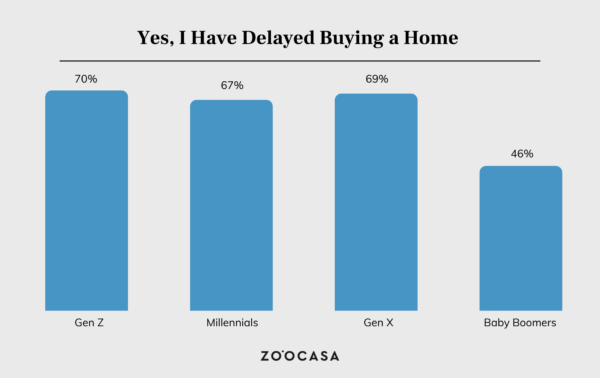

High borrowing costs are leading many would-be Canadian homebuyers to put their homeownership plans on pause. In a recent Zoocasa survey of more than 1600 Zoocasa readers, 67% of Millennial respondents said they have delayed buying a home, with the largest reason cited as high interest rates. Yet, in the same survey, 65.9% of respondents said they are looking to buy a home in the near future, indicating the dream of homeownership is still alive, but the process of getting there might be changing.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

For previous generations, one’s first home purchase may have been their forever home, or they might have bought a smaller, starter home, and then a few years down the line bought their permanent home by investing their equity. These days it might take a few extra steps to reach your homeownership goals, but it is still possible. We talked with eXp Realty agent Kristi Newman about the new trend of co-ownership and how it might be the solution potential homebuyers are looking for.

Look to the Future and Think Long-Term

“If you aren’t able to buy your dream home right now, it might be a two or three-step plan to get to that ultimate home,” said Newman. “Clients are choosing co-ownership because they either can’t get into the market or they can’t get into the market in where they want to live, especially in the GTA (Greater Toronto Area).”

Not to be confused with simply having roommates, co-ownership is when two or more people pool their resources together to purchase a property and divide the space into separate units or have some common shared amenities within the property.

“I think this is something people should seriously be considering. By getting into the market earlier, you are hedging up against inflation, building equity, and likely getting a home that is worth much more than what you could afford on your own,” added Newman.

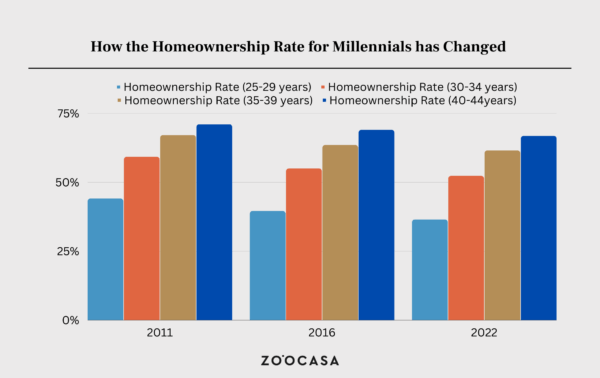

According to Statistics Canada, homeownership is on the decline for Millennials. The homeownership rate for those aged 25 to 29 years old dropped from 44.1% in 2011 to 36.5% in 2021, and for those aged 30 to 34 years old, the homeownership rate dropped from 59.2% in 2011 to 52.3% in 2021. This is markedly less than the homeownership rate for those over 50, where the homeownership rate is 72.8% for those aged 50 to 54, and 74.6% for those aged 55 to 59. With inflation remaining high and home prices unlikely to fall back to pre-pandemic levels, co-ownership may be the best option for Millennial homebuyers looking to build equity for a future home purchase on their own.

“People need to think of their home as a money generator for them because it’s a huge investment. You can hold onto your co-ownership property for 3 to 5 years, sell it, and then move up,” recommends Newman.

How it Works and What to Expect

So you’ve got your finances all sorted and are ready to enter the market, but how do you choose someone to co-buy with? “Ideally, there would be an app that could match like-minded homebuyers with each other so they could partner up,” said Newman. “You want to find someone who has the same goals as you, whether that’s an acquaintance or business partner. You can even ask your real estate broker if they know anyone who can’t qualify to live where they want solo, but could qualify with another person,” suggests Newman.

Thinking of this arrangement as a business partnership will help the co-ownership run smoothly, which is why Newman also recommends working with a lawyer. “The lawyer would know how to draft the arrangement correctly and would look at all different angles, for example, if somebody’s finances changed and they needed to sublet. The lawyer can plan for the what-ifs and make sure that the arrangement is equally beneficial to all parties.” She also suggests working with a knowledgeable mortgage broker who is trustworthy and can problem-solve.

The next step is finding the right property that could be turned into several areas and split up for the different owners. For this, you’ll want to work with a real estate agent who has handled this type of arrangement before and can visualize how a property could be split up into different parts.

The last aspect you’ll need to consider is the length of time you decide to co-own, which Newman recommends between 3 to 5 years. After that, you can use the equity you’ve built in the co-ownership property to either move up into a nicer home of your own or continue into another co-ownership arrangement.

“Sometimes you have to slow down to speed up. Slowdown meaning you co-buy and then sell in 3-5 years, and this will speed up your ability to build wealth and equity,” concluded Newman.

If you’re considering a move this fall, be it alone or as a co-ownership arrangement, let us help! Contact us today to speak with a trusted realtor about the home-buying or selling process.