Bare trusts are more common in Canadian real estate than most people realize. And thanks to new CRA bare trust rules, more Canadians are discovering they’ve been part of one without even knowing. If you’ve ever had someone else’s name on a title—or yours—this legal structure may apply to you. So, what is a bare trust, and why should real estate buyers, homeowners, or investors care in 2025? Let’s break it down.

What Is a Bare Trust?

A bare trust is a legal arrangement in which one person (the trustee) holds the legal title to property solely on behalf of another person (the beneficiary). The trustee has no independent power over the property, and they can only act according to the beneficiary’s instructions. The beneficiary is the true owner, enjoying all of the benefits, risks, and responsibilities associated with the property.

Bare Trust vs. Other Trusts

Unlike discretionary or family trusts, a bare trust is entirely passive. The trustee’s role is purely administrative: they hold and transfer the property as directed, without making management decisions. This simplicity is part of what makes bare trusts appealing (and sometimes confusing) in Canada, as they’re often more of a legal formality than a shift in control.

Legal and Tax Considerations in Canada

In Canada, a bare trust is not taxed as a separate entity. All income, expenses, and capital gains from the property are attributed directly to the beneficiary and must be reported on the beneficiary’s own tax return. In most cases, the trustee does not file a separate trust tax return unless specifically required by the Canada Revenue Agency (CRA).

How Do Bare Trusts Work in Real Estate?

In real estate, bare trusts often show up in practical ways. Here are a few common scenarios:

1. Parents on Title, Child is the Real Owner

Suppose Sarah buys a condo, but her parents co‑sign the mortgage and are added to the title so she can qualify for financing. Sarah pays all the bills, makes all the decisions, and lives in the home. Her parents are trustees holding legal title; Sarah is the sole beneficial owner. This is a clear bare trust arrangement.

2. Investor Structures

Investors sometimes arrange title to be held by a corporation or nominee trustee for reasons like limiting liability or for tax planning. The trustee’s role is purely administrative, while the investor retains full control, benefit, and risk. In some provinces, this approach can also help facilitate property transfers without triggering certain taxes (e.g., in specific BC or Ontario situations).

3. Partnerships or Joint Ventures

In multi‑party real estate deals, only one person or entity may be registered on title, even though two or more parties own the property. A bare trust agreement ensures the legal titleholder (trustee) acts only on the other owner(s)’ instructions and reflects the true beneficial ownership split. This is common in syndications and development projects.

4. Privacy and Confidentiality

Some beneficiaries may want to keep their name off public land records. Since anyone can look up who owns a property, a high-profile person (such as a celebrity, politician, or business owner) may not want strangers, reporters, or even competitors to know exactly where they own property. To protect their privacy, they might use a trustee company to hold legal title, ensuring their name does not appear in public searches.

Why Use a Bare Trust?

Bare trusts offer flexibility and practical benefits in real estate, but they’re not just about convenience. In Canada, common reasons to use a bare trust include:

- Estate Planning: To avoid or reduce probate, simplify future transfers, and ensure smoother succession of ownership without having to change legal title upon death.

- Family Transfers: To help children or spouses buy property, where someone else temporarily holds legal title but the beneficiary keeps all control, benefits, and responsibilities.

- Tax Planning: To coordinate property ownership with other entities as part of a larger tax strategy. For income tax purposes, however, the bare trust is generally ignored – the beneficiary must report all income, expenses, and capital gains.

- Liability Protection: When paired with corporations or nominee companies, a bare trust can separate legal title from beneficial ownership, reduce liability exposure, and create a clear ownership record.

- Investment & Joint Venture Structures: To simplify multi‑party ownership by designating a single trustee on title while documenting each party’s beneficial share in an agreement.

However, a bare trust is still a formal legal arrangement. It involves proper documentation, may require legal fees, and—due to recent CRA rule changes—often comes with reporting obligations. In some cases, trustees must now file trust information returns, even when there is no income.

What Are the CRA’s Bare Trust Reporting Rules?

Until recently, bare trusts received little attention from the CRA. However, new legislation introduced in 2023 has significantly expanded reporting requirements for bare trusts, especially those holding real estate or other assets.

