharge refers to the document that removes a paid-off mortgage from the title. American buyers are more likely to encounter terms such as Satisfaction of Mortgage or Lien Release for the same process.

Other terms worth knowing include bridge financing, which helps buyers manage overlapping transactions, and remuneration, the term commonly used in Quebec for real estate commissions.

What Are You Actually Buying? Property Types That Don’t Translate

The “Duplex” Trap

“Duplex” is the single most misleading word for cross-border buyers.

- In Canada, major municipal zoning bylaws (Toronto, Calgary, Edmonton, Vancouver) define a duplex as one building split horizontally into two self-contained units, stacked vertically under a single land title.

- In the U.S., “duplex” is a catch-all for any two attached units on one lot—stacked or side-by-side.

- In New York City, “duplex” refers to a single high-end apartment spread over two floors connected by a private staircase. A triplex has three floors; a simplex has one floor.

Canadians use the term semi-detached to describe two homes that share a common wall. Even though the buildings are attached, each home generally occupies its own legal lot and has a separate title.

American listings may describe a similar property as a twin home or semi-attached home, depending on local conventions.

Canadian buyers should also be aware that a bungalow refers simply to a detached home with one storey. In the United States, the term may describe both a one-storey home and a particular architectural design.

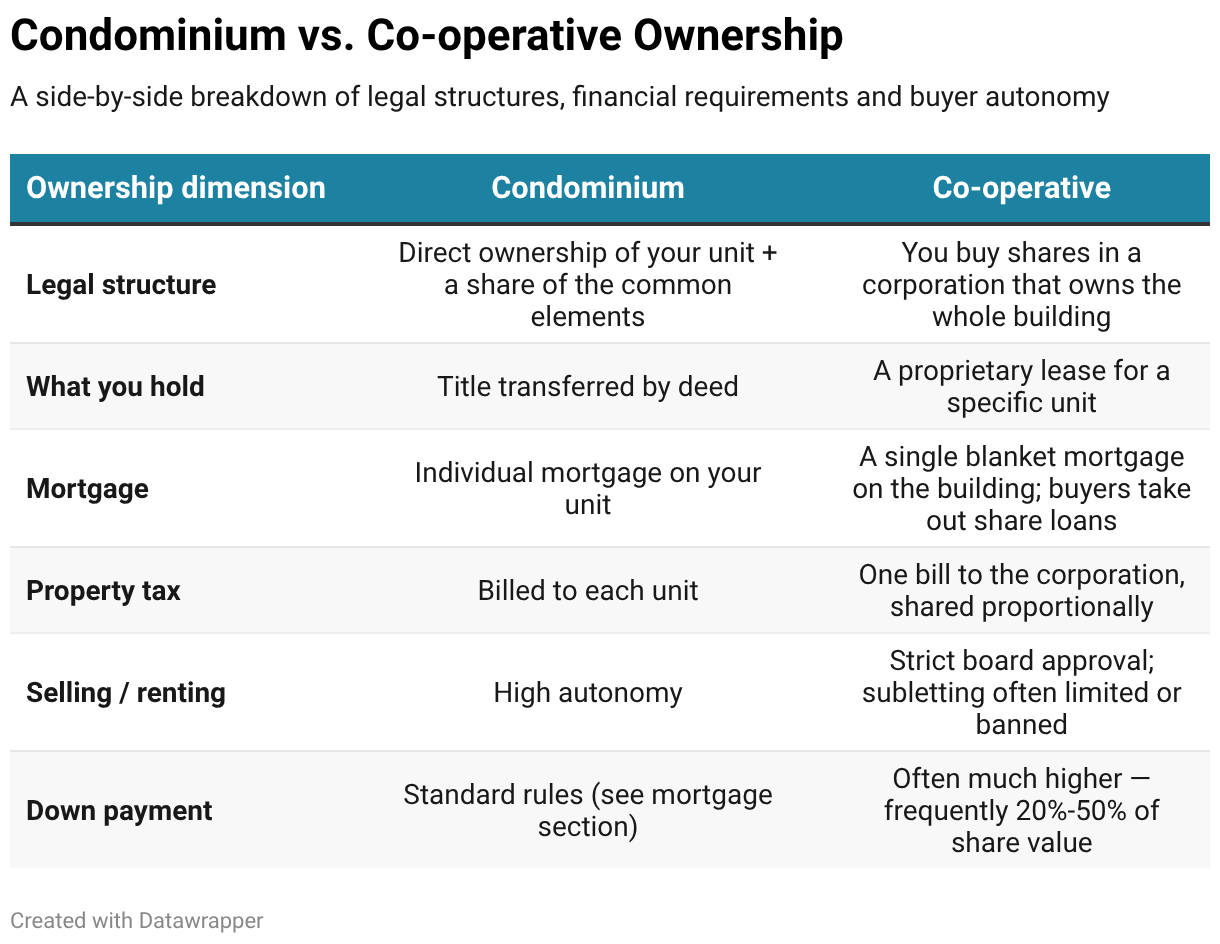

Condominium vs. Co-operative

Canadian condo owners pay condo fees, which fund the upkeep of common areas and shared amenities. These fees are similar to Homeowners Association (HOA) fees in the U.S., which help maintain community spaces and services.

