When a homeowner passes away, one of the most common questions families ask is what happens to a mortgage when an owner dies. In Ontario, the answer is governed by provincial estate law, real property law, and lender policies. A mortgage does not disappear upon death. Instead, it remains a legally registered charge against the property and must be dealt with through the estate administration process.

Does a Mortgage End When the Owner Dies?

No. In Ontario, a mortgage survives the death of the borrower. It continues to exist as a secured debt against the home.

If the mortgage was in the deceased homeowner’s name only, the heirs are not personally responsible for the debt. However, the estate is responsible, and mortgage payments must continue to avoid default, foreclosure, or Power of Sale proceedings.

The estate trustee (executor) must notify the lender as soon as possible, usually by providing a death certificate. From that point forward, the lender will communicate only with the legally authorized estate representative.

How Property Ownership Affects the Mortgage in Ontario

The way a property is registered at the Ontario Land Registry Office has a major impact on what happens to a mortgage when an owner dies.

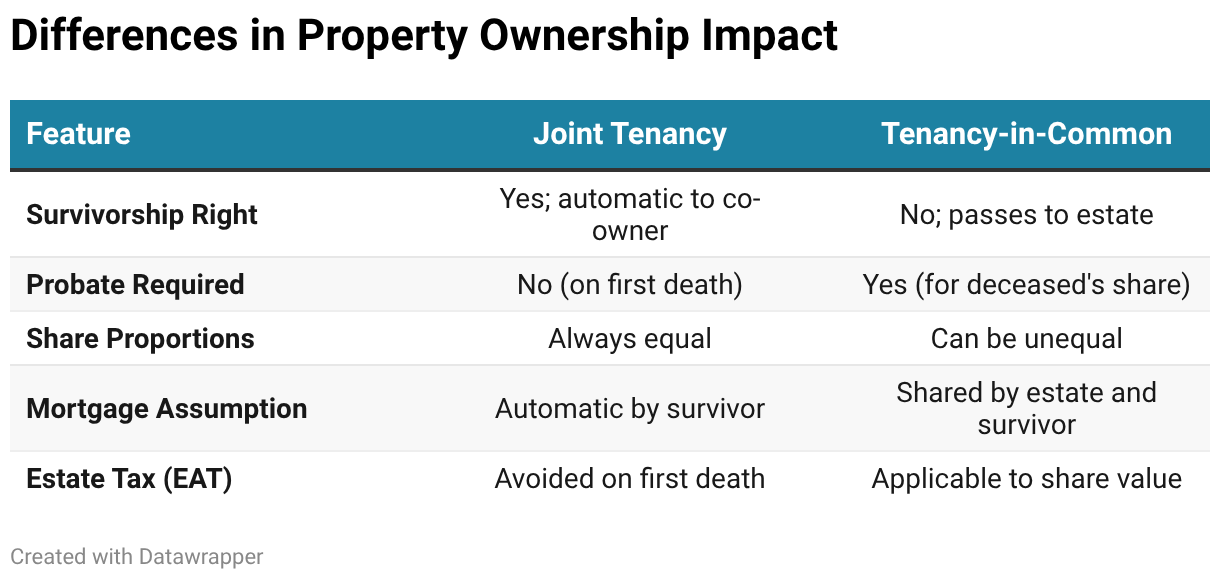

Joint Tenancy and Right of Survivorship

Joint tenancy includes the right of survivorship. When one owner dies, their interest automatically transfers to the surviving owner(s). The property bypasses the estate and does not require probate for that transfer.

The surviving joint tenant becomes the sole owner and continues making the mortgage payments. Lenders typically do not require re-qualification unless the survivor wants to refinance or switch lenders.

Joint tenancy is common between spouses. When used with adult children, Ontario courts may apply a presumption of resulting trust, requiring evidence that the ownership was intended as a gift.

Tenancy-in-Common and Estate Involvement

Tenants-in-common each own a defined share of a property. There is no right of survivorship.

When one owner dies, their share becomes part of their estate and is distributed according to their will or Ontario’s intestacy laws. The mortgage remains a shared obligation between the surviving owner and the estate, and probate is required to transfer or sell the deceased’s share.

The Role of the Estate Trustee (Executor) in Ontario

In Ontario, the executor is legally called the estate trustee. This role carries strict fiduciary duties, especially when a mortgaged property is involved.

Immediate Responsibilities

The estate trustee must:

- Secure the property

- Maintain insurance coverage

- Continue mortgage payments

- Open a separate estate bank account

- Notify the mortgage lender’s estate department

If the estate lacks cash flow, the trustee may need to negotiate temporary relief with the lender or use other estate assets to keep the mortgage in good standing.

Personal Liability Risk

An estate trustee can be held personally liable if they distribute assets before paying secured debts, including the mortgage and taxes. This is especially important in insolvent estates.

Probate and Mortgaged Property in Ontario

Probate is the court process that confirms the validity of a will and the authority of the estate trustee. Probate is usually required when real estate is owned solely by the deceased.

