Buying a home in Canada this year? The mortgage stress test is one of the first hurdles you’ll face. It’s not new, but the rules have shifted heading into 2026. Whether you’re a first-time buyer or coming up on a renewal, understanding how the Canadian mortgage stress test works helps you set a realistic budget and avoid surprises at the approval stage.

Here’s what you need to know.

What Is the Mortgage Stress Test?

The mortgage stress test is a federal rule. It ensures you can afford your mortgage payments even if interest rates rise.

Instead of qualifying at your actual contract rate, your lender uses a higher “qualifying rate.” Think of it as a built-in safety buffer. If rates rise after you lock in, you should still be able to make your payments.

The stress test applies to all new mortgage applications, refinances, and, in most cases, lender switches. It doesn’t matter how much you put down.

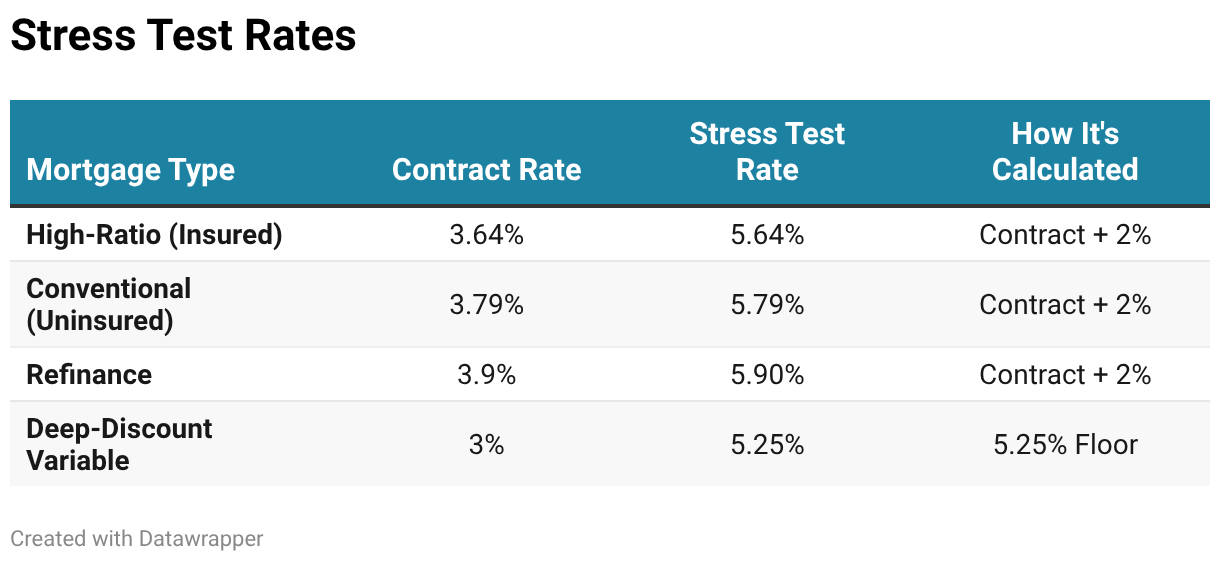

How Is the Stress Test Calculated?

In 2026, you must qualify at the higher of two rates:

- Your contract rate plus 2%

- The floor rate of 5.25%

The larger number is your qualifying rate.

As of March 2026, the Bank of Canada’s policy rate sits at 2.25%. Most contract rates are low enough that the “contract rate plus 2%” calculation applies. For example, if your lender offers you a 5-year fixed rate of 3.79%, you need to prove you can handle payments at 5.79%.

Here’s how that breaks down:

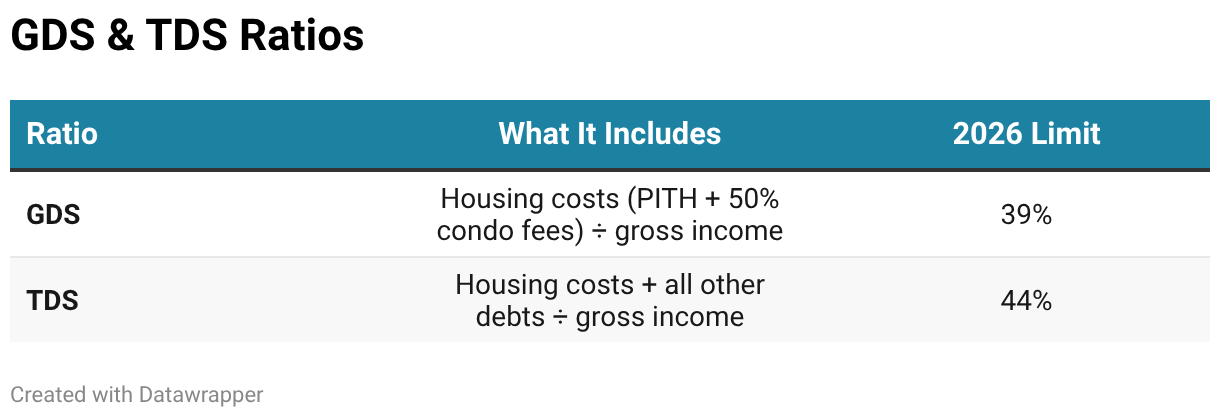

GDS and TDS: The Debt Ratios You Need to Pass

The qualifying rate is only part of the picture. Your lender also checks two ratios to make sure your overall debt load is manageable.

