Saving for a 20% down payment is widely regarded as one of the most effective ways to reduce long-term housing costs. It lowers mortgage payments, eliminates the need for costly CMHC insurance, and shrinks the total loan amount. But for many Canadians, the path to that milestone isn’t just challenging, it’s deeply shaped by a single factor: your job.

Across Canada, millions are struggling to keep up with the rising cost of living. As highlighted in a January 2025 RBC report, financial pressure is taking a serious toll on Canadians: 55% of survey participants report feeling financially paralyzed. Nearly half (48%) report they can no longer maintain their previous standard of living, while more than one in four (29%) admit their finances are in a constant state of chaos.

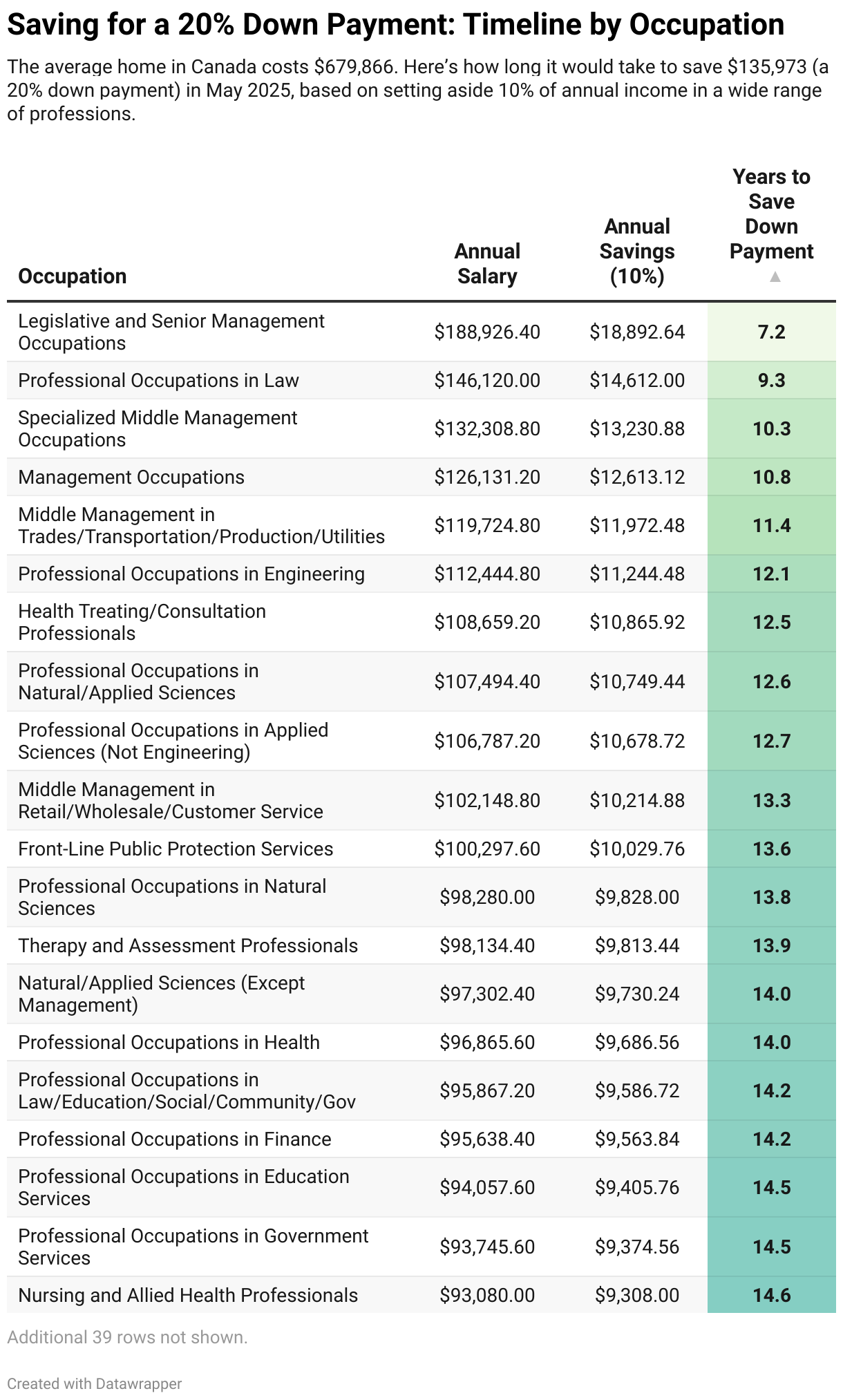

While the advantages of reaching the 20% down payment target are clear, the ability to do so varies significantly by income. For some, it’s a multi-year savings journey; for others, it’s a distant dream. Using Statistics Canada’s 2024 wage data across 60 occupations and the national average home price as of April 2025, this report breaks down how long it takes Canadians in different careers to reach that 20% down payment target if they were to save 10 percent of their annual income each year.

