Canada’s housing market continued to build on the rebound that began in May, with June 2025 marking a second straight month of national gains. According to the Canadian Real Estate Association (CREA), 47,871 homes were sold across the country in June, up 3.5% from the 46,237 units sold in June 2024. The national average home price in Canada was $691,643, representing a 1.3% decline year-over-year.

While still below historical highs, this uptick signals a potential turning point in market momentum. On a seasonally adjusted basis, home sales rose 2.8% from May, offering further evidence of a gradual recovery. However, new listings decreased 2.9% month-over-month, suggesting that while demand is increasing, supply has yet to catch up. Even so, the total number of active listings reached 206,435, a 11.4% increase from the previous year and just 1% below the long-term seasonal average. Overall, this is a strong sign that the market is slowly shifting back toward balance after a volatile start to the year.

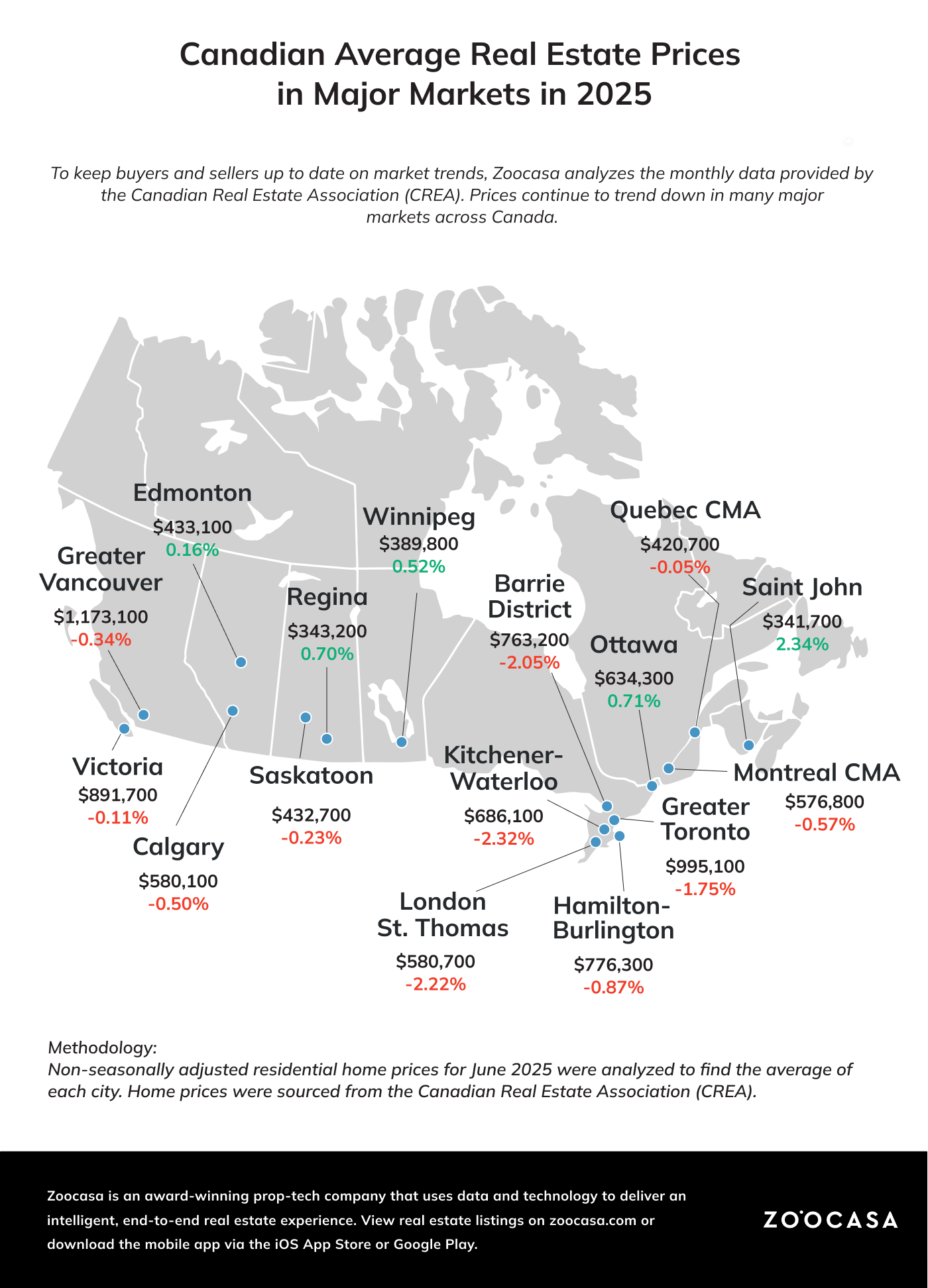

Prices Hold Steady Nationally, but Urban Centres See Declines

National home prices remained relatively stable in June, though annual comparisons showed modest declines in key urban centres. The actual (not seasonally adjusted) national average home price came in at $691,643, down 1.3% from $700,693 in June 2024. This $9,050 drop was primarily attributed to softer conditions in larger, more expensive cities.