Without a Certificate of Appointment of Estate Trustee, the property cannot be sold or transferred. While court approval may take several weeks, full estate administration often takes 8–12 months or longer.

The First Dealings Exemption

In limited cases, a property may qualify for the First Dealings Exemption, allowing transfer without probate. This applies only to specific properties originally registered under the old registry system and is relatively uncommon.

Estate Administration Tax (Probate Fees) and Mortgages

Ontario’s Estate Administration Tax (EAT) is charged at $15 per $1,000 of estate value over $50,000.

A key benefit for homeowners is that the registered mortgage balance can be deducted from the property’s value when calculating EAT.

Insurance Options to Protect a Mortgage

Many Ontario homeowners use insurance to prevent a mortgage from becoming a burden for their family.

Mortgage Life Insurance

Mortgage life insurance pays the remaining balance directly to the lender. Coverage decreases over time, premiums often remain fixed, and underwriting typically occurs at claim time.

Term Life Insurance

Private term life insurance pays a tax-free lump sum to beneficiaries, who can decide how to use the funds. It is portable, flexible, and often more cost-effective.

What Options Do Beneficiaries Have?

Beneficiaries are not automatically responsible for the mortgage unless they co-signed the loan. However, the mortgage must be addressed if they want to keep the home.

Mortgage Assumption

Some Canadian lenders allow beneficiaries to assume an existing mortgage, subject to income and credit qualification. This can be advantageous if interest rates are lower than current market rates.

Refinancing or Selling

If a mortgage assumption is not possible, beneficiaries may refinance the mortgage in their own name or sell the property. Sale proceeds are used to pay off the mortgage, with the remaining equity distributed to beneficiaries.

Reverse Mortgages

Reverse mortgages become fully due upon death. Estates are typically given 6–12 months to repay the balance, including accumulated interest.

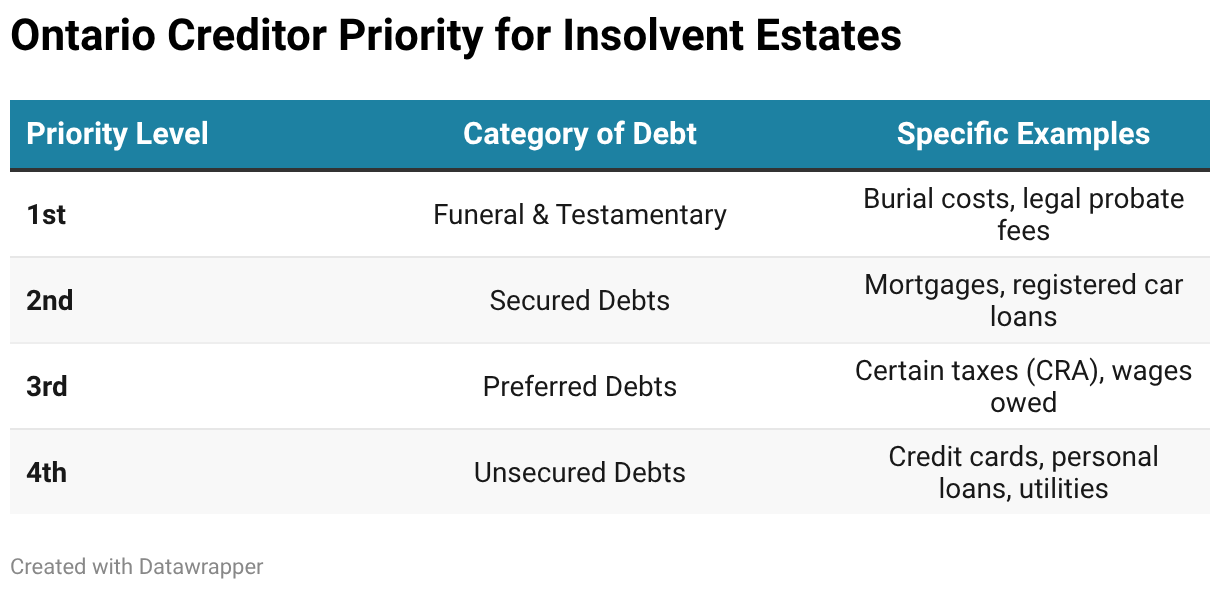

Insolvent Estates and Mortgage Priority in Ontario

If an estate has more debts than assets, creditors must be paid in a strict legal order.

If the sale of the home does not cover the mortgage and no other assets exist, heirs are generally not responsible for the shortfall.

If the Home Was Sold Before Death

If a homeowner dies after signing an Agreement of Purchase and Sale, the contract remains legally binding. Probate delays often trigger the double default doctrine, giving the estate time to complete the sale without penalty.

Planning Ahead for Ontario Homeowners

Understanding what happens to a mortgage when an owner dies can ease uncertainty during a difficult time. Although the mortgage remains in place, Ontario’s estate framework offers clear paths to manage the debt and protect inherited property.

If inheriting a home means selling or exploring new housing options, Zoocasa can help. Start your search today.