High Earners Save Decades Faster

At the top of the earnings ladder are executive and specialized management roles. These professions not only command six-figure salaries but also significantly reduce the time needed to save for a 20% down payment.

These professionals can realistically aim to purchase a home with 20% down in under 10–13 years, well below the national average of 17.5 years.

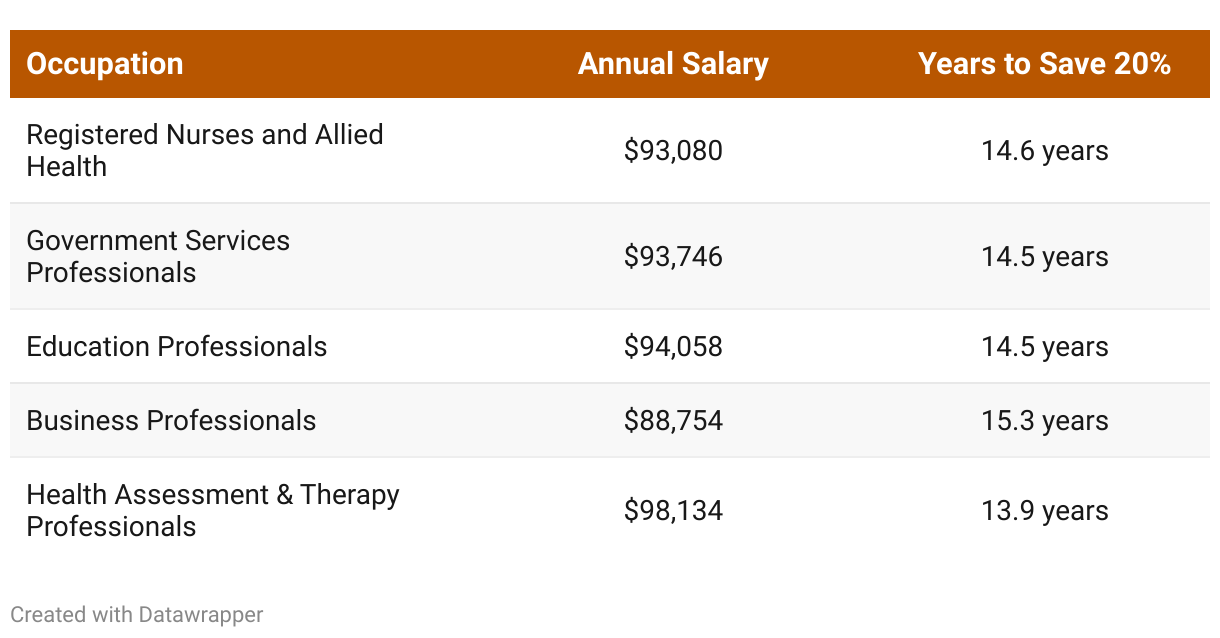

Even highly skilled professionals in health, education, science, and business are facing over a decade of savings before they reach the 20% threshold, despite earning above-average incomes. These workers often have stable incomes and job security, but face significant affordability gaps in cities like Toronto and Vancouver, where a 20% down payment can exceed $150,000.

Trade and technical roles can offer solid wages, especially in engineering-related sectors. However, for many in logistics, support, and manual roles, savings are slower due to lower base salaries.

Savings Timeline When You Earn Less Than $80,000

Even with relatively high demand and opportunities for overtime, many trades workers require 20–25 years to save for a 20% down payment if they save 10% of their income annually.

