Navigating the housing market isn’t just about timing. It’s important to know which areas have stable home values and which are seeing declines. Whether you’re moving up, downsizing, or buying your first home, knowing where prices are steady can help you plan your finances this year.

So, which cities have seen the most significant price drops since the start of the year? Zoocasa looked at the Canadian Real Estate Association’s benchmark price data for 16 major Canadian markets and compared prices from January to October 2025 to find out.

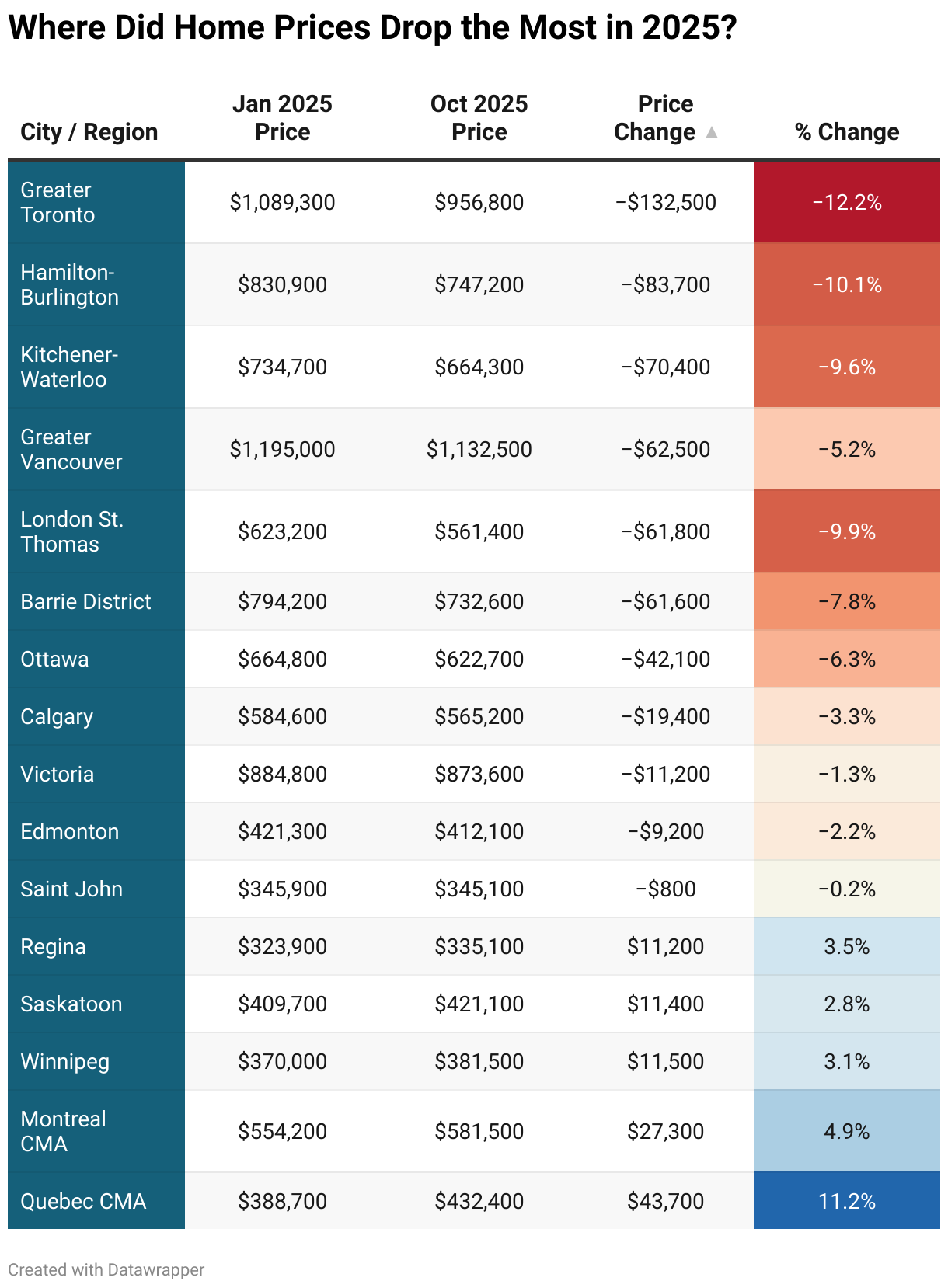

Only a Third of Major Markets Saw a Price Increase Since January

Over the past 10 months, benchmark prices fell in 10 out of 16 major Canadian real estate markets. Quebec CMA was an exception, with prices rising 11.24% since January to $432,400, up by $43,700. Montreal had the second-highest growth rate, with buyers spending an average of $27,300 more in October than at the start of the year. Winnipeg, Saskatoon, and Regina saw minor increases, all under $11,500.

Montreal and Winnipeg are Canada’s Catch-Up Markets

From January to October, housing prices in Montreal rose by 4.93%. This increase may help explain why the city’s average debt grew by 2.49%, outpacing Ottawa, Calgary, and Edmonton. According to Equifax’s Q3 2025 report, Montreal still maintains the lowest average debt at $17,315. However, rising home prices indicate that residents are relying more on credit to keep pace with the market, potentially driving debt growth faster than in other stable regions.

Winnipeg shows a similar trend, with historically low debt now rising rapidly as housing prices increased by 3.1%. At an average debt of $18,635, it is the only major city outside Quebec with debt under $20,000.

Ready to Buy? Why the Slowdown Works in Your Favour

This slowdown is due to seasonal trends and higher borrowing costs. For buyers who are ready to act, this means more negotiating power and better prices, especially in expensive markets that have seen big corrections.

With fewer first-time buyers moving from renting to owning, sellers have had to lower their expectations. Greater Toronto saw the most significant price drop, falling 12.16% since January, to $956,800 from $1,089,300. Home values in Hamilton-Burlington dropped 10.07%, or $83,700. In Greater Vancouver, prices fell 5.23%, or $62,500.