Gross Debt Service

The Gross Debt Service (GDS) ratio measures your housing costs against your gross income. This includes your mortgage principal, interest, property taxes, heating costs, and 50% of any condo fees. For insured mortgages, your GDS can’t exceed 39%.

Total Debt Service

The Total Debt Service (TDS) ratio adds your other debts on top of housing costs. Car loans, student loans, credit card minimums—they all count. The cap for insured mortgages is 44%.

Both ratios use the stress test rate, not your actual contract rate. Your real monthly payment will be lower, but you need to show you can handle the higher one.

The $1.5 Million Insured Mortgage Cap

One of the biggest recent changes is the insured mortgage price cap. It jumped from $1 million to $1.5 million on December 15, 2024. Before this, buying anything over $1 million required at least 20% down payment. That’s no longer the case.

Now, buyers can purchase homes up to $1.5 million with a smaller down payment:

- 5% on the first $500,000

- 10% on the portion between $500,001 and $1,499,999

For a $1.2 million home in Toronto or Vancouver, the minimum down payment dropped from $240,000 to $95,000. That’s a major difference.

This opened the door for buyers who had the income to pass the Canadian mortgage stress test but didn’t have the savings for a 20% down payment. Keep in mind, though, that mortgage insurance premiums are added to your loan and are stress-tested along with it.

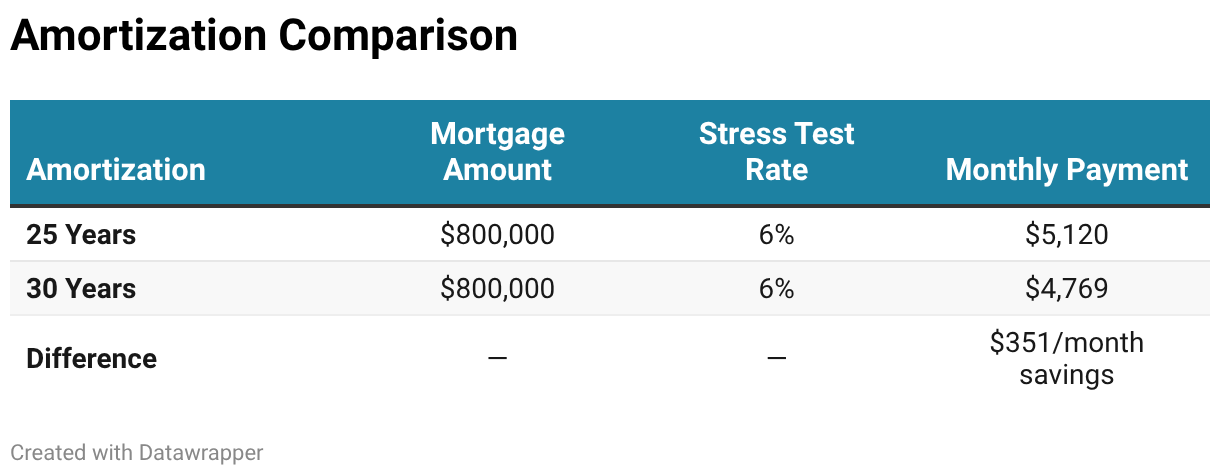

30-Year Amortizations

To help with the higher costs that come with larger mortgages, the federal government expanded 30-year amortization periods for insured mortgages. Two groups qualify in 2026:

- First-time homebuyers (any home type)

- Buyers purchasing a newly built home (any buyer type)

Why does this matter for the stress test? The test is based on your monthly payment. Stretching payments over 30 years instead of 25 lowers that monthly number, which lowers your GDS and TDS ratios.

Here’s an example:

That $351 monthly difference could bring your GDS from 42% (a fail) down to 38% (a pass). It could be the difference between getting approved and getting declined.

The Loan-to-Income (LTI) Cap

The stress test checks whether you can handle higher rates month to month. The LTI cap looks at something different: how much total mortgage debt a lender can hand out relative to borrower income.

Under the 2026 rules, federally regulated lenders must keep no more than 15% of their quarterly mortgage originations above a 4.5x loan-to-income ratio.

What does that mean for you? Say your household earns $200,000. A 4.5x ratio caps you at $900,000. If you need a $1,000,000 mortgage, your lender counts that loan against their 15% allowance.

