The national 2018 housing market kicked off with a quieter January, as sales slowed following the implementation of new mortgage rules, reports the Canadian Real Estate Association. The numbers for the first month of the year reveal activity was down in three fourths of all markets and “virtually all major urban centres”, falling 2.4 per cent year over year, and a hefty 14.5 per cent from December.

A large portion of the slowdown was felt in Ontario’s Greater Golden Horseshoe region, which has contracted from record-breaking activity throughout 2016 and the first half of 2017. However, British Columbia markets bucked the slowing trend with sales up year over year in the Lower Mainland, Vancouver Island, and the Okanagan. Montreal, Edmonton, Greater Moncton, and Halifax-Dartmouth also saw annual gains.

CREA says much of this decline is due to the “pull forward” effect from unusually high December sales; with new mortgage qualification rules looming January 1st, many prospective buyers rushed to purchase homes before the deadline, rather than wait for the new year market.

The new mortgage rules require mortgage applicants to undergo a “stress test” to ensure they can afford their mortgage payments should rates rise. The test is anticipated to reduce affordability for the average borrower by 20 per cent, the impact of which is evident in the January market, says CREA President Andrew Peck.

“The piling on of yet more mortgage rule changes that took effect starting New Year’s Day has created homebuyer uncertainty and confusion. At the same time, the changes do nothing to address government concerns about home prices that stem from an ongoing supply shortage in major markets like Vancouver and Toronto,” he states, adding that unless such shortages are addressed, “concerns will persist.”

