Marking a continued period of stability, the Bank of Canada held its policy rate steady at 2.25% in its second announcement of 2026. By opting for its third straight hold, the Bank is exercising strategic caution, balancing domestic economic data against global risks—specifically, the threat of energy-driven inflation stemming from renewed conflict in the Middle East.

What the March Rate Hold Means for Borrowers

Penelope Graham, mortgage expert at Ratehub.ca, says the Bank is navigating a difficult balancing act. “Once again, the Bank of Canada is facing fresh geopolitical upheaval while it makes its monetary policy decision,” she explains. “With the onset of the war in the Middle East, the headwinds facing Canada’s economy have shifted; rising oil prices, if sustained, could quickly re-heat inflation growth and compel the Bank to hold off on future rate cuts, even as Canadians struggle to cope with high living costs and ongoing trade uncertainty.”

Graham adds that, given how quickly the situation is evolving, the Bank is most likely to maintain its hold on rates, “with little to no rate relief on the horizon for the remainder of this year.”

The February Consumer Price Index (CPI) data showed headline inflation easing to 1.8% year-over-year (down from 2.3% in January) largely due to base-year effects from last year’s GST/HST holiday.

Despite today’s rate hold, borrowing costs remain significantly lower than in recent years. The overnight lending rate has held at 2.25% since October 2025, following nine cuts between June 2024 and October 2025. This stability provides a degree of predictability for both buyers and mortgage holders.

What’s Happening with Mortgage Rates

Variable rates remain the most affordable option as we enter the spring market. According to Graham, variable mortgage rates remain the lowest-priced borrowing option in Canada, with a five-year variable term as low as 3.35%. She notes this will likely remain the case as long as the Bank of Canada holds its trend-setting rate. Going variable can offer borrowers strong value, provided they have the risk tolerance and room in their budget to handle future increases, or a plan to lock into a fixed rate should the Bank return to a hiking cycle.

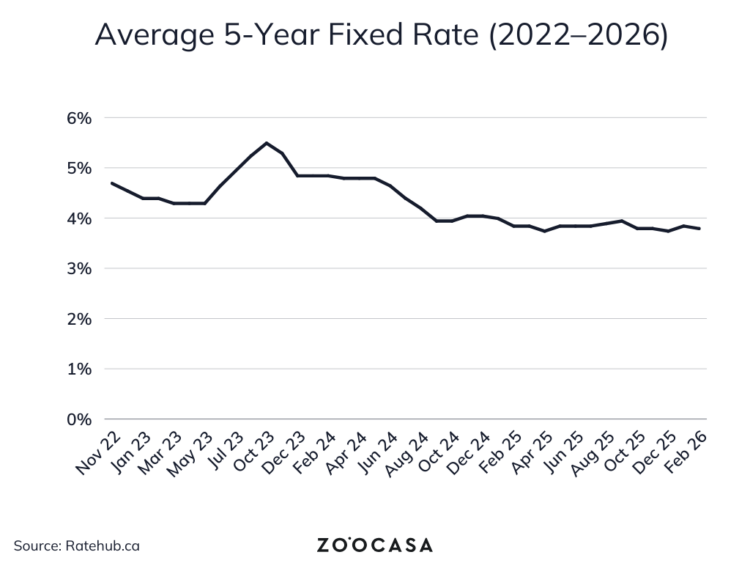

On the fixed-rate side, Graham cautions that current pricing may not hold. She points out that fixed mortgage rates remain competitively priced, with the lowest five-year term in Canada at 3.69%, but that this window is rapidly closing.

Graham highlights that rising bond yields, fueled by global inflation concerns and uncertainty around the U.S. Federal Reserve, are pressuring Canadian lenders to raise rates. With the five-year Government of Canada bond yield already exceeding 3%, further increases in mortgage rates are expected soon.

The Spring Market: Opportunity Amid Uncertainty

Nationally, the Canadian Real Estate Association’s February data paints a similar picture. Home sales came in 8.1% below year-ago levels, while the national average price held essentially flat at $663,828. New listings also pulled back, falling 3.9% month-over-month, leaving fewer fresh options heading into spring. The sales-to-new-listings ratio sits at 47.6% (within balanced territory), and months of inventory remain at five months nationally, right in line with the long-term average.

In the Greater Toronto Area, the latest TRREB data show conditions tightening slightly in February compared to a year ago. While sales were down 6.3% year-over-year, new listings declined by a steeper 17.7%, suggesting sellers are pulling back. The average selling price in the GTA sits at $1,008,968 – down 7.1% from last year. For condo buyers in particular, the market continues to offer exceptional choice and negotiating power, with elevated inventory across the segment.

Despite the uncertainty, Graham sees upside for motivated buyers. “Given rates probably won’t drop further, and labour and trade pressures remain, home buyers are unlikely to return to the housing market in droves this spring season,” she says. “However, motivated buyers will take advantage of comparably good borrowing costs, ample supply, and softer home prices.”

Looking ahead, the combination of stable borrowing costs, softening prices, and ample inventory creates favourable conditions for buyers – particularly first-time buyers who stand to benefit from reduced competition. However, as CREA has noted, when first-time buyers enter the market, they remove listings without replacing them, which could tighten supply faster than expected as activity picks up.

For those approaching mortgage renewal, it might be time to act quickly. According to the Canada Mortgage and Housing Corporation (CMHC), 1.15 million mortgages will come up for renewal in 2026. With fixed rates facing upward pressure from rising bond yields, locking in a rate hold with a lender can help hedge against further increases.

Considering a move this year? It doesn’t hurt to start looking. Browse thousands of listings on Zoocasa and explore what’s possible in today’s market.