Why Alberta is Resisting the National Downturn

Calgary and Edmonton saw only some slight weakening. Unlike the bigger drops in Ontario, this looks more like a seasonal adjustment, helped by stronger financial stability. Calgary’s prices fell 3.32% (or $19,400) to $565,200. Edmonton’s prices dropped 2.18% ($9,200) to $412,100.

Financial stability sets Alberta apart from areas that experienced larger price drops. Edmonton especially stands out as a stable market. The average non-mortgage debt is $23,867 and has barely changed, rising just 0.52% over the past year. Meanwhile, Calgary’s debt grew moderately by 1.89%, a sign that Alberta households aren’t being forced to take on excessive debt, which helps prevent the distressed selling seen in more heavily leveraged markets.

The Canadian Home Builders’ Association National Municipal Benchmarking Study reports that, between 2022 and 2031, Canada is expected to build fewer homes per new resident than at any time since at least 1972.

At the same time, many people left expensive areas such as Toronto, Peel Region, and Vancouver due to rising housing costs. Many young Canadians aged 25 to 44 moved to Calgary, Edmonton, and Durham, which were the most popular choices between 2021 and 2023.

Are Canadians Filling the Gap with Credit Card Debt?

With real incomes falling and costs rising, many Canadians in big cities have turned to credit. Equifax’s latest report shows that cities with the highest rent also have the fastest-growing debt. In Vancouver, non-mortgage debt jumped 3.58% to $24,808. In Toronto, it rose 3.12% to $21,523. This extra borrowing hurts credit scores and reduces the mortgage amounts buyers can qualify for, limiting how much they can offer on homes.

What This Means for Buyers and Sellers

Although sales have increased across Canada since spring, the large number of homes for sale, especially in Ontario, gives buyers an advantage.

In most markets, buyers now have more choices and stronger negotiating power. They need to decide whether to buy at today’s lower prices or wait for more rate cuts, which could bring back competition and push prices up by spring 2026.

Meanwhile, sellers in a falling market will likely focus on selling quickly and setting the right price to avoid further drops. In a rising market, sellers aim to get the highest possible value while demand is strong.