Related Read: Tougher OSFI Mortgage Rules to Come in January

Prices are Up, But at Slower Pace

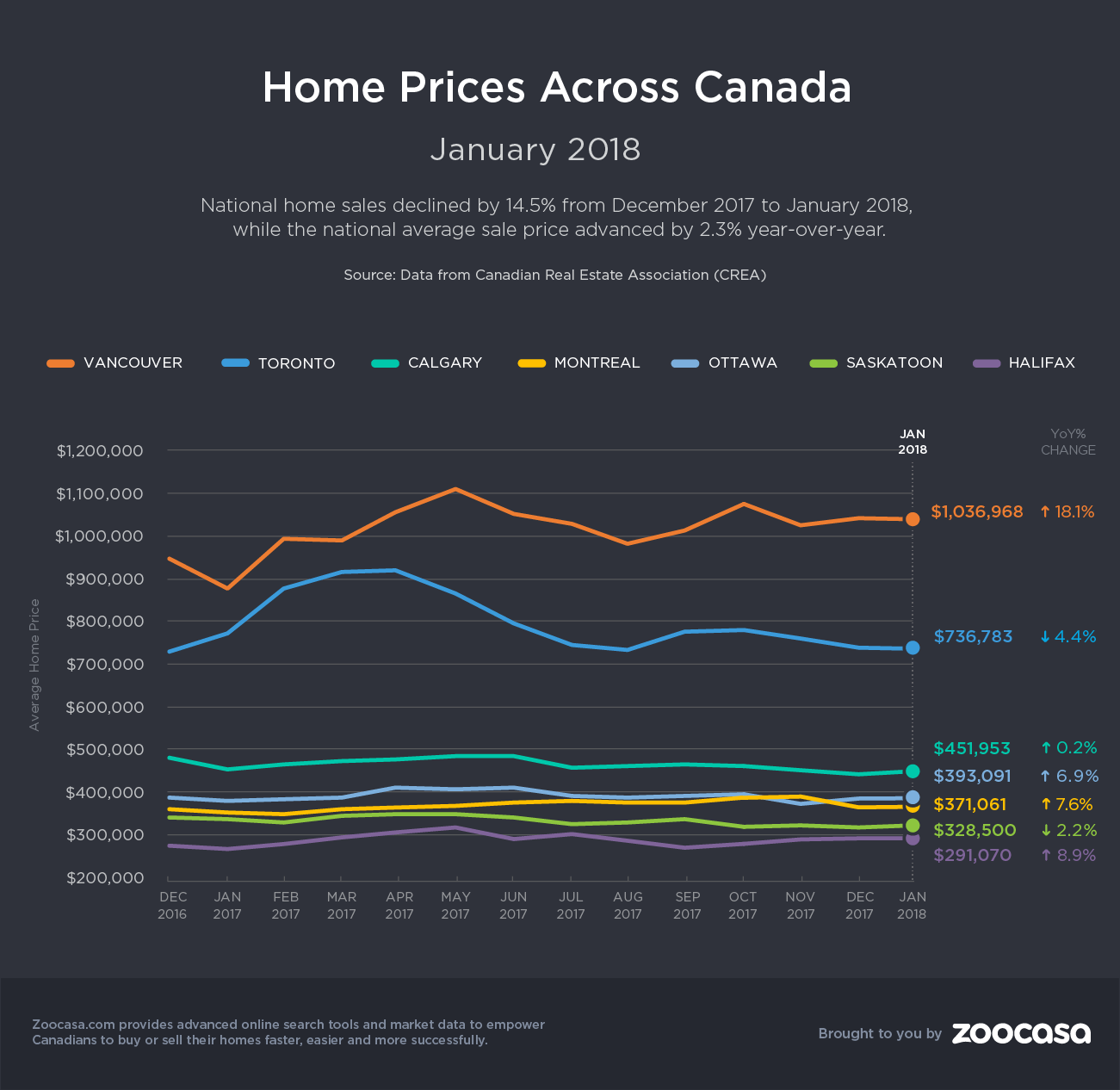

Home prices are still on the rise, though the pace of appreciation is slowing; the HPI Index rose 7.7 per cent, the 9th consecutive deceleration, and the smallest year over year gain since December 2015. The average national sale price increased 2.3 per cent to $481,500. Excluding Toronto and Vancouver would strip out a total of $107,500, to a national average of $374,000.

Annual benchmark home prices rose in nine of the 13 markets.

Lack of Listings Keeps Market in Sellers’ Territory

However, slowing activity has not led to softer buying conditions across the country. A 21.6-per-cent plunge in new listings – the lowest level since spring 2009 – has actually nudged the national market back into sellers’ territory, at a sales-to-new-listings ration of 63.6 per cent.

This ratio, which is determined by dividing the number of sales by new listings during a specific time frame, illustrates the level of buyer competition in a given region. A ratio between 40 – 60 per cent is considered balanced, says CREA, with below and above that range indicating buyers’ and sellers’ conditions, respectively.

INFOGRAPHIC: These Toronto Neighbourhoods are Now Buyers’ Markets

Says CREA’s Chief Economist Gregory Peck, “The decline in January sales provides clear evidence that the strength in activity late last year reflected a pull- forward of transactions, as rational homebuyers hurried to purchase before mortgage rules changed in 2018.

“At the same time, a large decline in new listings prevented market balance from shifting in favour of home buyers.”

Nationally, the months of inventory (the amount of time it would take to completely sell off all homes listed for sale) sits at five months, slightly below the long-term average of 5.2 months.

Growth By Home Type

Condos continue to lead the market growth, posting the largest year over year price appreciation at 20.1 per cent. Townhouses and rowhouses followed at 12.3 per cent, with one-storey single-family homes appreciating 4.3 per cent, and two-storey single-family homes up 2.3 per cent.

Activity By Region

British Columbia: All west coast markets continue to experience more-than-robust activity, as price trends reach new record highs. Values rose 16.6 per cent in Greater Vancouver, 22.4 per cent in Fraser Valley, 14 per cent in Victoria, and 20 per cent throughout the rest of Vancouver Island. The region remains in a seller’s market with a ratio of 72.3 per cent, and a benchmark price of $1,056,500.

Ontario: Much of the national slowdown can be attributed to declining sales in the Greater Golden Horseshoe markets, CREA reports – while prices have stabilized following the introduction of the Ontario Fair Housing Plan, year over year they are falling from the “rapid rise in prices one year ago”. Prices are up 5.3 per cent in the Greater Toronto region, with Guelph rising 10.9 per cent and Milton declining 1.2 per cent.

Ottawa, which has enjoyed booming interest over the past year due to its strong job market and relative affordability, saw prices rise 7.2 per cent year over year, with two-storey single-family homes leading growth at 8.1 per cent.

The Ontario region remains in a balanced market with a ratio of 55.7 per cent and benchmark price of $743,200.

Prairies: The market continues to be softer in Canada’s bread basket and oil hub, with prices down 0.5 per cent in Calgary, 4.9 per cent in Regina, and 4.1 per cent in Saskatoon. The Calgary region remains in balanced conditions with a ratio of 53.7 per cent and a benchmark price of $426,500.