Adding a child to a real estate title is a long-standing estate planning tactic, particularly among parents looking to simplify inheritance and reduce probate costs. On the surface, it appears efficient and cost-effective. In reality, putting a child on a property title can lead to a series of problems that often cost more than the probate fees families are trying to avoid.

Before adding an adult child to a property title in Ontario, homeowners should understand the legal, tax, and government rules that apply to these transfers.

Why This Strategy Is So Common in Ontario

Ontario’s Estate Administration Tax (EAT), often referred to as probate fees, is approximately 1.5% on estate assets exceeding $50,000. On a $1,000,000 home, that equates to roughly $15,000. Many families see adding a child to the title as an easy way to bypass probate entirely.

However, this narrow focus on probate ignores the income tax regime, trust law, land transfer tax, and family law exposure that accompany any change in ownership structure.

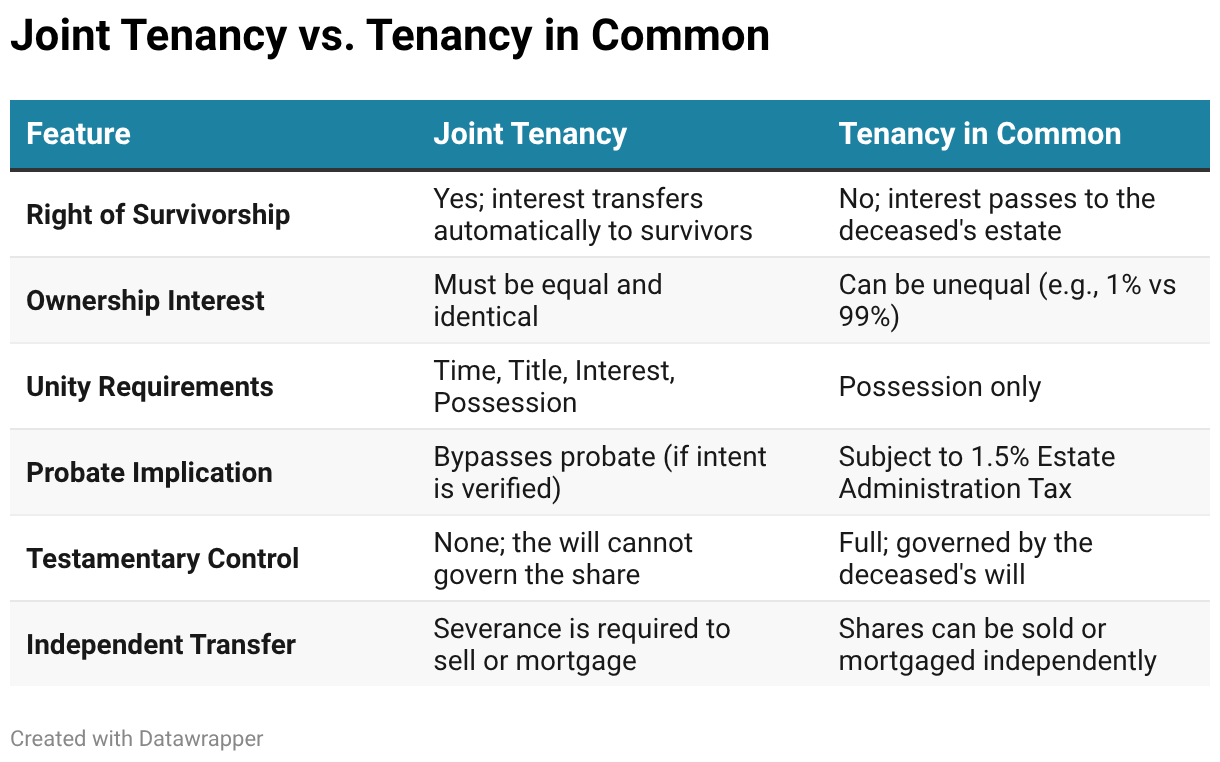

Co-Ownership Structures

Joint Tenancy

Joint tenancy requires the four unities of time, title, interest, and possession, meaning all owners must acquire identical interests at the same time and through the same instrument. Its defining feature is the right of survivorship.

When a parent dies:

- Their interest is extinguished

- The surviving joint tenant automatically becomes the full owner

- The property typically bypasses probate

Downside

The parent loses the ability to control who gets the property after death. A will cannot change the automatic transfer to the surviving owner. Even if the parent wants one child to share it with others, the right of survivorship takes over unless the matter is challenged in court.

Tenancy in Common

Tenancy in common does not require equal ownership or survivorship. Interests can be allocated strategically, such as 99% parent / 1% child, allowing parents to retain control while testing intergenerational planning strategies.

Upon death:

- The parents’ share flows through the estate

- Probate fees apply

- Distribution follows the will

This structure is often preferred in blended families or where asset division among multiple children is intended.