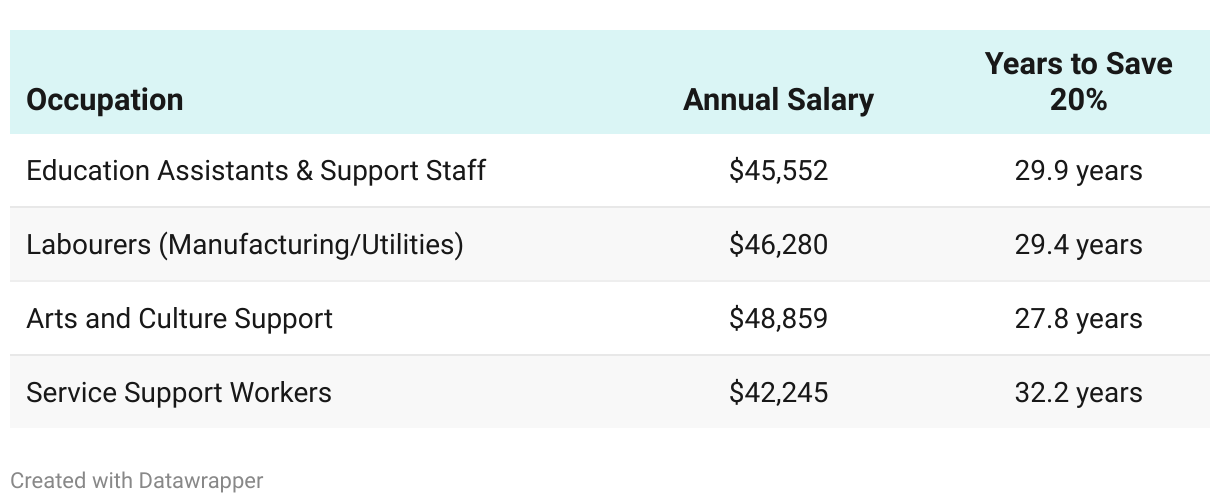

The Truth About Low-Income Savings

Those in creative, caregiving, and service occupations face the longest timelines to save a full 20% down payment, underscoring the profound affordability crisis affecting these workers. Even saving 10% per year (which is ambitious for low-wage earners) may not bring homeownership within reach without external assistance, such as a partner’s income, family gifts, or inheritance.

All in all, while a 20% down payment offers significant financial benefits, it’s often out of reach for many Canadians based solely on their income. High earners may save it within a decade, but middle-income professionals usually need 13–19 years, and lower-wage workers may wait 25–30 years. These timelines highlight why many buyers opt for smaller down payments and why support programs, affordable housing, and flexible mortgage options are essential in making homeownership more accessible.

How Far Lower Incomes Go in Affordable Housing Markets

Let’s take Newfoundland as an example, one of Canada’s most affordable housing markets, where the average home price sits at $326,741, translating to a $65,348 down payment. On the surface, that figure may seem within reach. However, for many modest earners, the path to that goal is far more challenging.

Even for modest earners, hitting that number can take over a decade. For example, a Service Support Worker earning $42,245 per year would need over 15 years to save enough by putting away just 10% of their income. Let’s say that you bump the savings up to 15%, a down payment will still take over 10 years.

While the math checks out, the reality is tough. Consistently saving 10–15% of your salary for nearly a decade or more ( while covering rising rent, groceries, and bills) is easier said than done. Even in a more affordable market like Newfoundland, saving for a home can feel out of reach without additional support, such as living at home for a few years without paying market price rent.

Why Down Payment Matters More Than Salary

For most people hoping to buy a home, the down payment plays a far bigger role than salary in determining how soon they can enter the market. While income affects mortgage approval and monthly affordability, it’s the down payment that acts as the real gatekeeper. Without it, buying a home simply isn’t possible. Saving tens or even hundreds of thousands of dollars upfront is a major hurdle, especially for first-time buyers or single-income households. Someone might earn a good salary and easily afford a mortgage payment, but without a significant savings cushion, they can’t make the leap.

In contrast, those with a modest income but a gifted or inherited down payment can often purchase a home much sooner. Ultimately, the ability to save (or access) a down payment usually determines whether and when someone can own a home, regardless of their income.

While a down payment is key to entering the housing market, income is crucial for staying there. It determines what mortgage you can qualify for and whether you can afford the costs associated with owning a home. In the end, savings may unlock the door, but income keeps it open.

Thinking of buying or selling in 2025? Search your dream home on Zoocasa.