A less common housing type in Canada is the co-op, where residents purchase shares in a corporation rather than owning their unit outright. Monthly maintenance fees generally cover building expenses, property taxes, and a share of the corporation’s mortgage obligations.

Quebec Speaks a Different Legal Language

Because Quebec runs on civil law (the Civil Code of Québec) rather than common law, its vocabulary stands apart from both the rest of Canada and the U.S.:

- Real property is an immovable (immeuble).

- A condo is divided into co-ownership (copropriété divise), split into fractions registered in a declaration of co-ownership.

- Owners form a syndicate of co-ownership (syndicat de copropriété) — the equivalent of a condo corporation.

- Space is split into private portions (parties privatives) and common portions (parties communes); expenses are shared by each fraction’s relative value.

- Deals close with a notary (notaire), not a title company or a lawyer in the common-law sense.

- Droits acquis (vested rights) let older buildings keep operating under a legal non-conforming status even if they’d break today’s zoning — as long as the use has been continuous.

- Quebec listings use fractions like 3½ or 4½, where the whole number refers to the main living spaces and the ½ indicates the unit includes a bathroom (not a ‘half bath’ as defined in Ontario).

The Mortgage: Where the Math Differs

Amortization Period vs. Mortgage Term

Canada keeps these two ideas separate:

- The amortization period is the total time to pay the loan off in full, capped at 25 years for default-insured mortgages, with 30-year amortizations now available to first-time buyers and buyers of newly built homes.

- Inside that, you sign a series of shorter terms, usually 6 months to 10 years (5 years is the market standard). Each term locks your rate and conditions; when it ends, you do a mortgage renewal at the current rates.

Canadian mortgages are also open (repay anytime, no penalty) or closed (prepayment limited, with penalties for paying out early beyond set annual privileges).

In the U.S., the term and the amortization are usually one unified contract, often 15 or 30 years, with the rate locked for the entire life of the loan and no renewal. Most U.S. residential mortgages are effectively open, so borrowers can refinance or prepay without penalty.

A Tax Wrinkle Worth Knowing

In the U.S., mortgage interest on a primary residence is generally tax-deductible under federal rules. In Canada, it generally is not deductible for your principal residence.

Title, Records, and Who Guarantees Ownership

Torrens System vs. Deeds Registration

Most Canadian provinces use the Torrens system, built on “title by registration.” The government register itself is the proof of ownership, so you don’t have to trace a historical chain of documents. It rests on three principles:

- Mirror: The register reflects the true state of the title (mortgages, easements, covenants).

- Curtain: You can rely on the register without looking behind it.

- Insurance: The province guarantees the title and runs an assurance fund to compensate for registry errors or fraud.

Older areas of Ontario, P.E.I., and Newfoundland and Labrador still use a traditional registry system (deeds registration), where documents are evidence of title but the state doesn’t guarantee ownership.

The U.S. has no centralized registry at all. Records are kept at the county level, where recorded deeds set priority but carry no state guarantee.

Title Insurance

Because Torrens already guarantees title, Canadians once saw little need for title insurance, but it’s now standard, largely as a cost-effective alternative to a fresh land survey that lenders would otherwise demand.

In the U.S., title insurance is essential because there’s no state-backed guarantee. A title search runs before closing, and buyers typically purchase both an owner’s policy and a lender’s policy to guard against prior claims, missing heirs, or unrecorded liens.

The People and the Rules Behind the Transaction

Designations: Salesperson, Broker, REALTOR®

Canadian licensing is set province by province:

- Sales representative/salesperson: Completed pre-registration education; must work under a licensed brokerage.

- Broker: Worked as a salesperson for a minimum period (often 24 months) plus advanced coursework; can own and run a brokerage.

- REALTOR®: A trademarked designation for members of the Canadian Real Estate Association (CREA) or the National Association of REALTORS® in the U.S., who follow a specific code of ethics.

Dual Agency and a Border Town That Needs Two Licenses

Fiduciary-duty rules differ even between provinces. In British Columbia, dual agency (one agent representing both sides) is largely prohibited, with exceptions for remote areas.

In Ontario, multiple representation is allowed under the Trust in Real Estate Services Act (TRESA), but only with written disclosure and informed consent, and the brokerage must treat both parties impartially.

Understanding Canadian vs. American Real Estate Terms

The biggest challenges in cross-border real estate are often caused by similar-sounding terms that hide important differences. From deposit versus earnest money to differences in how homes are classified and how mortgages are structured, Canadian vs. American real estate terms can easily lead to wrong assumptions.

Knowing these distinctions helps buyers and investors make more informed decisions and reduce risk before committing to a contract.

Understanding Canadian vs. American real estate terms is just the first step. Find your next property with Zoocasa. Start your search today.