So even if you pass the stress test, your application could hit a wall if your lender has already reached their LTI limit that quarter. In that case, you may need to look at credit unions or smaller lenders that aren’t subject to the same federal caps.

The 2026 Renewal Wave: What You Need to Know

About 60% of Canadian mortgages were set to renew between 2025 and 2026. Many of those were locked in at ultra-low rates below 2%. That’s why 2026 is often called the “crest of the renewal wave.”

No More Stress Test on Lender Switches

As of November 21, 2024, you can switch lenders at renewal without taking the stress test again. There are two conditions:

- Your mortgage balance stays the same (up to $3,000 in transfer fees is allowed)

- You don’t extend your amortization period

Previously, many borrowers were stuck with their existing lender because they couldn’t pass the test at today’s higher rates. Now, you can shop around for a better deal.

The Rate Jump Is Still Real

Even with the ability to switch, moving from a 2% rate to a 4% rate is a noticeable jump. Bank of Canada analysis shows the median mortgage debt service-to-income ratio is expected to rise from 15.3% to 18.0% for affected borrowers.

The silver lining? Most of these borrowers originally qualified at rates near 5.25% back in 2021. Their new rates are still below what they were tested at. That built-in cushion helps prevent widespread payment defaults.

Programs That Help You Save for a Bigger Down Payment

A larger down payment means a smaller mortgage and a smaller number being stress-tested. Two federal programs can help you get there faster.

The Tax-Free First Home Savings Account (FHSA)

The FHSA lets you contribute up to $8,000 per year, with a lifetime cap of $40,000. Contributions are tax-deductible. Withdrawals for a home purchase are completely tax-free.

By 2026, a couple who started saving early could have up to $80,000 ready (plus any investment growth). That goes straight toward your down payment.

The RRSP Home Buyers’ Plan (HBP)

The HBP withdrawal limit increased to $60,000 per person in 2024. If you withdrew between 2022 and 2025, you don’t need to start repaying until the fifth year after withdrawal. That gives you time to adjust to your new mortgage payments before worrying about your RRSPs.

Do Credit Unions Follow the Same Rules?

Not always. The federal stress test under OSFI’s Guideline B-20 only applies to federally regulated lenders, which include the big banks like RBC, TD, and Scotiabank.

Provincially regulated credit unions in B.C. and Ontario aren’t legally required to follow the same rules. Many choose to anyway, but some offer more flexibility.

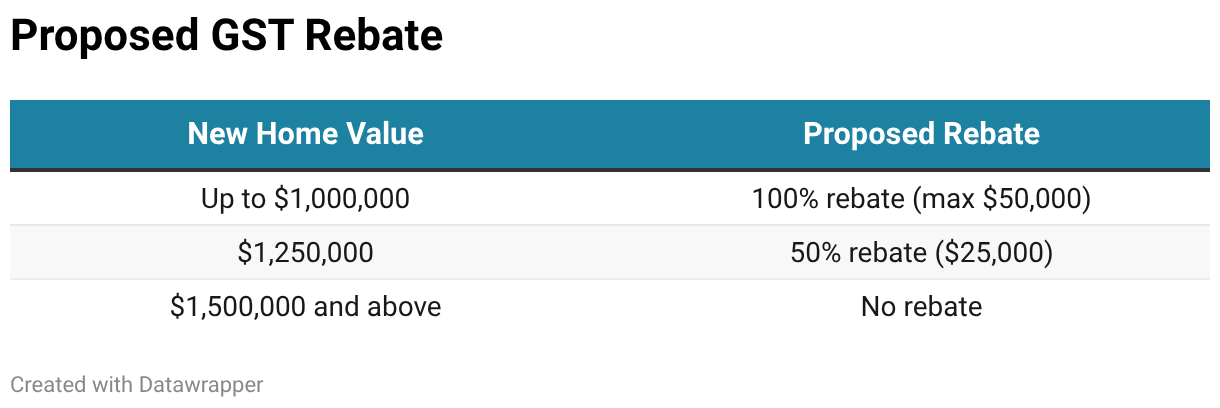

Proposed GST Rebate for First-Time Buyers

A federal proposal tabled in late 2025 would give first-time buyers a GST rebate on newly built homes. Here’s what’s on the table:

If this passes, first-time buyers could put those savings toward their down payment. A bigger down payment means a smaller mortgage to stress-test.

The Bottom Line

The Canadian mortgage stress test in 2026 is part of a bigger picture. It works alongside the LTI cap, the higher insured price cap, 30-year amortizations, and new savings programs to balance access with financial safety. The best thing you can do? Start early. Max out your FHSA and HBP contributions, reduce other debts, and talk to a mortgage professional who can map out your options before you start shopping.

Ready to see what you can afford? Zoocasa can connect you with a local real estate agent who understands your market and your budget. Start your search today.