Canada’s housing market experienced minimal changes in August despite the Bank of Canada’s interest rate cut in June, the first since 2020. Many potential buyers and sellers are expected to stay cautious, holding off on further rate reductions—a trend economists anticipate to continue well into 2025.

Shaun Cathcart, senior economist at the Canadian Real Estate Association (CREA), acknowledged this hesitation, stating, “It makes sense” for buyers to wait until affordability improves. He added, “Despite some early signs of life as the long-awaited monetary policy easing begins, the housing market remains stuck in the same holding pattern it’s been in all year.”

While interest rate cuts are expected to drive demand and enhance overall affordability, CREA predicts that year-over-year comparisons will show improvement from now on. National home sales had remained flat throughout 2024, but in August, they increased by 1.3% (seasonally adjusted) compared to July, marking the highest level this year since January. Newly listed properties also experienced a slight increase of 1.1% (seasonally adjusted) during the same time. Since sales grew slightly more than new listings, the national sales-to-new-listings ratio edged up to 53%, a slight change from 52.9% in July.

Declining Prices and Sales Through Major Markets

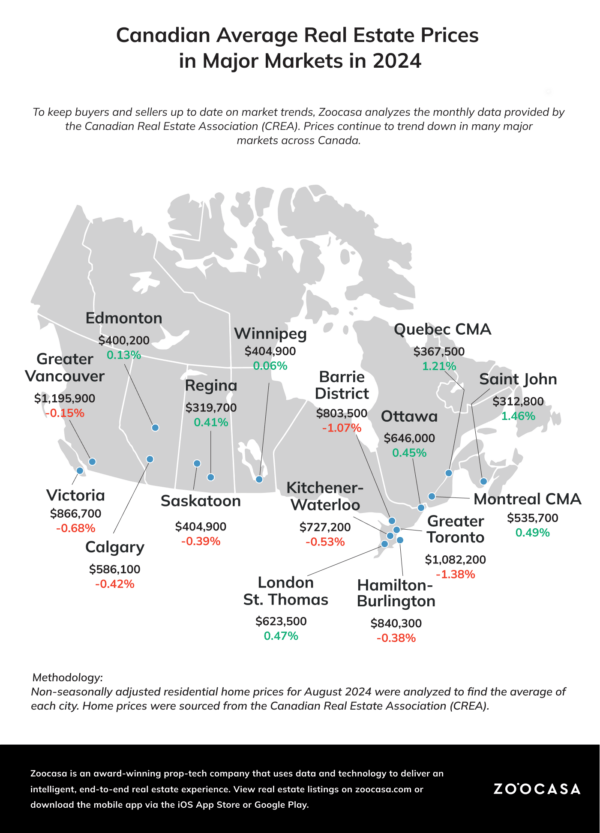

On a national level, home sales dropped 2.1% year-over-year (not seasonally adjusted), with British Columbia seeing the most significant decline—sales fell 10.8%, from 6,601 in August 2023 to 5,391 in August 2024. However, Fraser Valley was the province’s exception regarding average home prices, with a 6.0% increase year-over-year, pushing the average price back over the $1M mark, reaching $1,059,005. Meanwhile, Vancouver and Victoria faced declines, with prices decreasing year-over-year by 2.2% and 7.3%, respectively.

Ontario, which had the highest number of sales in the country, saw a 3.7% drop, falling just below 13,500 sales in August compared to nearly 14,000 the previous year. Toronto recorded just under 5,000 sales, a year-over-year drop of 6%, while Calgary and Edmonton each hovered around 3,000, with 2,891 and 2,917 sales. Although Edmonton experienced a large bump in sales – a year-over-year increase of 15.3% – Calgary’s sales were on the opposite end, declining year-over-year by 15.9%.

Alberta’s Changing Affordability

Alberta has always been known as one of the most affordable regions for homeowners in Canada, but increased demand is showcasing notable price increases. Highlighting year-over-year price changes, Alberta’s cities of Calgary and Edmonton experienced noteworthy changes. In August 2023, prices were at an average of $533,379 in Calgary but are now at $622,261, a whopping 16.7 percent more. Edmonton also saw a significant increase, with average home prices at $380,865 in August 2023 to $420,712 in August 2024.

Budget-Friendly Markets to Watch in 2024

For buyers seeking affordability, cities like Edmonton and Winnipeg offer average homes priced within the $400,000 range, while Regina and Saint John present even more budget-friendly options with homes averaging under $330,000.

Meanwhile, Quebec’s Saguenay CMA region saw home prices surge by 19% year-over-year, with the average price rising from $268,755 in August 2023 to $319,891 in August 2024.

Nationally, the average home price mainly remained unchanged, with just a 0.1% increase, bringing the price to $649,096.

Home Prices Surpass the $300,000 Average Mark

However, year-to-date average home prices saw a significant shift from 2023 to 2024, with no regions left where home prices fall within the mid-to-high $200,000 range. In Newfoundland and Labrador, the year-to-date average home price was $292,074 in August 2023, rising to $316,970 in August 2024—a 9.5% increase. Similarly, in Quebec, Saguenay’s year-to-date average home has also increased past $300,000.

“With more interest rate cuts now expected between now and next summer, the stage is set for a faster return of demand, but we’re clearly not there just yet,” said James Mabey, Chair of CREA. “There are typically four times in any given year that see a burst of new supply that can excite the market and draw buyers off the sidelines, and those are the first weeks of April, May, June, and September. So, the first week of September saw not only a third rate cut but also a lot of new properties for buyers to consider.”

Are you thinking of moving? Give us a call. As market conditions change, a trusted agent can help you prepare whether you’re considering buying, selling, or both.