Key Points

- Who Must Report: Most bare trusts holding real estate or other assets will be subject to the new reporting rules starting with the 2025 tax year (filings due in 2026), subject to some exceptions for small trusts or certain family/homeowner situations.

- What Is Required: A T3 Trust Income Tax and Information Return must be filed, including Schedule 15 (Beneficial Ownership Information of a Trust). This requires detailed information about both the trustee(s) and the beneficiary(ies).

- Reporting Details: Unlike other trusts, bare trusts generally report no income or capital gains because these are attributed directly to the beneficiary. The T3 filing for bare trusts mainly focuses on ownership disclosure.

- CRA Transitional Relief: The CRA waived mandatory bare trust filings for the 2023 and 2024 tax years to reduce confusion and administrative burden.

- Penalties for Non-Compliance: Penalties for failure to file a required T3 return can be up to $2,500, with higher penalties for deliberate avoidance or fraud.

- CRA’s Position: The CRA considers these rules critical for transparency in property ownership and tax compliance. Common situations, such as parents holding property on behalf of children, are within this reporting regime.

If you are involved in a bare trust in Canada, you likely have reporting obligations beginning with the 2025 tax year. It is important to ensure all paperwork is filed correctly and timely, and to remain up to date on CRA guidance and any future legislative changes.

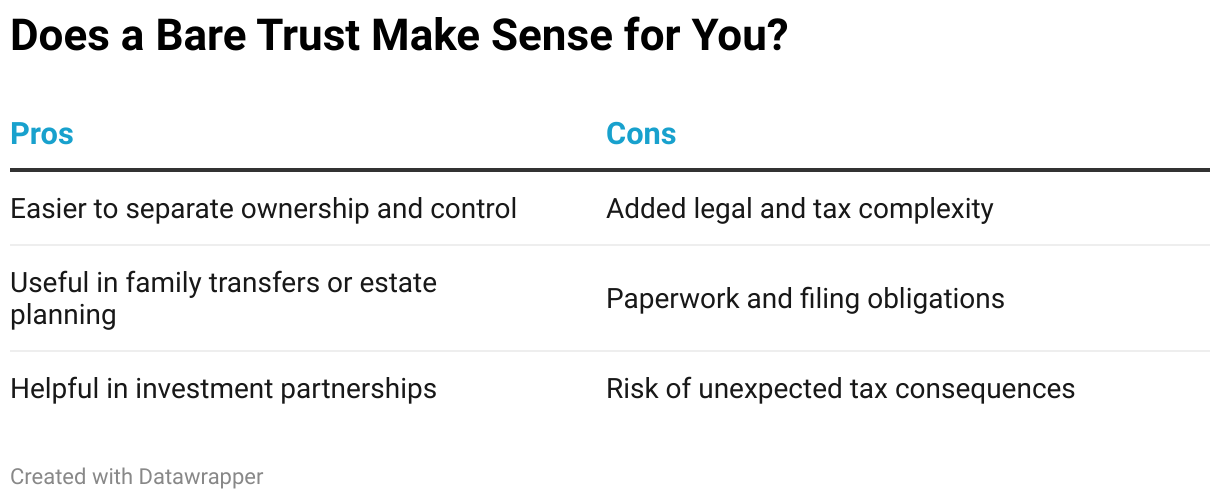

Does a Bare Trust Make Sense for You?

Like any legal structure, a bare trust has its pros and cons:

A bare trust can be incredibly useful, but it’s not a shortcut. Always speak to a real estate lawyer and tax advisor before setting one up.

Know What You’re Signing Up For

A bare trust can make homeownership or real estate deals more accessible and flexible, but it also comes with legal and tax obligations that many people overlook. With the CRA bare trust reporting rules now in effect starting with the 2025 tax year, it’s important to take action.

What to Do Now

- Review your property title and ownership documents.

- Determine whether a bare trust arrangement exists (even informally).

- Consult a tax advisor or real estate lawyer to confirm your obligations.

- File the required T3 Trust Income Tax and Information Return (including Schedule 15) if your bare trust meets the new reporting rules.

Buying with help from family? Understand how bare trusts may impact your ownership and taxes. Start your search today with Zoocasa.