CREA Senior Economist Shaun Cathcart noted that, “At the national level, June was pretty close to a carbon copy of May, with sales up about 3% on a month-over-month basis and prices once again holding steady.” He added, “It’s another month of data suggesting the anticipated rebound in Canadian housing markets may have only been delayed by a few months, following a chaotic start to the year; although with the latest 35% tariff threat, we’re not out of the woods yet.”

Quebec Leads the Way as Prices Surge in Smaller Cities and Atlantic Markets

Quebec remained the top-performing province on the pricing front, with the Trois-Rivières CMA leading the charge. Home prices there jumped 22.5% year-over-year, rising from $365,869 to $436,397. Meanwhile, the Quebec CMA posted a solid 13.1% gain, with prices reaching $471,238.

In Atlantic Canada, momentum was also strong. Saint John saw prices climb 18.1% to $389,945, while Halifax-Dartmouth recorded an 11% increase, bringing the average price to $618,659.

These sizeable increases across Quebec and Atlantic Canada reflect a broader trend: smaller and mid-sized cities are becoming increasingly attractive to buyers seeking affordability and lifestyle options outside the country’s major urban hubs.

British Columbia’s High-Priced Markets See Uneven Results

By contrast, British Columbia experienced mixed results. Victoria recorded a 15.6% year-over-year sales increase, with a total of 740 homes trading hands. In contrast, Greater Vancouver saw sales decline 15.4%, dropping from 3,551 to 3,004 units. The Fraser Valley followed suit with an 8.6% decrease in sales to 1,144 in June.

Price trends reflected this slowdown. Greater Vancouver’s average home price fell 5.5% year-over-year to $1,275,785, suggesting reduced buyer appetite at higher price points. Meanwhile, Fraser Valley recorded a slight increase, with prices edging up 0.8% to $1,035,013. These mixed signals point to persistent affordability concerns and growing resistance to premium pricing in some of B.C.’s most sought-after markets.

Toronto Treads Water, While Montreal Gains Ground

In Greater Toronto, the market remained relatively steady in terms of activity, with sales up just 0.5% year-over-year, increasing from 6,213 to 6,243 transactions. Despite this, average home prices fell 5.2% to $1,103,694, suggesting buyers are becoming more cautious and sellers may be adjusting expectations. In comparison, the Montreal CMA saw more substantial gains, with a 15.9% increase in sales and a 7% rise in prices, with homes now costing $653,827. Ultimately, Toronto is flatlining, and other major urban centres are regaining traction.

- Related: Canada’s Hottest Condo Market of the Last Decade Might Surprise You (It’s Not Toronto or Vancouver)

A Balanced Market Emerges, With Opportunities on the Horizon

In terms of market balance, despite fewer new listings, the number of active listings increased to 206,435 in June, a 11.4% year-over-year increase. The national sales-to-new listings ratio rose to 50.1% (up from 47.3% in May), indicating that Canada’s housing market is moving deeper into balanced territory. The months of inventory stood at 4.7, just shy of the five-month long-term average. These numbers suggest that buyers and sellers are now on more equal footing, with neither party holding a significant advantage that tips the scale either way.

Outlook: Delayed Activity Poised to Resurface

As CREA’s chair Valérie Paquin stated in the June report, “Most housing markets continued to turn a corner in June, although market conditions still vary considerably depending on where you are in Canada.” She added, “If the spring market was mostly held back by economic uncertainty, barring any further big shocks, that delayed activity could very likely surface this summer and into the fall.”

Together, these trends suggest a market in cautious recovery. While high-priced urban centres like Vancouver and Toronto are seeing adjustments, smaller cities and more affordable provinces are emerging as the new front-runners, offering buyers renewed opportunities in the third quarter of 2025.

Wondering what this could mean for your plans to buy and sell? A local agent can walk you through your options. Start your search today.