Why Courts Presume a Trust, Not a Gift

The Supreme Court of Canada’s decision in Pecore v. Pecore fundamentally reshaped intergenerational property transfers.

When a parent gratuitously adds an adult, financially independent child to the title:

- The law presumes a resulting trust

- The child is presumed to hold the property for the parent’s estate

- The burden is on the child to prove that a true gift was intended

Without clear and convincing proof, like a Deed of Gift or a written statement showing the parent’s intent, courts will often treat the property as still belonging to the estate, meaning it could go through probate and be divided equally among all heirs.

This creates a complex situation: families may try to avoid probate by changing the property title, only to face unexpected legal battles over who truly owns the home after a parent’s death.

Beneficial Ownership

Courts and the CRA are increasingly viewing property ownership as a bundle of rights rather than a single, unified concept, with legal title representing just one piece of that bundle.

The CRA examines:

- Who occupies the property

- Who pays the expenses and the mortgage

- Who receives rental income

- Who bears financial risk

- Who makes major decisions

Where the parent retains most of these attributes, the CRA may treat the parent as the true owner for tax purposes, regardless of title.

Capital Gains Tax

Deemed Disposition on Non-Principal Residences

Adding a child to the title of a cottage, rental, or investment property is treated by the tax authorities as if part of the property was sold at its current market value.

For Example

- Purchase price: $200,000

- Current FMV: $1,000,000

- Total gain: $800,000

- 50% added to child: $400,000 deemed gain

- Taxable (50% inclusion): $200,000 added to income

At top marginal tax rates, this can easily approach or exceed $100,000 in immediate tax, compared to $7,500 in probate fees on the same interest.

This imbalance is why adding a child to a real estate title is often financially irrational when motivated purely by probate avoidance.

Capital Gains Inclusion Rate

Recent changes and proposed updates to federal tax rules make it crucial to carefully evaluate the timing and potential consequences of adding a child to a property title, as these adjustments could substantially increase the associated financial liabilities.

A deemed sale after 2026 could significantly raise the amount of taxes owed, especially for expensive properties in Ontario that have increased in value by more than $250,000.

Principal Residence Exemption

While the PRE can shelter gains for the parent, it does not automatically protect the child’s share.

Key risks:

- If the child does not live in the home, their share accrues taxable gains

- If the child already owns a home, they can only designate one principal residence per year

- Long-term joint ownership erodes exemption efficiency

The “plus-one” rule offers only temporary relief during transition years and does not solve multi-year exposure.

Land Transfer Tax

Ontario Land Transfer Tax (LTT) is calculated on consideration, not intent. If a child assumes part of an existing mortgage:

- The assumed debt is treated as purchase consideration

- LTT becomes payable on that amount

In Toronto, this means both provincial and municipal LTT apply, often resulting in tens of thousands of dollars of unexpected tax on a “gift.”

Creditor, Bankruptcy, and Family Law Risk

Once a child is on the title:

- Creditors can register judgments

- Bankruptcy trustees can force sales under the Partition Act

- Divorce can entangle the property in equalization claims

Even if the child owns only a small percentage, courts may still order the sale of the entire property to satisfy claims.

First-Time Buyer Incentives

Being added to the title, even at 1%, can permanently disqualify a child from:

- Ontario land transfer tax rebate (up to $4,000)

- Toronto rebate (up to $4,475)

- First Home Savings Account (FHSA)

- RRSP Home Buyers’ Plan (up to $60,000)

This opportunity cost alone can exceed probate savings several times over.

CRA Compliance

Bare Trust Filings

Where a child holds legal title but no real authority, a bare trust may exist. Future CRA enforcement may require annual T3 filings and Schedule 15 disclosures, with penalties up to $2,500 per year.

Section 160: Joint Liability for Tax Debt

If a parent has outstanding tax debt at the time of transfer:

- The child becomes jointly liable

- Liability equals the value of the gift

- Interest accrues without limit

Strategic Alternatives That Preserve Value

Professionals often recommend:

- Properly structured wills or dual wills

- Alter ego or joint partner trusts (age 65+)

- Life insurance to fund probate and capital gains

- Clear documentation of beneficial ownership

These approaches preserve control, reduce tax exposure, and protect children’s financial futures.

A High-Risk Shortcut Disguised as Simplicity

In Ontario, adding a child to a real estate title is usually not a smart move on its own. The small amount of money saved on probate can easily be wiped out by big capital gains taxes, losing tax exemptions, risks from creditors, and government rules.

In the current legal and regulatory environment, a title change should be the exception, not the rule, and only undertaken with coordinated legal and tax advice.

Probate savings can disappear quickly when taxes come into play. See your real estate options clearly with Zoocasa. Start your search today.