Does it make more financial sense to rent or buy your home? The pros and cons of either scenario have long been debated by money pundits; it was once considered savvy for savers to invest their down payment sums as an alternative to homeownership, while enjoying the lower housing costs and fewer responsibilities that come with renting your home.

But that approach harks back to a time when renting in Toronto was still a feasibly affordable alternative; today, the average 416 rental apartment commands $2,417 per month, according to the Toronto Real Estate Board’s Q2 rental report. For a Torontonian earning the city’s median single income of $39,560, that consumes 73.3 per cent of their pay; financial experts mandate housing costs should account for no more than 30 per cent of an individual’s income.

A Classic Supply and Demand Crunch

Toronto rents have skyrocketed in recent years as steep demand and too-little supply keep the vacancy rate below 1 per cent – a historical low. TREB’s report finds that the rate for the average one-bedroom unit increased 10.4 per cent year over year in Q2, to $2,055.

Two-bedroom unit rents rose 8.8 per cent to $2,755, while three-bedrooms now cost $3,469 on average – an annual increase of 10.2 per cent. Even bachelor units, once considered the most affordable entry point into the rental market, fetch an average of $1,716 (an increase of 10.6 per cent). That still accounts for 52 per cent of income for a solo earner.

TREB President Garry Bhaura says that with demand for rentals steadily increasing, more needs to be done at the policy level to ensure supply is available and remains affordable for Toronto residents.

“The demand for condominium apartment rentals remained strong compared to the number of units available for rent. Current market conditions point to the fact that renters have little choice when it comes to finding a place to live,” he says. “Governments need to look at ways to increase the supply of rental accommodation, both in terms for purpose-built rental properties and individual investor-held units. This would go a long way to easing the pace of rent growth in the GTA.”

New Rent Controls Still Controversial

This was a challenge the Ontario government tried to address in April 2017, when it introduced new rent controls and tenant compensation rules as part of the Fair Housing Plan.

The rules cap rent increases upon lease renewal at the rent increase guideline (currently 1.8 per cent) prescribed by the province. Prior to this, only units built before 1991 were subject to rent controls, meaning landlords could increase rents as they saw fit when tenant leases came up for renewal.

While support for rent controls has been high – 56 per cent of Canadians polled by Zoocasa agree they’ve helped with rental affordability – there are concerns they’ll have the opposite effect. The caps do not apply to rents on brand new leases, or increases required to pay for extensive renovations or upgrades. Critics have pointed out this does little to cool overall market prices, and encourages “renovictions”, the practice of kicking tenants out to update units, raise the rent, and lease them out anew.

The rent caps have also been derided for dissuading developers from creating new rental-purpose units, as well as would-be landlords from renting their privately-owned condo units; 53 per cent of Toronto rentals are privately owned, according to StatsCan, accounting for a significant portion of rental inventory in the city.

“Recent government policy changes, including rent controls, have not alleviated the strong upward pressure on monthly rents for available condominium apartments in the GTA,” says Jason Mercer, TREB’s director of market analysis. “New, investor-held condominiums entering the market have not been enough to provide the needed balance in the condo rental market. As a result, the strong competition between renters continues to sustain double-digit or near double-digit annual average rent increases.”

Should Rent Be More Than a Mortgage?

Meanwhile, in the resale ownership market, TREB reports the average value for Toronto condos rose 6.5 per cent to an average of $603,480 over the same time period. That would require a monthly mortgage payment of $2,297 (assuming a 20-per-cent down payment, 3.05-per-cent mortgage rate, and 25-year amortization), and actually comes to $120 less spent per month on shelter costs.

Related Read: Where Can You Buy a Toronto Condo for Less Than Average?

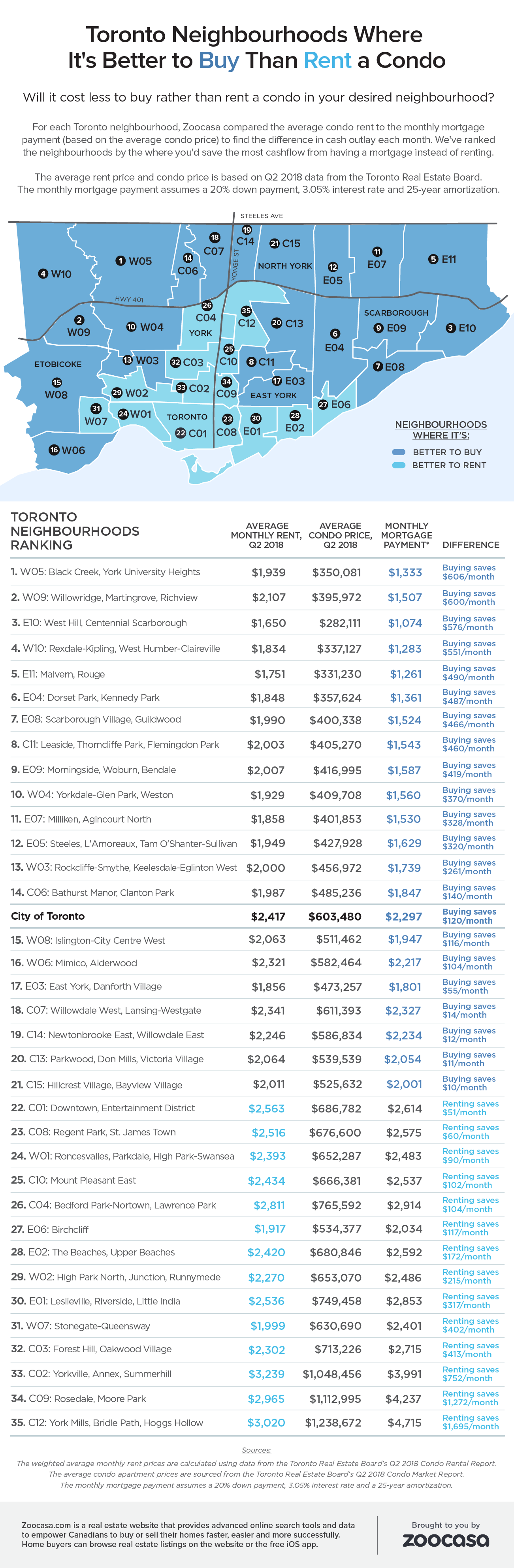

Toronto Neighbourhoods Where It’s Better to Buy Than Rent a Condo

To find out how condo and rental apartment affordability compares across the City of Toronto, we looked at the average monthly rent and average condo price in each 416 MLS district. According to the calculations, it makes more financial sense from a monthly payment perspective to own rather than rent in 21 of the 35 neighbourhoods studied.

Check out the infographic below to see where in the City of Toronto you’d save the most cash flow by owning your home instead of renting it. (Calculations are based on average price only and do not include condo fees, insurance, utilities, etc.)